1. Overview of the Chinese Automotive Market, 2005-2006

Having experienced a "Golden Period" in the H2 2005, China automobile market will be influenced by more industrial policies in 2006, such policies may include the adjustments in automobile customs, petroleum price and excise, the "three guarantees" policy£¨provisions on maintenance, replacement & return of private auto£© and incentive policies on the development of economical cars proclaimed by the National Development and Reform Commission.

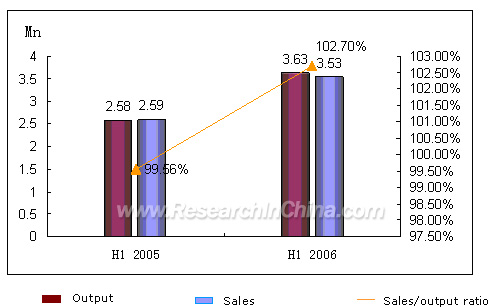

Good Sale of the Automobile in the H1 2006

In H1 2006, the production and sale of automobile broke through 3.5 million to 3.63 million units and 3.53 million, up by 28.94% and 26.71% than 2005 separately.

The Output and Sales volume of China Automotive Industry, H1 2005 and H1 2006

Here the output and sales of passenger vehicles are 2.60 million units and 2.51 million units separately, up by 40.30% and 36.53% than H1 2005; the output and sales of business vehicle are 1.03 million units and 1.02 million units respectively, up by 7.16% and 7.71% than H1 2005.

In H1 2006, both the production and sale of saloon car, multifunction passenger vehicle (MPV), sport utility vehicle (SUV) were on a growth spurt. The sale of MPV and SUV separately increased by 33.70£¥ and 38.68£¥ than H1 2005.

The sale of self-owned brands Chery, Geely, Brilliance, BYD, Great Wall etc. is increasing at a fabulous speed. Chery achieved a growth of 72.15% than 2005 in the sale of passenger vehicles, ascending to the 6th place in the Top 10 automobile manufacturers; Geely, with a growth of 55.62%, ranked at the 7th place and Brilliance, the 10th, up by 62.11%.

The Sales of Automobile in China, 2005

The Sales Volume of the Top 10 Manufacturers (by Automobile Total Sales Volume), Jan, 2005-Dec 2005 (Unit: thousand)

|

FAW |

Shanghai Automobile Industry Corporation (Group) |

Dongfeng |

Chang¡¯an |

Beijing Automobile Works |

Guangzhou Automobile Industry Group Co., Ltd. |

Hafei Motor Co., Ltd. |

Chery |

Jianghuai |

Geely |

|

983 |

917 |

729 |

631 |

597 |

237 |

230 |

189 |

154 |

151 |

The Sales Volume of the Top 10 Manufacturers (by Saloon Car Sales Volume), Jan, 2005-Dec 2005( Unit: thousand)

|

Shanghai GM |

Shanghai Volkswagen |

FAW Volkswagen |

Beijng Hyundai Motor |

Guangzhou Honda |

Tianjin FAW Xiali |

Chery |

Dongfeng Nissan |

Geely |

Dongfeng Peugeot Citroen |

|

325 |

250 |

240 |

234 |

231 |

190 |

189 |

157 |

150 |

140 |

2. Analysis on the Opportunity of Investment and Reorganization in China Automobile Industry

Since 1999, the rapid growth of medium and large passenger vehicles brought about another automotive investment fever. Before this, the investment subjects were the state and foreign capital, but now private capital and stock capital are involving. From 2001 to 2002, as the good performance of heavy-loaded tracks and saloon cars contributed a lot to the local tax income and employment, the local governments began to input a great deal of capital in the automotive industry. According to the official statistics, over the past few years, some hundred billion has been invested in automotive industry and 23 provinces have engaged in the production of saloon cars.

In these years, many manufacturers of household electric appliances begin to take part in the production of automobile, Chunlan, for instance, is producing motorcycle and automobile; Geely, another company originally in household and construction material fields, now devotes to motorcycle and automobile investment; so do Bird, BYD and Lifan. Konka and Shinco, too have switched their attention to the auto accessory & auto part industry.

In the global market, it is impossible for automobile manufacturers with an annual sale of less than 1 million units to survive independently. Even manufacturers with an annual capacity of 2 million units are facing reorganizations. Being dispersive and small, China automobile industry is weak in independent development. Currently about 13 automobile manufacturers have the production capacity of over 100 thousand unit vehicle per year, accounting for 91% of the China automotive market share. The number of the small and medium enterprises with annual sales less than 10 thousand vehicles adds up to a half more in Chinese 100 more automobile enterprises. All the above mentioned enterprises are not enough to or too weak to compete with those foreign large scale enterprises, instead they are more likely to go bankrupt or be merged by large ones, so merger is a trend for them to expand.

Typical cases of investment, acquisition and reorganization in automotive industry in recent years:

In Oct 2002, Shanghai Automobile declared to acquire 10% shares of GM Daewoo with USD 59.7 million.

In Feb 2004, Shenyang Jinbei GM was jointly reorganized by Shanghai Auto, GM and Shanghai GM. Shanghai Auto and GM (China) separately acquired 25% of the shares, while Shanghai GM held 50% of the shares to form the third whole-car production base.

On Oct 30, 2004, Chang'an Automobile Co., Ltd. and Jianglin Group separately invested RMB 50 million to establish the Jiangling Holding Co Ltd. On Dec, 6, Chang'an Automobile and Jianglin Group separately input RMB 450 million to enhance the capital capacitity of Jiangling Holding,Co, Ltd. And equally 50% of the shares were held separately.

In Mar 2005, Dongfeng Motor spent RMB 352 million to acquire 51% of the shares of Zhengzhou Nissan. Dongfeng Motor is a joint venture founded by Nissan and Dongfeng Motor, each holding 50% of the shares, which is the largest investment project of Nissan all over the world.

On July 23, 2005, Nanjing Motor Group acquired MG Rover with over 50 million pounds, and then began to make full use of the tangible assets to launch cars of its own brand one year later on this platform.

On August 8, 2005, Weichai Power spent RMB 1.023 billion and became the largest shareholder by acquiring 28.12£¥ of the total stock of Torch Automobile Group Co., Ltd, which is the most and largest eye-catching open tendering case. Weichai Power then follows the trend to integrate the advantageous capital from the affiliated companies of Torch such as Shanxi Automobile Group and Fast Gear

In the past blind expansion and unreasonably seeking diversification of the production could be seen now and then in merger and acquisition, while in the next few years, the investment and reorganization in automotive industry will bound to be more rational.

The whole automobile industry is speeding up to reorganize the investment. Such reorganizations will happen in the international and China automobile markets at the same time. The large state-owned enterprises and MNC will play the leading roles in the reorganizations.

|