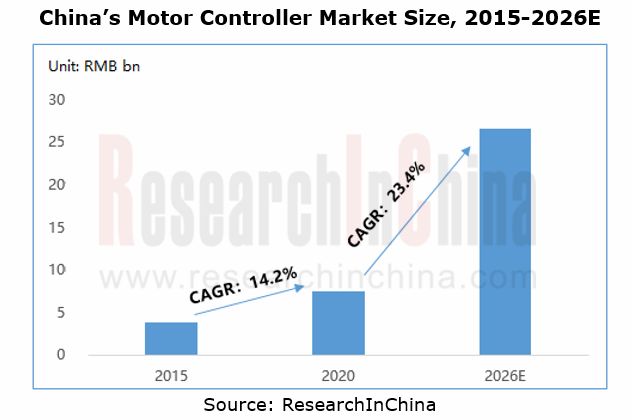

Automotive motor controller industry is expected to grow at CAGR of 23.4%, and local manufacturers are rising.

1) The growing new energy vehicle market gives a boost to the motor controller market.

The supply and demand in the electric vehicle motor controller market is dependent on the expansion of new energy vehicle market.

At present, countries and automakers worldwide have formulated their plans and requirements for the development of new energy vehicles. In future, new energy vehicle sales will be bound to surge. As the new energy vehicle market booms, the motor controller market will make steady growth. It is predicted that China’s motor controller market will sustain a CAGR of up to 23.4% between 2020 and 2026.

2) In the fiercely competitive motor controller market, local manufacturers lead the way.

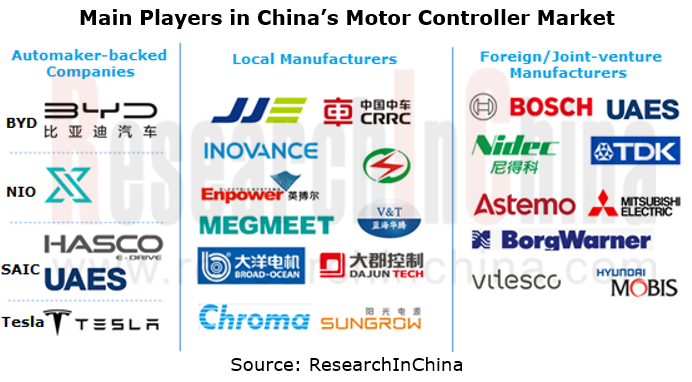

Currently, China’s electric vehicle motor controller market is intensely competitive. There are mainly three types of players: automaker-backed companies, local manufacturers, and foreign/joint-venture manufacturers. Among them, automaker-backed players support their own vehicles; local manufacturers are suppliers of Chinese independent auto brands; foreign/joint-venture companies build supply relationships with foreign/joint-venture auto brands.

Local manufacturers now have the upper hand on the strength of the development of homegrown new energy vehicle brands, especially emerging automakers. In 2020, seven out of the top ten manufacturers by market share were local companies, among which BYD still dominated the list with a 13.5% share; Inovance Technology, Sungrow and Huayu E-drive first edged into the top-ten list.

3) N-in-one products hold the trend, and three-in-one drive system will become the mainstream

Motor and ECU integration is a way to not only reduce weight and size of products but cut costs of production and procurement and improve efficiency. In current stage, most companies still stay at the two-in-one phase, while the three-in-one drive system will become the mainstream.

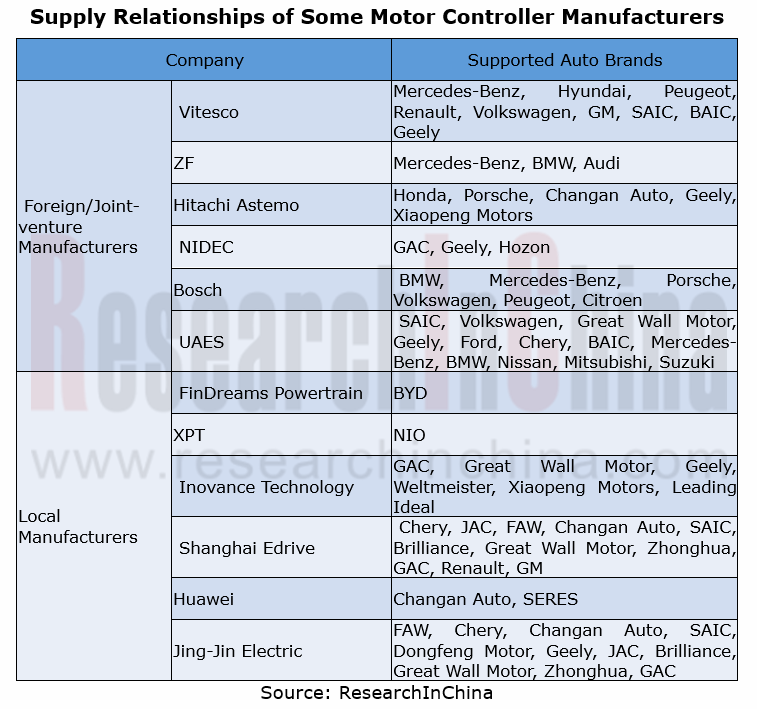

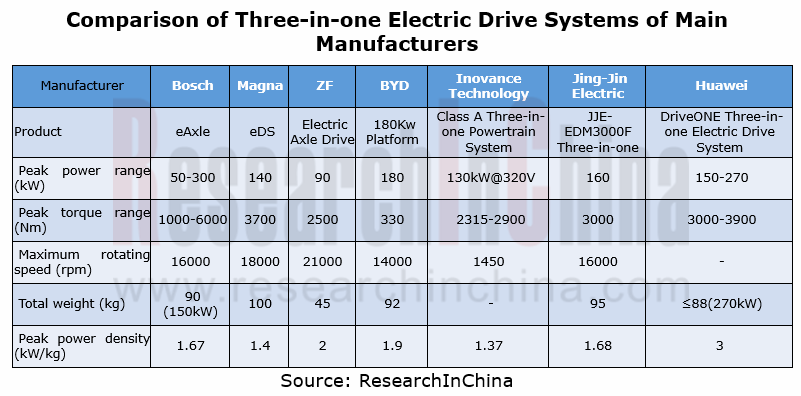

In 2020, China shipped more than 500,000 sets of three-in-one electric drive systems for passenger cars, or around 37% of the total motor controller shipments. Companies including Bosch, BYD, Inovance Technology and Jing-Jin Electric have rolled out their three-in-one electric drive systems. One example is Huawei DriveONE three-in-one electric drive system which boasts peak power density of 3kW/kg, the highest in the industry.

Through the lens of market share, the three-in-one system is still an oligopolistic market. In 2020, Tesla, BYD, XPT and NIDEC took a combined 82.1% of the total sales. Yet as Dongfeng SERES SF5 equipped with Huawei three-in-one system goes into mass production in 2021, the competition in the three-in-one electric drive system market will be more intense.

4) Power modules head in high voltage, and silicon carbide becomes a mainstream material.

New energy vehicles now use 400V electrical voltage systems. 80% SOC for a battery takes about 30 minutes, but the use of an 800V voltage system will cut the time down to 10 minutes. The need for fast charge makes high voltage power modules an inevitable trend.

Manufacturers like Hitachi Astemo, BorgWarner, Vitesco, Inovance Technology and ZF currently have introduced their 800V inverter/electric drive system products to meet fast charge needs, and all use silicon carbide (SiC) material except for Hitachi Astemo.

In BorgWarner’s case, its SiC inverter mass-produced in 2019 is the first 800V inverter using SiC power switch. The double-sided cooling structure makes the inverter 40% lighter and 30% smaller, improves its power density by 25%, and allows the inverter to perform better in thermal conductivity, high temperature stability and efficiency for shortening the charging time and extending the range.

Electric Controller Upstream Market

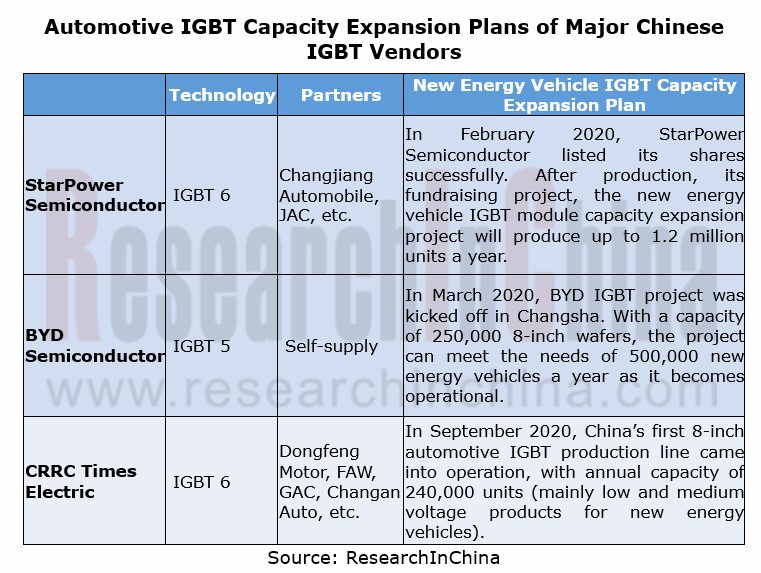

1) Automotive IGBT market—local companies gear up to scramble

IGBT module which plays a crucial role in new energy vehicles makes up roughly 45% of the cost of electric vehicle motor controller.

Current local companies such as BYD Semiconductor, StarPower Semiconductor and CRRC Times Electric already work hard on new energy vehicle IGBT development, and race to expand their capacity to rival their foreign peers.

China’s automotive IGBT market is dominated by international vendors like Infineon, Mitsubishi Electric, Semikron and Denso, among which Infineon shares over half the market, up to 58.2% in 2019. BYD Semiconductor, StarPower Semiconductor and CRRC Times Electric were however on the list of the top ten automotive IGBT vendors in 2019, especially BYD Semiconductor which became the runner-up with market share of 18%, far higher than the third-ranking Mitsubishi Electric which occupied just 5.2%.

2) Silicon carbide power devices are expected to be an alternative to IGBT, a key component of motor controller.

Globally, there is a belief that silicon carbide is the next-generation semiconductor material.

Compared with Si-based IGBT power devices, silicon carbide (SiC) power devices feature lighter weight, smaller size, higher power density, longer range, lower controller loss, better thermal conductivity, and stronger high temperature resistance. Motor controllers using SiC power devices are an effective way for new energy vehicles to improve range, power mass density, and electric energy conversion efficiency. So SiC power devices are expected to replace IGBT as a key component of motor controller.

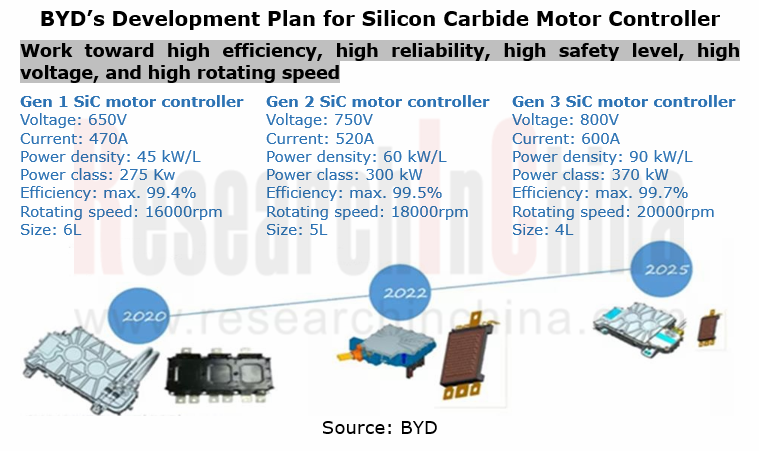

Manufacturers such as Delphi and BYD have set about making deployments in SiC motor controller. BYD indicated that from 2020 to 2025, its SiC motor controllers will have three iterations, with applicable voltage platforms up to 800V, power density up to 90kW/L, efficiency up to 99.7%, and rotating speed up to 20,000 rpm.

Research Report on AI Applications in Cockpits, 2026

AI Application in Cockpits: AI Services Become More Comprehensive, Convenient, and Refined.

In the first half of 2026, cockpit AI functions underwent initial upgrades across multiple dimensions, inc...

Software-Defined Vehicles in 2026: OEM Software Development and Supply Chain Deployment Strategy Research Report

Research on OEMs’ Software Strategies: R&D Focus, Development Strategies and Supplier Building Models of 30 OEMs

In this paper, we adopt a research framework covering 13 subsystems and 48 sub-di...

Passenger Car Chassis Domain Control and Chassis Cross-Domain Integration Research Report, 2026

Chassis Control Research: Mass Production of Full Chassis-by-Wire Solutions Starts

1. A Cluster of Full Chassis-by-Wire Solutions Make Their Debut, and EMB Enters Mass Production and Adoption for the...

Central Domain Control (Powertrain, Chassis, Body) and Motion Controller Research Report, 2026

Central Domain Control and Motion Control Research: XYZ Coordinated Control and Full X-by-Wire Actuation System

With the gradual penetration of L3+ autonomous driving, the chassis control system is ...

48V Low-voltage Power Distribution Network (PDN) Architecture and Supply Chain Panorama Research Report, 2026

Research on 48V Low-Voltage Power Distribution Network (PDN): An Active 48V Supply Chain, with Priority Deployment in High-Power Scenarios Such as Steer-by-Wire Chassis

The automotive 48V low-voltage...

AI-Defined Vehicle (AIDV) OEMs' Deployment Strategies Research Report, 2026

AIDV Research: Deployment Strategies of 22 OEMs

The AI-Defined Vehicle (AIDV) OEMs' Deployment Strategies Research Report, 2026, released by ResearchInChina, analyzes the AI deployment strategies of ...

OEMs’ Passenger Car Model Planning Research Report, 2026

Vehicle Model Planning Research: Chinese OEMs Launch Sub-Brands Intensively, While Multinational OEMs Apply the Brakes to Electrification Strategies

ResearchInChina released the OEMs’ Passenger Car M...

Autonomous Driving Simulation and World Model Research Report, 2026

Autonomous driving simulation research: "Simulation test + world model"-driven test system has become R&D infrastructure.

The "Autonomous Driving Simulation and World Model Research Report, 2026"...

Cockpit-Driving Integration Central Domain Controller SoC and AI Supercomputing Architecture Research Report, 2026

Cockpit-Driving integration and AI supercomputing research: The One Chip solution is rapidly installed in vehicles, and AI supercomputing architectures are moving towards full-domain integration.

AI ...

Intelligent Driving End-to-End Large Model Research Report, 2026

Research on Intelligent Driving Large Models: A Critical Period for Technological Competition and Paradigm Integration

As autonomous driving technology rapidly iterates from L2 to L3?L4, intelligent...

Automotive Digital Key Industry Trend Report, 2026

Digital Key Research: Automotive BLE, UWB and SLE Hardware Layout

The Automotive Digital Key Industry Trend Report, 2026, released by ResearchInChina, analyzes and predicts the digital key market, co...

Monthly Report on Automotive New Technology (May 2026)

UHD gaze technology, full-color LiDAR, UWB, etc. promote the upgrade of intelligent driving perception capabilities

This report is published once a month and is available for annual subscription.The...

In-Cabin Monitoring Systems (DMS, OMS, etc.) Research Report, 2026

In-Cabin Monitoring System Research: DMS to Become Mandatory in 2027, Expected to be Installed in Over 14 Million Vehicles

ResearchInChina released the In-Cabin Monitoring Systems (DMS, OMS, etc.) Re...

Automotive Service-Oriented Architecture (SOA) and Cross-Domain Middleware Industry Report, 2026

Research on automotive SOA and cross-domain middleware: The era of AI atomic services and AI cross-domain fusion agents is coming.

Automotive SOA evolves towards AI + full SOA servitization Driv...

Automotive Display, Center Console and Cluster Industry Report, 2026

Automotive Display Research: Multi-Screen Application Slows Down, While OLED and MiniLED Are Introduced in Vehicles Quickly

In 2026, automotive displays will no longer excessively pursue the number a...

Global and China Intelligent Vehicle Standard System Construction and Certification Research Report, 2026

Intelligent Driving Standards and Certification: With the Maturing Standardization System, China Will Participate in Formulation of Global Standards

China's automotive industry is transforming from ...

Automotive Intelligent Diagnosis Industry Report, 2026

Automotive Intelligent Diagnosis Research: Powered by AI, Remote Diagnosis Is Being Upgraded towards Intelligence.

ResearchInChina released the Automotive Intelligent Diagnosis Industry Report, 2026....

Automotive Cloud Service Platform Research Report, 2026

Research on automotive cloud service platform: with architecture upgrade and computing power improvement, cloud services enter a new stage

In 2026, the Internet of Vehicles industry generates petaby...