Global and China Automotive Semiconductor Industry Report, 2014-2015

-

Sep.2015

- Hard Copy

- USD

$2,400

-

- Pages:114

- Single User License

(PDF Unprintable)

- USD

$2,200

-

- Code:

ZYW215

- Enterprise-wide License

(PDF Printable & Editable)

- USD

$3,500

-

- Hard Copy + Single User License

- USD

$2,600

-

Global and China Automotive Semiconductor Industry Report, 2014-2015 mainly focuses on the following:

1. Global automotive market and industry;

2. China’s automotive market and industry;

3. Automotive semiconductor industry and market;

4. Fifteen major automotive semiconductor companies

In 2014, the global automotive semiconductor market size approximated USD28 billion, up 7.3% from 2013. It is predicted that in 2015 the market size will amount to USD29.6 billion, up 5.7% from a year earlier, and that by 2016 the growth rate will continue to decline, to only 3.7%. That was mainly attributed to the following two factors: first, remarkable deflation globally, which resulted in a substantial depreciation of the Japanese yen and the euro against the dollar; second, China, the world’s largest auto market, is very likely to go into decline. In 2015, China’s auto market is expected to edge up merely 1%, but may slide by 2% in 2016.

Automotive semiconductor falls into five categories: power semiconductor, sensor semiconductor, processor (main for MCU) semiconductor, ASSP (principally Connectivity and Amplifier) semiconductor, and logic semiconductor. In the field of traditional automobiles, the semiconductor costs for each unit approximate USD320, of which power occupies 26% and sensor 16%. In HEV, however, this figure is USD690, of which power represents as much as 75%. In EV, the semiconductor costs come to USD700, of which power accounts for 55%. But due to ongoing depressed oil prices, the market space of HEV/EV has been considerably squeezed. If the oil price returns back more than USD100, then the automotive semiconductor market will increase significantly.

In 2015, the market size of automotive sensors would reach about USD4.7 billion. Automotive sensors consist of CMOS Image Sensor, Pressure, Acceleration, Speed and Position, Magnetic (Hall effect), and Angle, among which CMOS Image Sensor mainly involves ON Semiconductor and OVT. The largest pressure sensor player is Sensata, which is also the biggest auto sensor maker worldwide. Moreover, Sensata is adept at Speed and Position. As the world’s second largest auto sensor company, Bosch specializes in Acceleration and Angle. ON Semiconductor is the world’s third largest sensor company. Infineon, the fourth largest sensor player in the world, mainly operates Magnetic (Hall effect) and Acceleration. Allegro, the world’s fifth sensor player under Sanken, is good at Magnetic (Hall effect) and Acceleration. In addition, other large auto sensor companies include Analog Devices, Melexis, Micronas, NXP, and STMicroelectronics.

In 2015, the market size of automotive processors, including MCU, DSP, and GPU, totaled some USD7 billion. In MCU market, Renesas takes absolutely the first place, with a market share of 40%, in contrast to 22% for Freescale. In the 32-Bit MCU market, Freescale accounts for the largest portion, Infineon and TI follows with 13% and 8% share, respectively. Other large players include STMicroelectronics and Spansion (Cypress).

Automotive power semiconductor mainly involves Power Management ICs, MOSFET, IGBT, and Diodes (Fast Recovery, Schottky, and High Voltage). HEV/EV needs a large quantity of IGBT, whose price is very high, thus leading to a sharp increase in costs of power semiconductor. Low-power circuit typically uses MOSFET while high-power and high-current circuit needs IGBT. SiC MOSFET is the most efficient, with high temperature resistance, far lower price than that of GaN, and more mature technology. So, it has good prospects in the future.

Automotive power semiconductor market has a low concentration, which provides a living space to some small companies. It is worth noting that to develop hybrid electric vehicle, Toyota ventured into the field of power semiconductor, so that its strength in IGBT is not inferior to specialized IGBT companies. Besides, Toyota is also not dwarfed by specialized automotive power semiconductor players in SiC MOSFET field.

Infineon, the largest automotive power semiconductor vendor, acquired IR, a move that helped bridge the gap in LV MOSFET, with the market share rising to 24%. STMicroelectronics, which specializes in Power Management, ranks second. What comes next is Renesas, Fuji Electric, and Bosch.

1 Global Semiconductor Industry

1.1 Market Status

1.2 Supply Chain

1.3 Industry Overview

2 Global and China Automobile Market

2.1 Global Automobile Market

2.2 Automobile Market Overview in China

2.3 Latest Development of Automobile Market in China

3 Automotive Semiconductor Market and Industry

3.1 Automotive Semiconductor Market Size

3.2 Overview of Automotive Sensor

3.3 Automotive CMOS imaging sensor

3.4 Automotive Sensor Industry

3.5 Automotive Processor

3.6 Automotive Processor Industry

3.7 Automotive Power Semiconductor

3.8 HEV/EV Power Semiconductor

3.9 Automotive Power Semiconductor Industry

3.10 Distribution of ADAS, Infotainment, and Body Semiconductor

3.11 Ranking of Automotive Semiconductor by Revenue

4. Automotive Semiconductor Companies

4.1 Infineon

4.2 Bosch Semiconductor

4.3 Rohm

4.4 ON SEMI

4.5 TI

4.6 STMicroelectronics

4.7 Renesas

4.8 Freescale

4.9 NXP

4.10 Melexis

4.11 Sensata

4.12 Fuji Electric

4.13 TDK

4.14 Murata

4.15 Allegro

Global Semiconductor Market Size, 2013-2019E

Global Semiconductor Market Distribution by Product, 2013-2016E

Growth Rate of Global Semiconductor Products, 2013-2016E

Semiconductor Outsourced Supply Chain

Semiconductor Company Systems

Semiconductor Outsourced Supply Chain Example

Food Chain IC CAD Design Industry

Top 25 Semiconductor Sales Leaders, 1Q2014

Top25 Semiconductor Sales Leaders, 1Q2015

Global Automobile Sales Volume, 2010-2015

Global Light Vehicle Output by Region, 2003-2015

Automobile Sales Volume in China, 2005-2015

Output YoY Growth of Vehicles in China by Model, 2008-2015

Global Automotive Semiconductor Market Size, 2012-2018E

Automotive Semiconductor Distribution by Product, 2014

Automotive Semiconductor Distribution by Application, 2012-2018E

Automotive Sensor Distribution

Sensors in Powertrain Applications

Sensors in Safety Applications

Shipments of Automotive CMOS Imaging Sensors, 2009-2018E

Market Share of Major Automotive CMOS Imaging Sensor Manufacturers, 2015

Ranking of Automotive Sensor Player by Revenue, 2014-2015

Ranking of Global MEMS Manufacturers by Revenue, 2013-2014

Automotive Processor Market Size, 2012 vs 2019E

Automotive Processor Per Vehicles, 2007 vs 2012 vs 2020E

Market Share of Major Automotive MCU Manufacturers, 2015

EV Vehicles Current Block Diagram

Power Semiconductor Devices in Toyota Prius

Power Semiconductor Devices in Toyota Lexus Ls600H

Market Share of Major Power Semiconductor Companies, 2014

ADAS Semiconductor by Type, 2013

Infotainment Semiconductor by Type, 2013

Body Semiconductor by Type, 2013

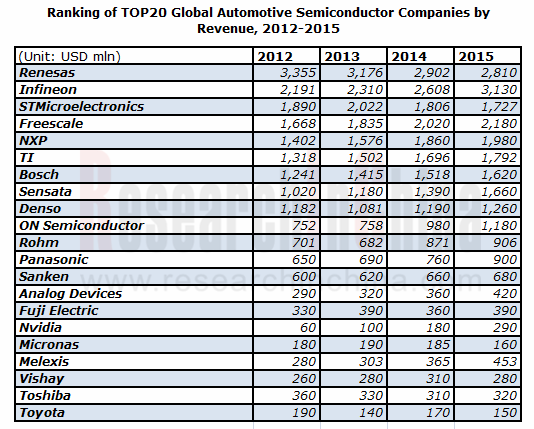

Ranking of Top 20 Automotive Semiconductor Companies by Revenue, 2012-2015

Infineon’s Revenue vs Gross Margin, FY2010-FY2015

Infineon’s Operation Margin and Net Margin, FY2010-FY2015

Infineon’s Assets and Liabilities, CY2015 H1

Infineon’s Employee by Region, CY2015 H1

Infineon’s Revenue by Region, FY2010-FY2015

Infineon’s Revenue by Segment, FY2011-FY2015

Infineon’s Operation Profit by Segment, FY2011-FY2015

Infineon’s Automotive Semiconductors Position

Infineon’s Automotive Segment Revenue by Region

Infineon’s Automotive Segment Revenue by Product

Infineon’s Automotive Segment Revenue by Application

Infineon’s Investments, FY2009-FY2015

Rohm’s Sales and Operation Margin, FY2011-FY2016

Rohm’s Sales by Segment, FY2011-FY2016

Rohm’s Operation Profit by Segment, FY2011-FY2016

Rohm’s Revenue by Application, FY2004-FY2016

ON Semi’s Revenue vs Operation Income, 2010-2015

Revenue of ON Semi by Segment, 2010-2015

Revenue Structure of ON Semi by Geographic Location, 2012-2014

Revenue Structure of ON Semi by Application, 2012-2017E

On Semi’s Major Product Application and Customer

On Semi’s Automotive Semiconductor Focus, 2014

On Semi’s Major Products

On Semi’s SPG Segment by Application, 2014

On Semi’s Position

On Semi’s SSG Segment by Application, 2014

ON SEMI’s ISG Segment Milestone

ON SEMI’s APG Segment Automotive Revenue, 2012-2014

TI’s Revenue vs Gross Margin, 2010-2015

TI’s Revenue by Segment, 2010-2014

TI’s Operation Profit by Segment, 2010-2014

TI’s Revenue by Application, 2013-2015

TI’s Automotive Infotainment Block Diagram

TI’s Automotive Charging Spot

STMicro Revenue vs Gross Margin, 2010-2015

STMicro’s Revenue by Region, 2014

STMicro’s Revenue by Product, 2014

STMicro’s APG Segment Revenue, 2005-2014

STMicro’s Automotive Semiconductor Market Position

Renesas’ Revenue vs Gross Margin, FY2011-FY2016

Renesas’ Gross Margin, Q2/CY2013-Q2/CY2015

Renesas’ Operation Margin, Q2/CY2013-Q2/CY2015

Renesas’ Automotive Business Revenue, Q2/CY2013-Q2/CY2015

Renesas’ General-purpose Business Revenue, Q2/CY2013-Q2/CY2015

Renesas Automotive Focus

Renesas HEV/EV Automotive Focus

Renesas HEV/EV Automotive MCU Roadmap

Renesas Powertrain MCU Roadmap

Renesas Chassis MCU Roadmap

Renesas Airbag MCU Roadmap

Renesas ADAS MCU Roadmap

Renesas Instrument Cluster MCU Roadmap

Renesas Car Audio MCU Roadmap

Freescale’s Revenue vs Operation Margin, 2007-2015

Freescale’s Revenue Breakdown by business, 2012-2015

Freescale’s Revenue Breakdown by customer, 2014

Freescale’s Revenue Breakdown by region, 2011 vs 2014

Freescale’s Major Product and Application

Freescale ADAS

Major Locations of Freescale

NXP Revenue Vs Operation Margin, 2010-2015

NXP Consolidated Balance Sheet Data, 2010-2014

NXP Automotive Sales by Product, 2014

NXP Automotive Sales by Region, 2014

NXP Customers

Major NXP Automotive Facilities

Melexis’ Financial Position, CY 2015H1

Melexis’ Revenue by Region, 2013-2014

Sensata’s Revenue vs Operation Income, 2010-2015

Sensata’s Capital Expenditures, 2004-2014

Sensata’s Revenue by Segment, 2012-2015

Sensata’s Revenue by Region, 2012-2014

Sensata+CST’s Revenue by Application

Sensata’s Sensor Revenue by Type, 2012-2014

Structure of Fuji Electric Electronic Devices Segment

Sales and Operation Income of Electronic Devices Segment, FY2013-FY2015

Sales of Fuji Electric Electronic Devices Segment by Application, FY2013-FY2014

New Products of Fuji Electric Electronic Devices Segment

TDK’s Net Sales, FY2006-FY2015

TDK’s Sales by Segment, FY2014-FY2015

TDK’s Operation Income, FY2006-FY2015

TDK’s R&D Costs, FY2006-FY2015

TDK’s Capex, FY2006-FY2015

TDK’s Sales by application, FY2012-FY2015

TDK’s Passive Components Sales by Application, FY2012-FY2015

Quarterly Sales of TDK by applications, 1Q/FY2015-1Q/FY2016

Quarterly Sales of TDK For Automobiles, 1Q/FY2015-1Q/FY2016

Murata’s Sales and Operation Margin, FY2009-FY2016

Murata’s Sales by product, FY2013-FY2016

Murata’s Major Products

Murata’s sales by Application, FY2013-FY2016

Murata’s Operation Income Bridge, FY2014-FY2015

Murata’s Quarterly Sales, Order and Backlog, 2012Q2-2015Q1

Murata’s Sales by Region, FY2014-FY2015

OEMs and Tier1s’ Intelligent Cockpit Platform (Hardware and Software) Innovation Strategy Research Report, 2026

Intelligent Cockpit Platform Research: multi-dimensional cockpit system architecture reconstruction for multi-agent collaboration and proactive intelligent services

The intelligent cockpit software s...

Automotive AIOS Research Report, 2026

Automotive AIOS Research: Mass Production Solutions Are Implemented

Mass Production Solutions Are Implemented on A Small Scale.

In 2026, AIOS starts small-scale implementation, helping to improve v...

Automotive Telematics Service Provider (TSP) Research Report, 2026

TSP Research: Leading providers collectively turn to AI agents to provide all-scenario active services

Telematics Service Providers (TSPs) are the core hub of the telematics industry chain, connectin...

Automotive Smart Interior Research Report, 2026

Smart Interior Research: As Technologies like Interactive Starlight Headliner, Hidden Display and Surface Projection Are Launched, Automotive Interiors Become Ever More Intelligent

The Automotive Sma...

Research Report on AI Applications in Cockpits, 2026

AI Application in Cockpits: AI Services Become More Comprehensive, Convenient, and Refined.

In the first half of 2026, cockpit AI functions underwent initial upgrades across multiple dimensions, inc...

Software-Defined Vehicles in 2026: OEM Software Development and Supply Chain Deployment Strategy Research Report

Research on OEMs’ Software Strategies: R&D Focus, Development Strategies and Supplier Building Models of 30 OEMs

In this paper, we adopt a research framework covering 13 subsystems and 48 sub-di...

Passenger Car Chassis Domain Control and Chassis Cross-Domain Integration Research Report, 2026

Chassis Control Research: Mass Production of Full Chassis-by-Wire Solutions Starts

1. A Cluster of Full Chassis-by-Wire Solutions Make Their Debut, and EMB Enters Mass Production and Adoption for the...

Central Domain Control (Powertrain, Chassis, Body) and Motion Controller Research Report, 2026

Central Domain Control and Motion Control Research: XYZ Coordinated Control and Full X-by-Wire Actuation System

With the gradual penetration of L3+ autonomous driving, the chassis control system is ...

48V Low-voltage Power Distribution Network (PDN) Architecture and Supply Chain Panorama Research Report, 2026

Research on 48V Low-Voltage Power Distribution Network (PDN): An Active 48V Supply Chain, with Priority Deployment in High-Power Scenarios Such as Steer-by-Wire Chassis

The automotive 48V low-voltage...

AI-Defined Vehicle (AIDV) OEMs' Deployment Strategies Research Report, 2026

AIDV Research: Deployment Strategies of 22 OEMs

The AI-Defined Vehicle (AIDV) OEMs' Deployment Strategies Research Report, 2026, released by ResearchInChina, analyzes the AI deployment strategies of ...

OEMs’ Passenger Car Model Planning Research Report, 2026

Vehicle Model Planning Research: Chinese OEMs Launch Sub-Brands Intensively, While Multinational OEMs Apply the Brakes to Electrification Strategies

ResearchInChina released the OEMs’ Passenger Car M...

Autonomous Driving Simulation and World Model Research Report, 2026

Autonomous driving simulation research: "Simulation test + world model"-driven test system has become R&D infrastructure.

The "Autonomous Driving Simulation and World Model Research Report, 2026"...

Cockpit-Driving Integration Central Domain Controller SoC and AI Supercomputing Architecture Research Report, 2026

Cockpit-Driving integration and AI supercomputing research: The One Chip solution is rapidly installed in vehicles, and AI supercomputing architectures are moving towards full-domain integration.

AI ...

Intelligent Driving End-to-End Large Model Research Report, 2026

Research on Intelligent Driving Large Models: A Critical Period for Technological Competition and Paradigm Integration

As autonomous driving technology rapidly iterates from L2 to L3?L4, intelligent...

Automotive Digital Key Industry Trend Report, 2026

Digital Key Research: Automotive BLE, UWB and SLE Hardware Layout

The Automotive Digital Key Industry Trend Report, 2026, released by ResearchInChina, analyzes and predicts the digital key market, co...

Monthly Report on Automotive New Technology (May 2026)

UHD gaze technology, full-color LiDAR, UWB, etc. promote the upgrade of intelligent driving perception capabilities

This report is published once a month and is available for annual subscription.The...

In-Cabin Monitoring Systems (DMS, OMS, etc.) Research Report, 2026

In-Cabin Monitoring System Research: DMS to Become Mandatory in 2027, Expected to be Installed in Over 14 Million Vehicles

ResearchInChina released the In-Cabin Monitoring Systems (DMS, OMS, etc.) Re...

Automotive Service-Oriented Architecture (SOA) and Cross-Domain Middleware Industry Report, 2026

Research on automotive SOA and cross-domain middleware: The era of AI atomic services and AI cross-domain fusion agents is coming.

Automotive SOA evolves towards AI + full SOA servitization Driv...