ADAS and Autonomous Driving Industry Chain Report 2018 (VII) - L4 Autonomous Driving Startups

ADAS and Autonomous Driving Industry Chain Report 2018 (VII) - L4 Autonomous Driving Startups at 205 pages in length focuses on researching L4 autonomous driving startups as well as HD map and V2X for L4 autonomous driving.

Of the report series (seven reports), the previous five introduce commercialized ADAS, vision, automotive radar, computing platform, system integration, and low-speed autonomous driving which is to be commercially available soon. The last two reports highlight eventually to-be-commercialized commercial vehicle automated driving and L4 passenger car autonomous driving, respectively.

There have long been two camps in the implementation path of automated driving: Camp A mainly comprised of European and Asian OEMs advocates a progressive path evolving from L2 and L3 to L4 and L5 step by step; Camp B represented by Google stands for a radical path going straight to L4 and above.

In 2018, Camp A believes more firmly that L3 cannot be avoided and L2.5 and L2.75 should be derived from between L2 and L3, and L3.5 from between L3 and L4. To secure the reliability of human and computer driving together, it becomes an important subject to monitor human driver.

Camp B is more confident as well, as WAYMO sees its market capitalization climb to USD175 billion and tests tens of thousands of self-driving cars on roads.

The operational design domain (ODD) of WAYMO self-driving car is confined to just hundreds of square kilometers for the moment; L2-L3 self-driving cars at Camp A can travel on most roads. So the two camps will continue to live in peace with each other in the short run.

In July 2018, John Krafcik, WAYMO’s CEO, admitted that it would take a longer time than expected for the prevalence of autonomous vehicles.

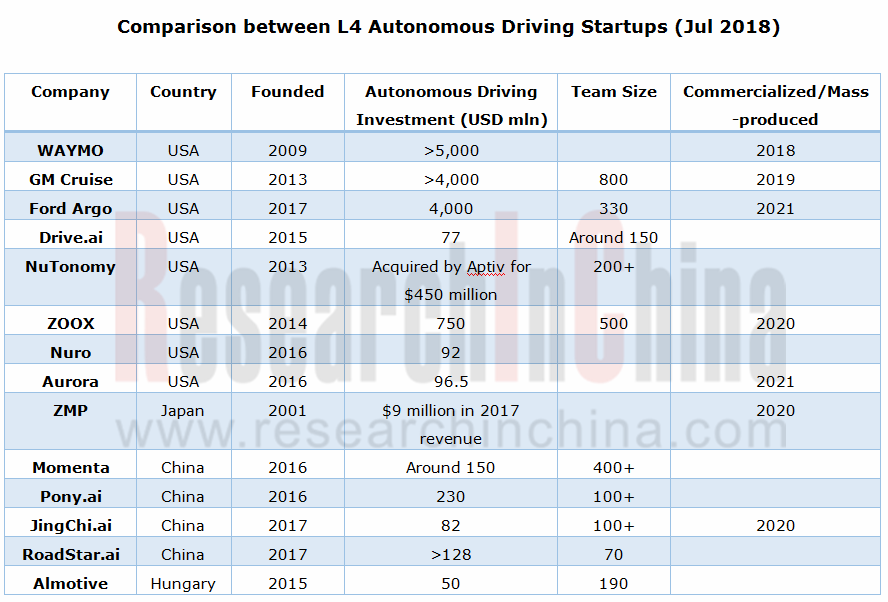

There are at least four technical barriers needing to be surmounted in pushing ahead with L4 from designated scenarios to public roads: first, mass-production of powerful computing platforms; second, stronger sensing capabilities and lower cost of sensors; third, improvement of related technical standards; fourth, inadequate infrastructure. L4 automated driving start-ups will still depend on raised funds to survive in the next two to three years.

We have discussed computing platform and sensor in the previous reports. But L4 development will affect the existing landscape of sensor companies.

Considering too high sensor cost, WAYMO develops by itself all sensor systems it needs, including LiDAR. GM Crusie bought Strobe, a LiDAR company, and Ford Argo acquired Princeton Lightwave, a company engaged in LiDAR. WAYMO can cut 90% cost by developing LiDAR independently; GM Cruise indicates that it can use Strobe’s system to integrate all sensors into one chip, lowering LiDAR cost by 99%.

In addition to sensors, the automated driving leaders also design core computing chips themselves, for example, WAYMO, Tesla and Baidu are all developing their own AI-powered chips.

Singulato, an emerging Chinese automaker indicates that: conventional automotive design is a kind of separate design when it comes to intelligent driving capabilities, that is, separate data cannot be combined for multi-scenario application. In other words, a front ADAS company has a set of sensors of its own and another automated parking company also uses different sensors from others. They cannot share sensor data, which means the waste of resources. Singulato adopts integrated design at the beginning, using same sensors to implement more than a dozen of ADAS functions. And such design also makes subsequent OTA update easier.

Against the backdrop of growing integration, traditional ADAS and sensor companies need to rethink their market orientation in an era of L4.

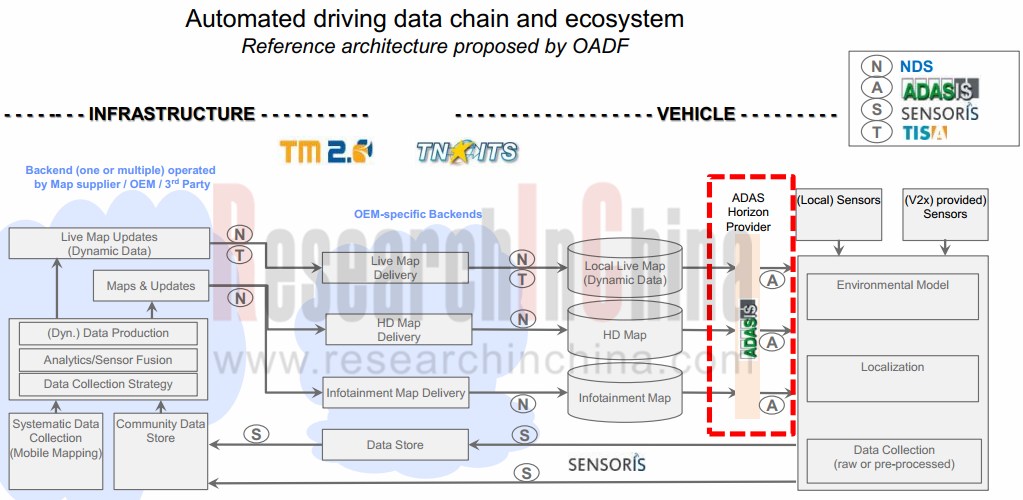

The number of sensors grows to a dozen and even dozens in the evolution from L2 to L4, generating a data traffic surge. Improvement in supporting facilities, mainly a better perception system, includes introduction of HD map and V2X, which also bring about massive data flow. Data confluence of various perception systems make acquisition, fusion and processing of autonomous driving data flow a focus in industrial competition and cooperation.

Absence of a universally accepted standard for acquisition and transmission of sensor (including HD map) data hinders the development of the industry. Hence, standards organizations like ADASIS, SENORIS, SIP-ADUS, CAICV HD MAP WG and ONEMAP have been initiated.

The year 2018 sees continued improvement in autonomous driving industry chain and influx of capital. As the market prospects of L4 become more visible, HD map and V2X, the auxiliaries of L4, are chased by enterprises and capital.

ResearchInChina tries to make an overall view of several hundreds of enterprises in autonomous driving industry and present a full picture of the industry via seven industrial-chain reports, 1,400 pages in total, whilst many problems are found, such as irrational layout, unclear orientation, disconnection from industrial chain, and lack of security policy.

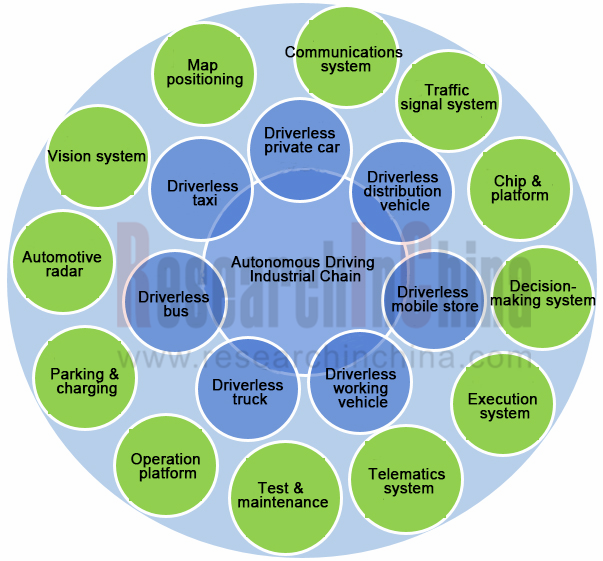

As shown in the following diagram, the autonomous driving industry chain is so complicated that it’s a challenge for any enterprise to have a overall grasp of development trends.

Dozens of times larger than the L2 market, the L4 market will take more than five years to grow mature in China. Tracking autonomous and ICV industry, ResearchInChina will release a weekly report every week and ten monthly reports every month, helping enterprises to see where the industry goes, take in competitive landscape, and seize opportunities in intelligent & connected and autonomous driving markets.

OEMs and Tier1s’ Intelligent Cockpit Platform (Hardware and Software) Innovation Strategy Research Report, 2026

Intelligent Cockpit Platform Research: multi-dimensional cockpit system architecture reconstruction for multi-agent collaboration and proactive intelligent services

The intelligent cockpit software s...

Automotive AIOS Research Report, 2026

Automotive AIOS Research: Mass Production Solutions Are Implemented

Mass Production Solutions Are Implemented on A Small Scale.

In 2026, AIOS starts small-scale implementation, helping to improve v...

Automotive Telematics Service Provider (TSP) Research Report, 2026

TSP Research: Leading providers collectively turn to AI agents to provide all-scenario active services

Telematics Service Providers (TSPs) are the core hub of the telematics industry chain, connectin...

Automotive Smart Interior Research Report, 2026

Smart Interior Research: As Technologies like Interactive Starlight Headliner, Hidden Display and Surface Projection Are Launched, Automotive Interiors Become Ever More Intelligent

The Automotive Sma...

Research Report on AI Applications in Cockpits, 2026

AI Application in Cockpits: AI Services Become More Comprehensive, Convenient, and Refined.

In the first half of 2026, cockpit AI functions underwent initial upgrades across multiple dimensions, inc...

Software-Defined Vehicles in 2026: OEM Software Development and Supply Chain Deployment Strategy Research Report

Research on OEMs’ Software Strategies: R&D Focus, Development Strategies and Supplier Building Models of 30 OEMs

In this paper, we adopt a research framework covering 13 subsystems and 48 sub-di...

Passenger Car Chassis Domain Control and Chassis Cross-Domain Integration Research Report, 2026

Chassis Control Research: Mass Production of Full Chassis-by-Wire Solutions Starts

1. A Cluster of Full Chassis-by-Wire Solutions Make Their Debut, and EMB Enters Mass Production and Adoption for the...

Central Domain Control (Powertrain, Chassis, Body) and Motion Controller Research Report, 2026

Central Domain Control and Motion Control Research: XYZ Coordinated Control and Full X-by-Wire Actuation System

With the gradual penetration of L3+ autonomous driving, the chassis control system is ...

48V Low-voltage Power Distribution Network (PDN) Architecture and Supply Chain Panorama Research Report, 2026

Research on 48V Low-Voltage Power Distribution Network (PDN): An Active 48V Supply Chain, with Priority Deployment in High-Power Scenarios Such as Steer-by-Wire Chassis

The automotive 48V low-voltage...

AI-Defined Vehicle (AIDV) OEMs' Deployment Strategies Research Report, 2026

AIDV Research: Deployment Strategies of 22 OEMs

The AI-Defined Vehicle (AIDV) OEMs' Deployment Strategies Research Report, 2026, released by ResearchInChina, analyzes the AI deployment strategies of ...

OEMs’ Passenger Car Model Planning Research Report, 2026

Vehicle Model Planning Research: Chinese OEMs Launch Sub-Brands Intensively, While Multinational OEMs Apply the Brakes to Electrification Strategies

ResearchInChina released the OEMs’ Passenger Car M...

Autonomous Driving Simulation and World Model Research Report, 2026

Autonomous driving simulation research: "Simulation test + world model"-driven test system has become R&D infrastructure.

The "Autonomous Driving Simulation and World Model Research Report, 2026"...

Cockpit-Driving Integration Central Domain Controller SoC and AI Supercomputing Architecture Research Report, 2026

Cockpit-Driving integration and AI supercomputing research: The One Chip solution is rapidly installed in vehicles, and AI supercomputing architectures are moving towards full-domain integration.

AI ...

Intelligent Driving End-to-End Large Model Research Report, 2026

Research on Intelligent Driving Large Models: A Critical Period for Technological Competition and Paradigm Integration

As autonomous driving technology rapidly iterates from L2 to L3?L4, intelligent...

Automotive Digital Key Industry Trend Report, 2026

Digital Key Research: Automotive BLE, UWB and SLE Hardware Layout

The Automotive Digital Key Industry Trend Report, 2026, released by ResearchInChina, analyzes and predicts the digital key market, co...

Monthly Report on Automotive New Technology (May 2026)

UHD gaze technology, full-color LiDAR, UWB, etc. promote the upgrade of intelligent driving perception capabilities

This report is published once a month and is available for annual subscription.The...

In-Cabin Monitoring Systems (DMS, OMS, etc.) Research Report, 2026

In-Cabin Monitoring System Research: DMS to Become Mandatory in 2027, Expected to be Installed in Over 14 Million Vehicles

ResearchInChina released the In-Cabin Monitoring Systems (DMS, OMS, etc.) Re...

Automotive Service-Oriented Architecture (SOA) and Cross-Domain Middleware Industry Report, 2026

Research on automotive SOA and cross-domain middleware: The era of AI atomic services and AI cross-domain fusion agents is coming.

Automotive SOA evolves towards AI + full SOA servitization Driv...