Passenger Car Radar Industry Research in 2023:

?In 2023, over 20 million radars were installed, a year-on-year jump of 35%;

?Driven by multiple factors such as driving-parking integration, NOA and L3, 5R solutions will become the mainstream configuration in the market in 2026.

?Influenced by the rising sales of China’s local suppliers, intelligent involution and other factors, localization is a megatrend.

?4D radars have landed on vehicles on a small scale and are expected to be mass-produced and installed on a large scale during 2025-2026.

?At present, 4D radars mainly involve cascade solutions; single-chip solutions will become the focus of the future layout and be implemented in 5-8 years.

?Analysis on BOM of Jingwei Hirain’s MRR510 front radar.

1. In 2023, over 20 million radars were installed, a year-on-year jump of 35%; it is estimated that more than 5 million 4D radars will be installed in 2026

According to ResearchInChina, 20.021 million radars will be installed in new passenger cars in China in 2023, up 21.6% year on year; in 2026, the number will hit 39.618 million.

From January to June 2023, the overall installations of 4D radars in new passenger cars in China exceeded 114,000 units, accounting for 1.3% of the total radar installations. In terms of the replacement order, 4D radars will first replace front radars, that is, priority will be given to meeting the driving needs in intelligent driving, and second replace corner radars to better meet high-level safety function requirements. It is expected that the installations of 4D radars will reach 5.594 million units in 2026, making up 14.1% of the total radar installations.

The main factors driving up radar installations include:

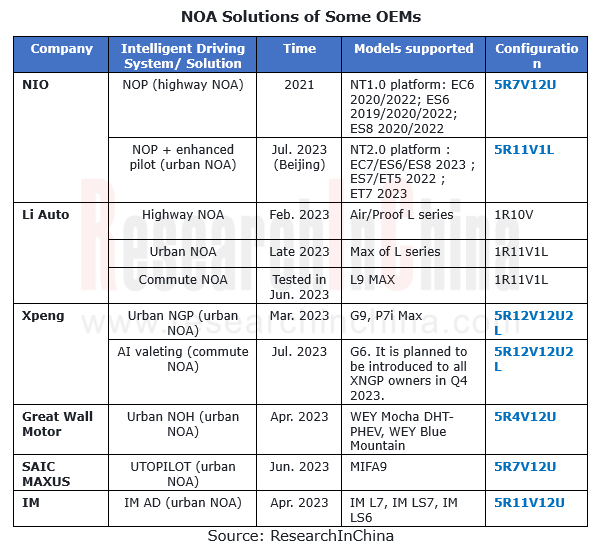

Consumer side: OEMs focus on deploying NOA functions, of which 5R becomes standard

NOA, a hotspot in the layout of major OEMs, includes highway NOA, urban NOA and commute NOA, among which 5R NOA solutions prevail in the market.

Highway NOA (L2.5): At the end of 2020, some Chinese automakers began to apply NOA to highway scenarios, and highway NOA thus became a layout highlight. In 2022, highway NOA intensively boarded vehicles.

Urban NOA (L2.9): In the second half of 2022, Xpeng, AITO and other OEMs took a lead on planning urban scenarios, extending NOA from highways to urban areas. In 2023, most leaders engaged in intelligent driving released their urban NOA plans, so 2023 marked the first year of urban NOA.

Commute NOA: it is the combination of urban NOA + route memory, and the selling point is to make it convenient to commute. It is likely to become another new arena following urban NOA. At present, companies that have launched such a solution include Li Auto and Xpeng.

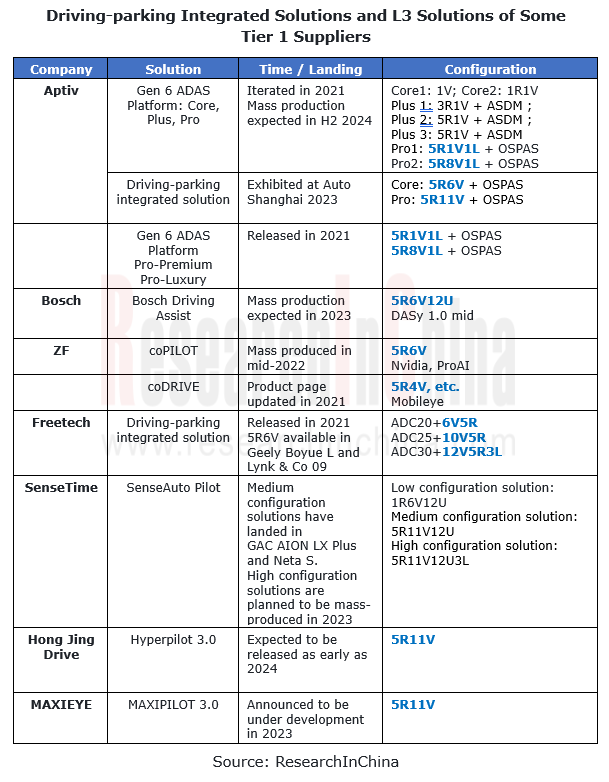

Supply side: Tier1 suppliers at home and abroad have introduced a large number of driving-parking integrated solutions and a variety of L3 solutions, which take 5R as the mainstream configuration.

For the driving-parking integrated solutions launched by many international and Chinese Tier 1 suppliers such as Aptiv, ZF, Freetech and iMotion, 5R has become the standard configuration of most mid-to-high-end solutions. According to the statistics of ResearchInChina, from January to May 2023, 490,000 sets of driving-parking integrated solutions were installed in production models, a like-on-like spurt of 138%; the installation rate hit 6.7%, up about 3.8 percentage points from the prior-year period. By 2025, the installations will reach 6.19 million sets, and the installation rate will climb to 30%.

As L3-related laws and regulations mature, the implementation of L3 has been put on the agenda, and will become another driving force for 5R solutions. For L3 solutions launched by Tier 1 suppliers, such as Bosch, Aptiv, Hong Jing Drive and MAXIEYE, 5R has also been a standard configuration.

The implementation of NOA and driving-parking integration as well as future L3 solutions will directly boost the installations of 5R solutions. According to the data from ResearchInChina, it is estimated that the proportion of 5R solutions will be 8.15% in 2023, 5.49 percentage points higher than that in 2021; the proportion of 5R solutions will reach up to 39.6% in 2026.

2. 4D radars are mainly cascade solutions, and single-chip solutions are expected to be implemented within 5-8 years.

Radar chips have passed through four development phases: radio frequency front end + processor; single SOC + digital analog; small-scale separation of SoC to the large-scale; a single chip can meet the needs of OEMs for high-level intelligent driving, a phase when the functional applications and scenarios of intelligent driving have basically been solidified, and the demand from OEMs has also stabilized.

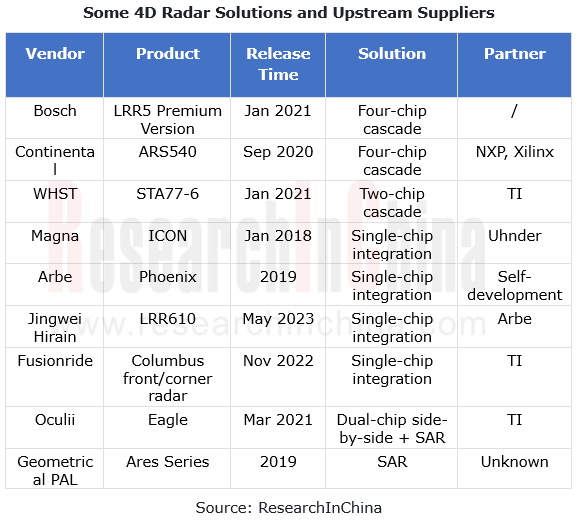

4D radar technology routes can be roughly divided into multi-chip cascade, single-chip integration, virtual aperture imaging, and metamaterials. Currently, the 4D radars that have been or will be installed in passenger cars are mainly multi-chip cascade, especially two-chip and four-chip cascade. Mature single-chip solutions will have cost performance/cost advantages, and are expected to become the focus of the future layout and be implemented in 5-8 years.

Models such as BMW IX, Li L7, and Rising Auto R7 have been confirmed to be equipped with 4D radars. Among them, Rising Auto R7 adopts ZF's FRGen21 front radar, 4-chip cascade 12T16R from TI and Xilinx, and Hella’s 4D corner radar; Li L7 Pro uses WHST's STA77-6 front radar, and 2-chip cascade 6T8R from TI.

At present, the main suppliers of single-chip solutions are TI, Arbe, and Uhnder.

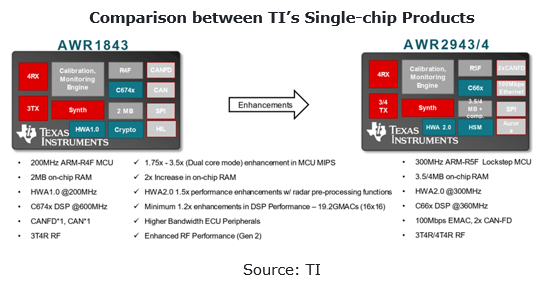

TI released AWR2944, its second-generation radar single chip, in January 2022. Compared with the previous AWR1843, AWR2944 adopts a 4T4R solution, which has one more transmitting channel than AWR1843 and can improve angle estimation. The MCU is upgraded from R4F to R5F with dual-core lock step, and the DSP is upgraded from C67x to C66x. HWA (radar algorithm accelerator) iterates from version 1.0 to 2.0, supporting radix-2 and radix-3 FFT, CFAR-OS and data compression. At present, the 4D radars based on this chip include WHST’s STA77-5S forward radar and Fusionride’s Columbus forward radar series.

3.Influenced by the rising sales of China’s local suppliers, intelligent involution and other factors, localization is a megatrend.

In the infancy of intelligent driving, conventional OEMs give priority to safety, quality and intelligent driving system integration when selecting suppliers, so they will prefer mature brands represented by foreign Tier 1 suppliers like Continental and Bosch which are versed in the automotive field to ensure that their software and hardware meet automotive standards. Foreign suppliers enjoy first-mover advantages and industry influence, so they sweep 90% of the Chinese radar market.

In 2022 and H1 2023, in the Chinese radar market, foreign suppliers took a more than 95% share, among which Bosch, the largest front radar supplier, made up 50.6% of the market in H1 2023, and Hella, the largest corner radar supplier, occupied 49.8% in H1 2023.

For Chinese radar suppliers, the key to catching up with and overtaking foreign counterparts lies in technical expertise, qualifications, and mass production experience, so radar suppliers with great technical strength and certain mass production experience gain greater first-mover advantages.

For example, Nova Electronics began to develop radars in 2014 and launched its first corner radar in 2018. So far, its products have covered front radars (including 4D radars), corner radars and cockpit radars. At present, the main products include NOVA 77GF-B Plus front radar (mass-produced in Q1 2022), NOVA 77GB-C corner radar (mass-produced in Q2 2021), NOVA 77GB-C Pro corner radar (mass-produced in February 2022), NOVA 77GB-T corner radar (mass-produced in 2022) and 4D imaging radar (launched in 2023 and designated by three OEMs).

WHST, established in 2015, supplied corner radars in small quantities in 2016. In 2018, the STA24-1 corner radar landed in two models, including Leopaard Mattu. Now, its products embrace front radars (including 4D radars), corner radars, cockpit radars, side radars and tailgate radars. The main products include STA 77-5 forward radar (mass-produced in 2021), STA 77-6 4D front radar (mounted on Li L7 Pro and Deepal SL03 in 2023), and STA 77-8 4D front radar (the company built cooperation with first-tier OEMs in China on custom development based on this product in 2022).

Chuhang Tech, founded in 2018, launched its first corner radar - ARC1 in December 2019. At present, its products cover front radars (including 4D radars), corner radars, cockpit radars, and stealth radars (innovative products). The main products include ARF front radar (installed by Neta, Leapmotor and JAC in 2022), ARC corner radar (available in Haima and Leapmotor in 2022), 4D front radar with 6 transmitters and 8 receivers (used by Windrose Technology and an independent new energy vehicle company in 2023), and 4D front radar with 12 transmitters and 16 receivers.

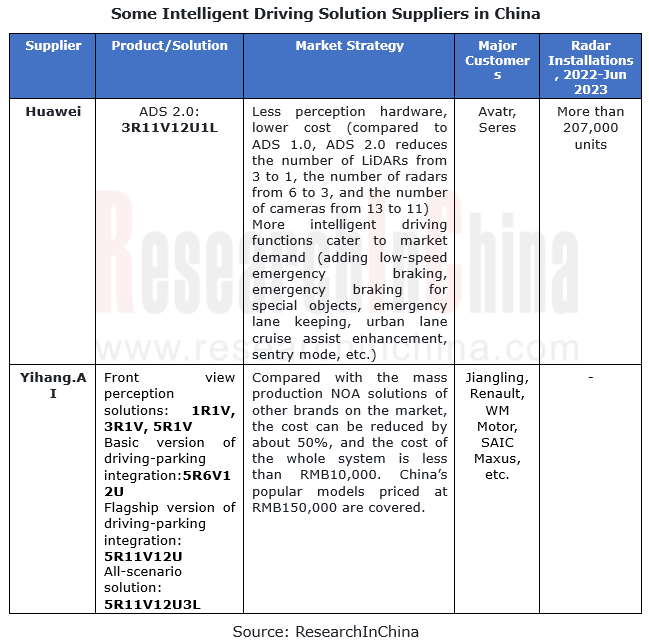

In the future, as technology matures, intelligent driving solutions will head in the direction of lower cost, higher efficiency, supporting services, application and localized delivery. By then, the advantages of domestic radar suppliers will be highlighted. For example, local suppliers such as Huawei and Baidu carry out more flexible market strategies than foreign Tier 1 suppliers. For example, compared with ADS 1.0, Huawei's ADS 2.0 cuts down hardware while improving intelligent driving functions, achieving cost reduction and efficiency improvement. ADS 2.0 has been installed in Avatr 11, AITO M5 and other models, among which the sales of AITO M5 totaled 69,000 units from 2022 to June 2023, with 207,000 radars installed. Yihang.AI's driving-parking integrated and all-scenario solutions also have a big cost reduction, with cost slashed by about 50% compared with other NOA solutions on the market.

4. Analysis on BOM of Jingwei Hirain’s MRR510 front radar

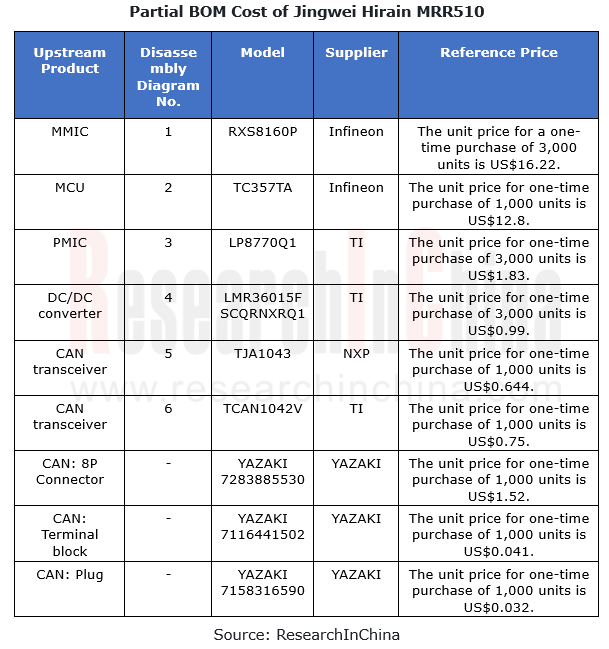

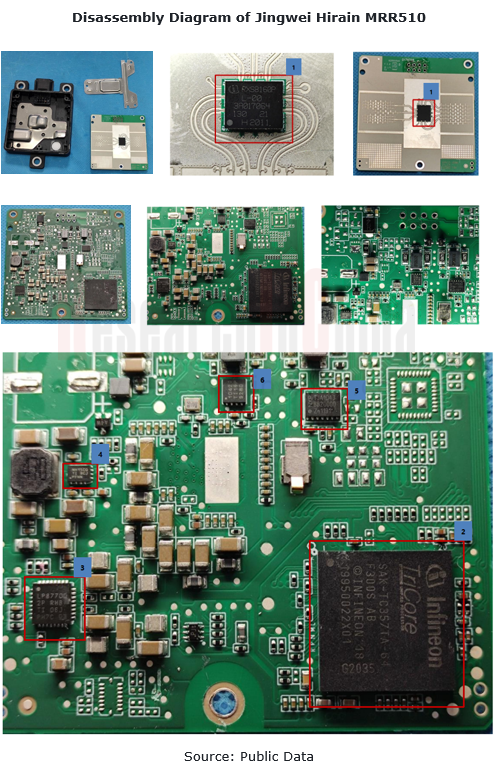

MRR510 is a 77GHz front radar released by Jingwei Hirain in 2022, with the ranging of 0.5-190m, the ranging accuracy of ±0.1m, the HFOV of 90°, the VFOV of 18°, and the side angle accuracy of ±0.5°, and the speed measuring accuracy of ±0.05 m/s. It has been available to SAIC, JAC, Jiangling Ford and other brands. The chip solution has 3 transmitters and 4 receivers, and the upstream suppliers include Infineon, TI and NXP. Referring to the market price, the BOM cost of the known parts of MRR510 is approximately USD35.827.

Automotive Cloud Service Platform Industry Report, 2024

Automotive cloud services: AI foundation model and NOA expand cloud demand, deep integration of cloud platform tool chainIn 2024, as the penetration rate of intelligent connected vehicles continues to...

OEMs’ Passenger Car Model Planning Research Report, 2024-2025

Model Planning Research in 2025: SUVs dominate the new lineup, and hybrid technology becomes the new focus of OEMs

OEMs’ Passenger Car Model Planning Research Report, 2024-2025 focuses on the medium ...

Passenger Car Intelligent Chassis Controller and Chassis Domain Controller Research Report, 2024

Chassis controller research: More advanced chassis functions are available in cars, dozens of financing cases occur in one year, and chassis intelligence has a bright future. The report combs th...

New Energy Vehicle Thermal Management System Market Research Report, 2024

xEV thermal management research: develop towards multi-port valve + heat pump + liquid cooling integrated thermal management systems.

The thermal management system of new energy vehicles evolves fro...

New Energy Vehicle Electric Drive and Power Domain industry Report, 2024

OEMs lead the integrated development of "3 + 3 + X platform", and the self-production rate continues to increase

The electric drive system is developing around technical directions of high integratio...

Global and China Automotive Smart Glass Research Report, 2024

Research on automotive smart glass: How does glass intelligence evolve

ResearchInChina has released the Automotive Smart Glass Research Report 2024. The report details the latest advances in di...

Passenger Car Brake-by-Wire and AEB Market Research Report, 2024

1. EHB penetration rate exceeded 40% in 2024H1 and is expected to overshoot 50% within the yearIn 2024H1, the installations of electro-hydraulic brake (EHB) approached 4 million units, a year-on-year ...

Autonomous Driving Data Closed Loop Research Report, 2024

Data closed loop research: as intelligent driving evolves from data-driven to cognition-driven, what changes are needed for data loop?

As software 2.0 and end-to-end technology are introduced into a...

Research Report on Intelligent Vehicle E/E Architectures (EEA) and Their Impact on Supply Chain in 2024

E/E Architecture (EEA) research: Advanced EEAs have become a cost-reducing tool and brought about deep reconstruction of the supply chain

The central/quasi-central + zonal architecture has become a w...

Automotive Digital Power Supply and Chip Industry Report, 2024

Research on automotive digital power supply: looking at the digital evolution of automotive power supply from the power supply side, power distribution side, and power consumption side

This report fo...

Automotive Software Business Models and Suppliers’ Layout Research Report, 2024

Software business model research: from "custom development" to "IP/platformization", software enters the cost reduction cycle

According to the vehicle software system architecture, this report classi...

Passenger Car Intelligent Steering Industry Research Report, 2024

Intelligent Steering Research: Steer-by-wire is expected to land on independent brand models in 2025

The Passenger Car Intelligent Steering Industry Research Report, 2024 released by ResearchInChina ...

China Passenger Car Mobile Phone Wireless Charging Research Report, 2024

China Passenger Car Mobile Phone Wireless Charging Research Report, 2024 highlights the following:Passenger car wireless charging (principle, standards, and Qi2.0 protocol);Passenger car mobile phone ...

Automotive Smart Exteriors Research Report, 2024

Research on automotive smart exteriors: in the trend towards electrification and intelligence, which exteriors will be replaced by intelligence

The Automotive Smart Exteriors Research Report, 2024 r...

Automotive Fragrance and Air Conditioning System Research Report, 2024

Research on automotive fragrance/air purification: With surging installations, automotive olfactory interaction is being linked with more scenarios.

As users require higher quality of personalized, i...

Intelligent Vehicle Multi-Domain Computing Industry Report, 2024

Multi-Domain Computing Research: A Summary of Several Ideas and Product Strategies for Cross-Domain Integration

1. Several ideas and strategies for cross-domain integration of OEMs

With the increasi...

Analysis on Xiaomi Auto's Electrification, Connectivity, Intelligence and Sharing, 2024

Research on Xiaomi Auto: Xiaomi Auto's strengths and weaknesses

Since the release of SU7, Xiaomi delivered 7,058 units and 8,630 units in April and May, respectively, and more than 10,000 units in bo...

ADAS and Autonomous Driving Tier 1 Suppliers Research Report, 2024 - Foreign Companies

Research on foreign ADAS Tier 1 suppliers: make all-round attempts to transform and localize supply chain and teams.???

1. Foreign ADAS Tier 1 suppliers fall behind relatively in development of inte...