Cloud service platform (cloud platform for short) can be interpreted as a scalable platform delivering basic services, middleware, data services, and software services to users over the Internet. Cloud platform is divided into: IaaS (Infrastructure as a Service), PaaS (Platform-as-a-Service), and SaaS (Software-as-a-Service). It is also classified into public cloud, private cloud and hybrid cloud types.

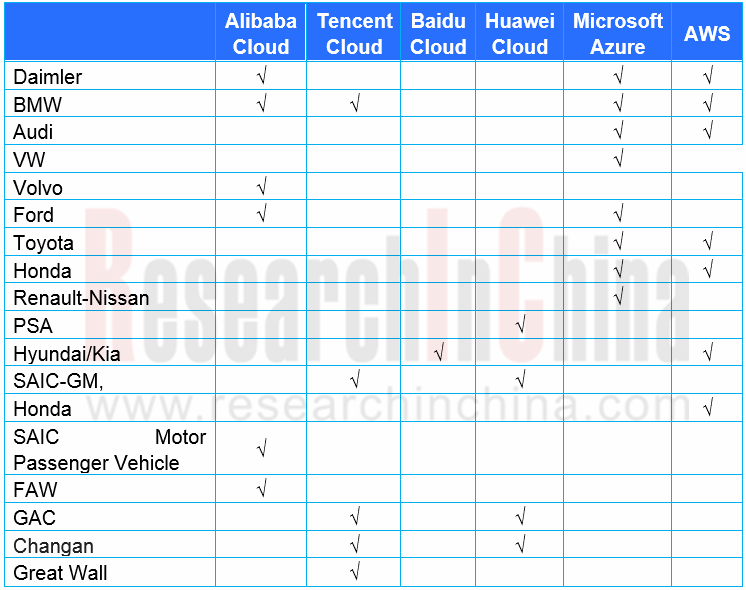

The public cloud platforms incorporate AWS, Microsoft Azure, Alibaba Cloud, Tencent Cloud, Huawei Cloud and Baidu Cloud. There are a large number of private cloud platform providers such as open-source Openstack and varying Openstack-based platforms. Non-open source providers include VMware, Zstack, etc.

Vehicle, infrastructure, cloud and network are crucial elements of cooperative vehicle infrastructure system (CVIS) industry chain. This report highlights the “cloud” link, with emphasis on OEM-centric automotive cloud platform services. With supplier’s cloud platforms as a foundation, OEMs build their own cloud platforms such as marketing & after-sale cloud platform, manufacturing & supply chain cloud platform, telematics cloud platform, autonomous driving cloud platform, simulation cloud platform and HD map cloud platform.

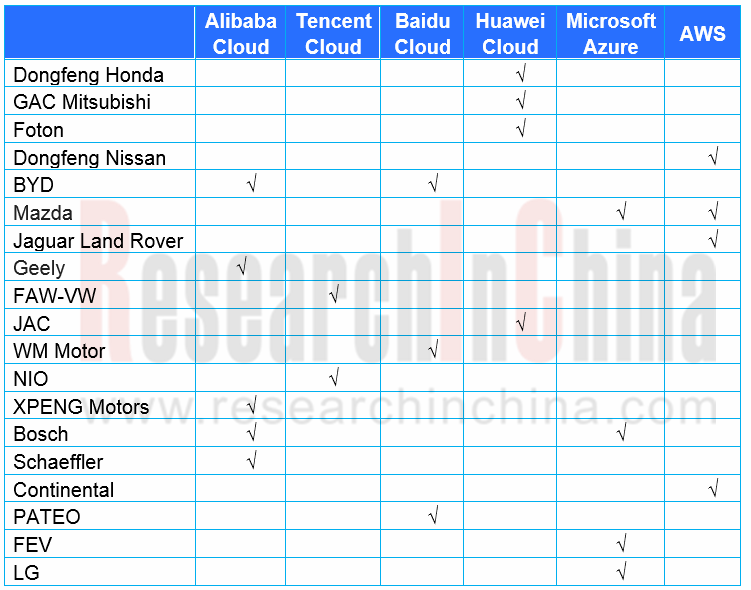

Viewed from the tables above, AWS, Microsoft Azure, Alibaba Cloud, and Tencent Cloud are the first choice of OEMs and Tier1 suppliers. Huawei Cloud and Baidu Cloud are the rising stars. Of both top ten OEMs and top ten Tier1 suppliers that once adopted Amazon Web Services (AWS), more turn to Microsoft Azure as Amazon starts developing and testing autonomous vehicles.

Quite a few OEMs stand on more than one cloud platforms. For instance, Volkswagen Automotive Cloud (vehicles, customers and services) uses Microsoft’s technology, while Volkswagen Industrial Cloud (manufacturing and supply chain management) utilizes Amazon’s.

Telematics cloud platform is among the first automotive cloud platforms already in wide use. In 2017, Microsoft released the Microsoft Connected Vehicle Platform (MCVP), an Azure-based connected automotive platform which has won support from many Tier1 suppliers. The automotive cloud service platform Huawei introduced in 2020 defines more features otherwise: autonomous driving, HD map, battery safety, OTA, V2X and “three powers” (motor, battery and ECU).

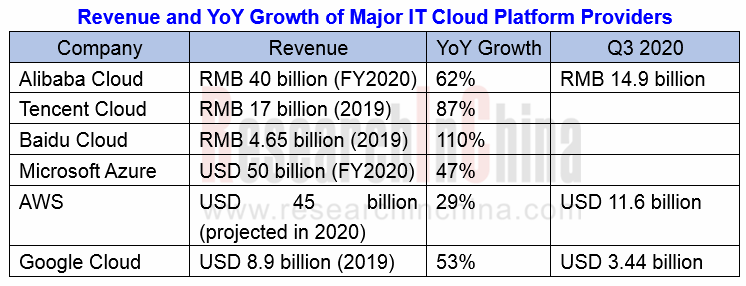

From above it can be clearly seen that IT giants post handsome cloud platform revenues at astounding growth rates, amid the booming demand from automotive sector for cloud services, which is fueled by the following:

(1) Enhancement of automaker’s production management, marketing activities and internal management, and digital revolution and synergy of related industry chains.

(2) Digitalization of the process of automakers’ development, design, test, and validation of software and hardware, and remote R&D teams’ cloud synergy and cloud-based simulation (such as cloud service for firmware simulation).

(3) Digitalization and CASE (Connected, Autonomous, Shared, and Electrified) of automotive products. This means software-defined vehicles, capabilities (e.g., connectivity, navigation, parking, entertainment and payment), and transition from a functional vehicle into an intelligent one cannot be achieved without the support of digitalized process and tools, and cloud services.

(4) Building of the telematics platform for automakers, and the connection, service and operation platform among the four -- car users, automotive products, Internet digital ecosystems, and automakers and their industry chains, providing real-time online mobile interconnected third-space services such as navigation, entertainment and payment, for better user driving experience.

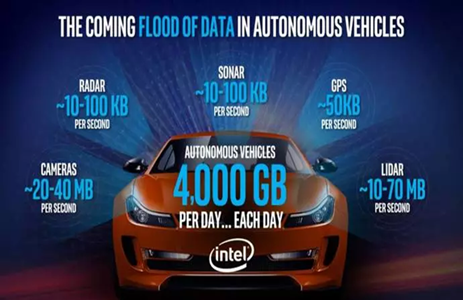

(5) As ADAS/AD gains popularity and gets updated, AVs will generate 4TB data per day, which prompts a surging demand for cloud platform space.

So BAT and Huawei lavish on automotive cloud platform involving operating system, simulation system, telematics system, autonomous driving software, and creation of software and application service ecosystem, considering it is the biggest source of their revenues after all.

OEMs always want to take hold of vehicle data. Currently, leading cloud platform solutions have reserved data ownership of OEMs. For instance, AWS platform retains full ownership of data, while providing functions like machine learning, and special solutions for connectivity and AVs to help OEMs freely create unique brand experience.

Quite a few OEMs set up their own cloud platform subsidiaries and big data centers. Take SAIC Cloud Computing Center as an example. The facility had a 6 or 7-person team, one data center and 5 or 6 cabinets at start and provided just basic cloud storage and IaaS environment. After evolution into Shanghai FinShine Technology Co., Ltd. in 2017, it now boasts a team with 150 talents, three data centers (Shanghai, Nanjing and Zhengzhou) and hundreds of cabinets, and adds software and platform services such as SaaS and PaaS. Up to now the company has owned more than 4,000 cloud hosts, over 10,000 virtual machines or containers, and 30PB storage space.

Companies like SAIC investing heavily in cloud platform still need help from IT tycoons. For example, in 2018, Alibaba Cloud and SAIC together released a hybrid cloud computing service platform for automotive R&D simulation: SSCC (SAIC Simulation Computing Cloud).

To reduce unit costs, IT giants not only build large-scale cloud platforms, but also enable AI algorithms and sundry tool chains and independently develop AI chips. Baidu Cloud, for example, has been a leader in autonomous driving cloud platform field by resorting to competitive DuerOS, Carlife, simulation platform, HD map, autonomous driving algorithms and Kunlun AI chip. OEM’s cloud platform business cannot live without the help of IT firms.

OEMs and Tier1s’ Intelligent Cockpit Platform (Hardware and Software) Innovation Strategy Research Report, 2026

Intelligent Cockpit Platform Research: multi-dimensional cockpit system architecture reconstruction for multi-agent collaboration and proactive intelligent services

The intelligent cockpit software s...

Automotive AIOS Research Report, 2026

Automotive AIOS Research: Mass Production Solutions Are Implemented

Mass Production Solutions Are Implemented on A Small Scale.

In 2026, AIOS starts small-scale implementation, helping to improve v...

Automotive Telematics Service Provider (TSP) Research Report, 2026

TSP Research: Leading providers collectively turn to AI agents to provide all-scenario active services

Telematics Service Providers (TSPs) are the core hub of the telematics industry chain, connectin...

Automotive Smart Interior Research Report, 2026

Smart Interior Research: As Technologies like Interactive Starlight Headliner, Hidden Display and Surface Projection Are Launched, Automotive Interiors Become Ever More Intelligent

The Automotive Sma...

Research Report on AI Applications in Cockpits, 2026

AI Application in Cockpits: AI Services Become More Comprehensive, Convenient, and Refined.

In the first half of 2026, cockpit AI functions underwent initial upgrades across multiple dimensions, inc...

Software-Defined Vehicles in 2026: OEM Software Development and Supply Chain Deployment Strategy Research Report

Research on OEMs’ Software Strategies: R&D Focus, Development Strategies and Supplier Building Models of 30 OEMs

In this paper, we adopt a research framework covering 13 subsystems and 48 sub-di...

Passenger Car Chassis Domain Control and Chassis Cross-Domain Integration Research Report, 2026

Chassis Control Research: Mass Production of Full Chassis-by-Wire Solutions Starts

1. A Cluster of Full Chassis-by-Wire Solutions Make Their Debut, and EMB Enters Mass Production and Adoption for the...

Central Domain Control (Powertrain, Chassis, Body) and Motion Controller Research Report, 2026

Central Domain Control and Motion Control Research: XYZ Coordinated Control and Full X-by-Wire Actuation System

With the gradual penetration of L3+ autonomous driving, the chassis control system is ...

48V Low-voltage Power Distribution Network (PDN) Architecture and Supply Chain Panorama Research Report, 2026

Research on 48V Low-Voltage Power Distribution Network (PDN): An Active 48V Supply Chain, with Priority Deployment in High-Power Scenarios Such as Steer-by-Wire Chassis

The automotive 48V low-voltage...

AI-Defined Vehicle (AIDV) OEMs' Deployment Strategies Research Report, 2026

AIDV Research: Deployment Strategies of 22 OEMs

The AI-Defined Vehicle (AIDV) OEMs' Deployment Strategies Research Report, 2026, released by ResearchInChina, analyzes the AI deployment strategies of ...

OEMs’ Passenger Car Model Planning Research Report, 2026

Vehicle Model Planning Research: Chinese OEMs Launch Sub-Brands Intensively, While Multinational OEMs Apply the Brakes to Electrification Strategies

ResearchInChina released the OEMs’ Passenger Car M...

Autonomous Driving Simulation and World Model Research Report, 2026

Autonomous driving simulation research: "Simulation test + world model"-driven test system has become R&D infrastructure.

The "Autonomous Driving Simulation and World Model Research Report, 2026"...

Cockpit-Driving Integration Central Domain Controller SoC and AI Supercomputing Architecture Research Report, 2026

Cockpit-Driving integration and AI supercomputing research: The One Chip solution is rapidly installed in vehicles, and AI supercomputing architectures are moving towards full-domain integration.

AI ...

Intelligent Driving End-to-End Large Model Research Report, 2026

Research on Intelligent Driving Large Models: A Critical Period for Technological Competition and Paradigm Integration

As autonomous driving technology rapidly iterates from L2 to L3?L4, intelligent...

Automotive Digital Key Industry Trend Report, 2026

Digital Key Research: Automotive BLE, UWB and SLE Hardware Layout

The Automotive Digital Key Industry Trend Report, 2026, released by ResearchInChina, analyzes and predicts the digital key market, co...

Monthly Report on Automotive New Technology (May 2026)

UHD gaze technology, full-color LiDAR, UWB, etc. promote the upgrade of intelligent driving perception capabilities

This report is published once a month and is available for annual subscription.The...

In-Cabin Monitoring Systems (DMS, OMS, etc.) Research Report, 2026

In-Cabin Monitoring System Research: DMS to Become Mandatory in 2027, Expected to be Installed in Over 14 Million Vehicles

ResearchInChina released the In-Cabin Monitoring Systems (DMS, OMS, etc.) Re...

Automotive Service-Oriented Architecture (SOA) and Cross-Domain Middleware Industry Report, 2026

Research on automotive SOA and cross-domain middleware: The era of AI atomic services and AI cross-domain fusion agents is coming.

Automotive SOA evolves towards AI + full SOA servitization Driv...