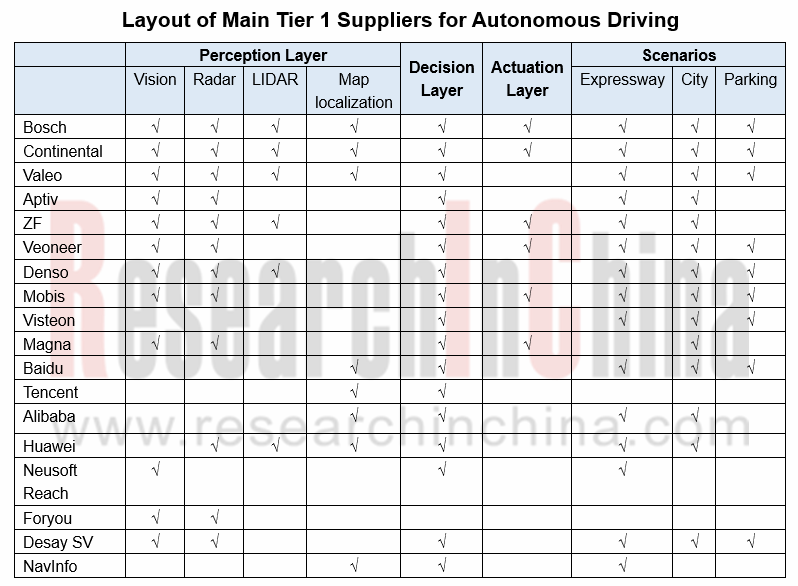

Tier 1 suppliers for autonomous driving: Chinese Tier 1 suppliers have not embarked on the actuation layer, and L3 will spread after 2022

Amid the controversy in L3, some media believe that Audi will give up L3, which is later denied by Audi saying it only elevate the L3 research to Volkswagen Group.

Most OEMs plan to launch L3 models in 2020 except Volvo, Ford and NextEV that will skip L3.

Strictly speaking, the L3 models to be launched by OEMs in 2020 may be prototypes of some high-end models or not real L3 models.

Tier 1 suppliers are not in readiness for large-scale supply to L3 models. Continental, for instance, focuses on L2 + models between 2019 and 2022, and will commercialize L3 models after 2022. Bosch will also begin commercializing the L3 highway pilot (HWP) function after 2022. To increase redundancy of the system, Bosch renders a dual-domain controller architecture to further ensure the system security.

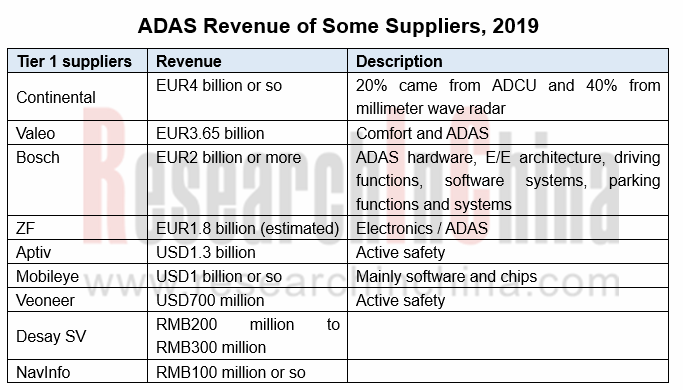

In the realm of autonomous driving, Tier 1 suppliers profit mainly from ADAS. Although Mobileye enjoys the largest market share in terms of ADAS algorithms (including software and chips), it did not secure the highest revenue in 2019 in the ADAS market which also covers control units, millimeter wave radars, map positioning systems, etc.

A case in point is Continental whose ADAS revenue in 2019 posted €4 billion (20% from ADAS domain control unit (ADCU) and 40% from radars).

It can be seen in the table below that Bosch, Continental and Valeo stay ahead by deployments among foreign Tier 1 suppliers, and Huawei deploys most widely in Chinese Tier 1 suppliers.

Chinese Tier 1 suppliers have not embarked on the actuation layer, which is undoubtedly their biggest shortcoming. Without the know-how about actuation technology, they cannot control the autonomous vehicles accurately nor have the initiative. It is expected that they will invest in or acquire related companies in the near future to address inadequacies.

Despite lagged far behind foreign Tier 1 suppliers in the underlying hardware of autonomous driving, Chinese Tier 1 suppliers delve more into application scenarios and V2X than foreign counterparts who usually deploy in expressways, urban roads, and autonomous parking, for the three of which Valeo, for example, launched Cruise4U, Drive4U, Park4U , respectively.

Chinese Tier 1 suppliers have laid out more scenarios. Together with partners, Baidu is present in such scenarios as autonomous cleaning, autonomous agricultural machinery, autonomous shuttles, RoboTaxi, autonomous delivery, autonomous buses, autonomous trucks, and AVP.

Alibaba is pivoted on autonomous logistics vehicle to bolster its e-commerce business.

OEMs and Tier1s’ Intelligent Cockpit Platform (Hardware and Software) Innovation Strategy Research Report, 2026

Intelligent Cockpit Platform Research: multi-dimensional cockpit system architecture reconstruction for multi-agent collaboration and proactive intelligent services

The intelligent cockpit software s...

Automotive AIOS Research Report, 2026

Automotive AIOS Research: Mass Production Solutions Are Implemented

Mass Production Solutions Are Implemented on A Small Scale.

In 2026, AIOS starts small-scale implementation, helping to improve v...

Automotive Telematics Service Provider (TSP) Research Report, 2026

TSP Research: Leading providers collectively turn to AI agents to provide all-scenario active services

Telematics Service Providers (TSPs) are the core hub of the telematics industry chain, connectin...

Automotive Smart Interior Research Report, 2026

Smart Interior Research: As Technologies like Interactive Starlight Headliner, Hidden Display and Surface Projection Are Launched, Automotive Interiors Become Ever More Intelligent

The Automotive Sma...

Research Report on AI Applications in Cockpits, 2026

AI Application in Cockpits: AI Services Become More Comprehensive, Convenient, and Refined.

In the first half of 2026, cockpit AI functions underwent initial upgrades across multiple dimensions, inc...

Software-Defined Vehicles in 2026: OEM Software Development and Supply Chain Deployment Strategy Research Report

Research on OEMs’ Software Strategies: R&D Focus, Development Strategies and Supplier Building Models of 30 OEMs

In this paper, we adopt a research framework covering 13 subsystems and 48 sub-di...

Passenger Car Chassis Domain Control and Chassis Cross-Domain Integration Research Report, 2026

Chassis Control Research: Mass Production of Full Chassis-by-Wire Solutions Starts

1. A Cluster of Full Chassis-by-Wire Solutions Make Their Debut, and EMB Enters Mass Production and Adoption for the...

Central Domain Control (Powertrain, Chassis, Body) and Motion Controller Research Report, 2026

Central Domain Control and Motion Control Research: XYZ Coordinated Control and Full X-by-Wire Actuation System

With the gradual penetration of L3+ autonomous driving, the chassis control system is ...

48V Low-voltage Power Distribution Network (PDN) Architecture and Supply Chain Panorama Research Report, 2026

Research on 48V Low-Voltage Power Distribution Network (PDN): An Active 48V Supply Chain, with Priority Deployment in High-Power Scenarios Such as Steer-by-Wire Chassis

The automotive 48V low-voltage...

AI-Defined Vehicle (AIDV) OEMs' Deployment Strategies Research Report, 2026

AIDV Research: Deployment Strategies of 22 OEMs

The AI-Defined Vehicle (AIDV) OEMs' Deployment Strategies Research Report, 2026, released by ResearchInChina, analyzes the AI deployment strategies of ...

OEMs’ Passenger Car Model Planning Research Report, 2026

Vehicle Model Planning Research: Chinese OEMs Launch Sub-Brands Intensively, While Multinational OEMs Apply the Brakes to Electrification Strategies

ResearchInChina released the OEMs’ Passenger Car M...

Autonomous Driving Simulation and World Model Research Report, 2026

Autonomous driving simulation research: "Simulation test + world model"-driven test system has become R&D infrastructure.

The "Autonomous Driving Simulation and World Model Research Report, 2026"...

Cockpit-Driving Integration Central Domain Controller SoC and AI Supercomputing Architecture Research Report, 2026

Cockpit-Driving integration and AI supercomputing research: The One Chip solution is rapidly installed in vehicles, and AI supercomputing architectures are moving towards full-domain integration.

AI ...

Intelligent Driving End-to-End Large Model Research Report, 2026

Research on Intelligent Driving Large Models: A Critical Period for Technological Competition and Paradigm Integration

As autonomous driving technology rapidly iterates from L2 to L3?L4, intelligent...

Automotive Digital Key Industry Trend Report, 2026

Digital Key Research: Automotive BLE, UWB and SLE Hardware Layout

The Automotive Digital Key Industry Trend Report, 2026, released by ResearchInChina, analyzes and predicts the digital key market, co...

Monthly Report on Automotive New Technology (May 2026)

UHD gaze technology, full-color LiDAR, UWB, etc. promote the upgrade of intelligent driving perception capabilities

This report is published once a month and is available for annual subscription.The...

In-Cabin Monitoring Systems (DMS, OMS, etc.) Research Report, 2026

In-Cabin Monitoring System Research: DMS to Become Mandatory in 2027, Expected to be Installed in Over 14 Million Vehicles

ResearchInChina released the In-Cabin Monitoring Systems (DMS, OMS, etc.) Re...

Automotive Service-Oriented Architecture (SOA) and Cross-Domain Middleware Industry Report, 2026

Research on automotive SOA and cross-domain middleware: The era of AI atomic services and AI cross-domain fusion agents is coming.

Automotive SOA evolves towards AI + full SOA servitization Driv...