This report studies autonomous vehicles that transport passengers on short distances, and delves in the product solutions, operational services, and major players in this market.

The development of autonomous shuttles slows down

Many companies, including start-ups, Tier 1 suppliers and automakers (like UISEE, Baidu, Bosch, Continental, Dongfeng, Yutong, etc.), will launch autonomous shuttles when trying to develop and test L4 technology, so as to verify the reliability of their autonomous driving solutions.

Among them, Navya and EasyMile, which are the first to enter the autonomous shuttle market, perform mediocrely.

In fact, the smart sensor configuration of L2+ passenger cars has been developing at an amazing speed, and suppliers such as Baidu have applied L4 technology to the L2+ market. L4 autonomous shuttles have developed slowly in the past two years. Although new players have flooded to the autonomous shuttle market, the development momentum herein is obviously not as good as that of the ADAS market and the autonomous driving market for special vehicles (such as autonomous driving in agriculture, mines and ports).

In terms of sensor configuration, autonomous shuttles lag behind the most cutting-edge passenger cars.

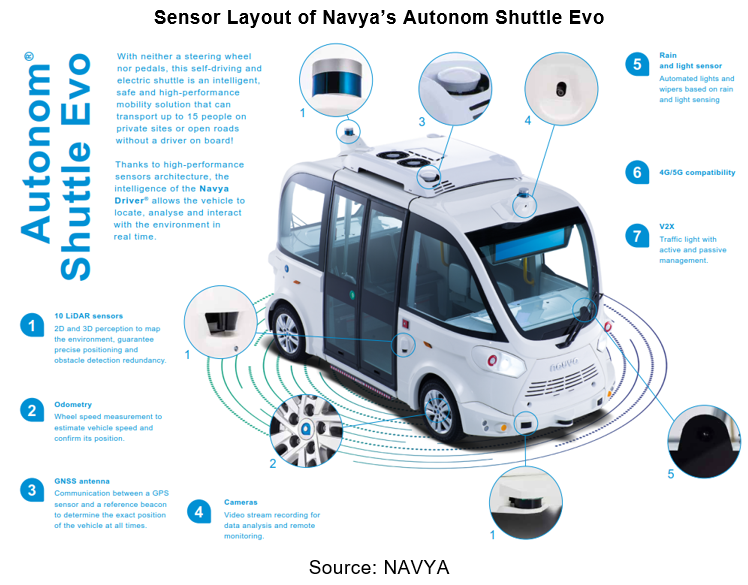

For example, Navya’s autonomous shuttle --- Autonom Shuttle Evo uses a lidar + front/rear view camera solution to enable L4 autonomous driving featuring capabilities such as straight driving, turning, U-turning at intersections, autonomous obstacle avoidance, and fixed site parking. It also supports background remote control.

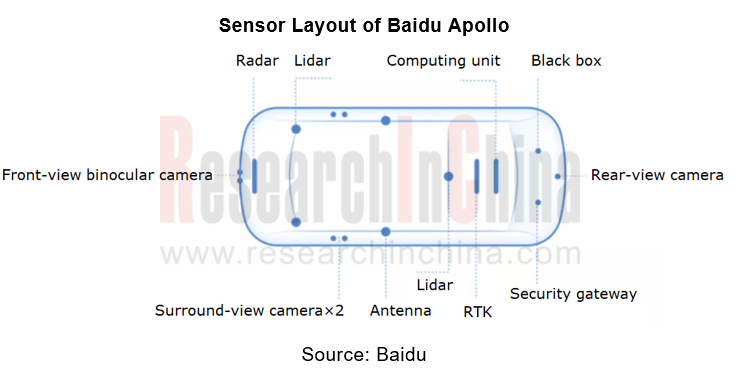

Baidu’s autonomous shuttle Apollo adopts a fusion solution of lidar + radar + front/rear view camera + surround view camera + ultrasonic radar to independently complete a series of driving capabilities such as autonomously exit from parking spaces, following cars, avoiding obstacles, turning/turning around, stopping at stations, etc.

The autonomous shuttle market in China is obviously more booming than abroad

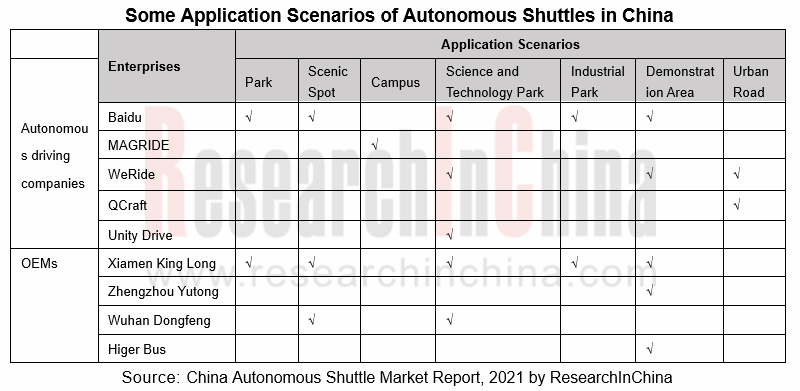

Autonomous shuttles mainly operate in parks, scenic spots, campuses, science and technology parks, industrial parks, demonstration areas and other closed/semi-closed or relatively simple mixed traffic environments, where there are a few vehicles and pedestrians and vehicles run slowly. These scenarios are a good starting point for fast realization and commercialization of autonomous driving.

The autonomous shuttle market in China is obviously more booming than abroad. Baidu’s autonomous shuttles are available in the most scenarios. "Apollo" jointly created by Baidu and Xiamen King Long since 2018 has landed in 35 parks in 28 cities of China. In addition, autonomous driving startups (such as MAGRIDE, WeRide, and QCraft) as well as OEMs (like Xiamen King Long and Zhengzhou Yutong) are actively embarking on this market.

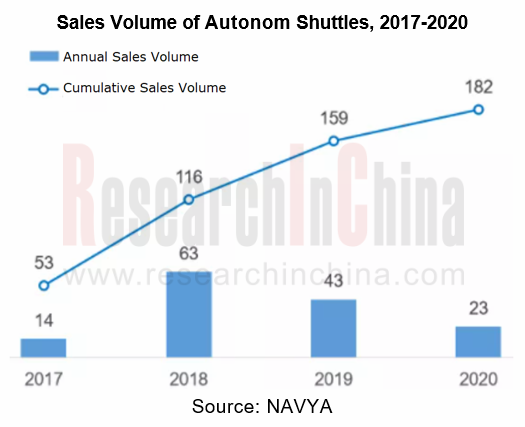

Navya: Global autonomous shuttle sales volume will reach 12,600 units in 2025

The autonomous shuttle market tends to develop more slowly, but it represents a typical scenario for autonomous driving and still attracts more and more players to join. According to the investor report released by Navya in January 2021, the global autonomous shuttle sales volume will reach 12,600 units by 2025, with a market value of EUR1.7 billion.

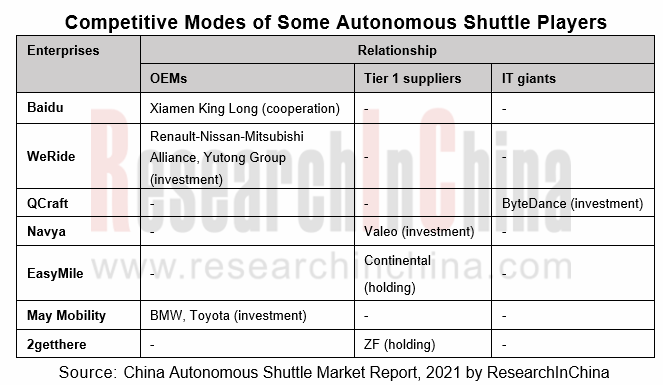

The autonomous shuttle market will thrive sooner or later, but the crucial problem is who can survive the difficult time. At present, autonomous shuttle enterprises are trying to find successful development paths through various forms of cooperation. We have summarized two paths as below.

Path 1: Autonomous shuttle enterprises and OEMs/Tier1s team up to complement advantages

Autonomous shuttle players --- autonomous driving startups, OEMs (buses, passenger cars) and Tier 1 suppliers s have their respective advantages:

- With full-stack layout capabilities in autonomous driving solutions, autonomous driving startups provide L4 autonomous shuttles through OEM cooperation or AM modification.

- Some OEMs use their own vehicle manufacturing capabilities to pre-install and integrate autonomous driving software, algorithms, sensors, etc., and directly embark on actuation.

- The capabilities of Tier1 suppliers in software & hardware layout and system integration cannot be underestimated.

The cooperation between autonomous driving startups, OEMs and Tier1 suppliers is conducive to achieving complementary advantages and enhancing competitiveness.

In March 2021, GM Cruise acquired Voyage, a self-driving car startup that focused on operation in retirement communities. The cooperation will merge Cruise’s engineering and software capabilities with Voyage’s presence in the retirement community market to launch bombshells.

Path 2: Expansion of scenarios and technical service capabilities

Autonomous shuttles have something in common with autonomous logistics vehicles and autonomous taxis in terms of technical solutions, featuring relatively low thresholds to different scenarios.

The French company Navya, which initially engaged in autonomous shuttles, launched Autonom Cab, a driverless taxi, in 2018.

After completing the layout in autonomous taxis, WeRide has dabbled in the autonomous buses and autonomous logistics successively.

In early 2021, WeRide and Yutong jointly built Mini Robobus, and started the normalization test in Guangzhou International Bio Tech Island and Nanjing Eco Hi-Tech Island. Mini Robobus will spread to Zhengzhou, Wuhan and other cities for normalization tests, and it will be commercialized in 2021. Mini Robobus is designed for urban open roads to gradually break the limits of the park scenario and blur the boundary with RoboTaxi.

In March 2021, WeRide acquired MoonX. They will collaborate in business. MoonX, which focuses on autonomous logistics vehicles, is expected to help WeRide realize its expansion in the field of unmanned logistics.

In addition to the above two paths, there must be other paths. Under the background of unclear business models, the expansion, cooperation, mergers and acquisitions of autonomous shuttle companies will occur constantly.

Report on Breakthrough Strategies of OEMs and ADAS Tier 1 Suppliers for Overseas Layout of Intelligent Driving, 2026

Regulatory Breakthrough, Local System Establishment, OEMs Competing for NOA Layout: Overall Trends of China’s Intelligent Driving Overseas Layout in 2026

Research on overseas intelligent driving layo...

OEMs and Tier1s’ Intelligent Cockpit Platform (Hardware and Software) Innovation Strategy Research Report, 2026

Intelligent Cockpit Platform Research: multi-dimensional cockpit system architecture reconstruction for multi-agent collaboration and proactive intelligent services

The intelligent cockpit software s...

Automotive AIOS Research Report, 2026

Automotive AIOS Research: Mass Production Solutions Are Implemented

Mass Production Solutions Are Implemented on A Small Scale.

In 2026, AIOS starts small-scale implementation, helping to improve v...

Automotive Telematics Service Provider (TSP) Research Report, 2026

TSP Research: Leading providers collectively turn to AI agents to provide all-scenario active services

Telematics Service Providers (TSPs) are the core hub of the telematics industry chain, connectin...

Automotive Smart Interior Research Report, 2026

Smart Interior Research: As Technologies like Interactive Starlight Headliner, Hidden Display and Surface Projection Are Launched, Automotive Interiors Become Ever More Intelligent

The Automotive Sma...

Research Report on AI Applications in Cockpits, 2026

AI Application in Cockpits: AI Services Become More Comprehensive, Convenient, and Refined.

In the first half of 2026, cockpit AI functions underwent initial upgrades across multiple dimensions, inc...

Software-Defined Vehicles in 2026: OEM Software Development and Supply Chain Deployment Strategy Research Report

Research on OEMs’ Software Strategies: R&D Focus, Development Strategies and Supplier Building Models of 30 OEMs

In this paper, we adopt a research framework covering 13 subsystems and 48 sub-di...

Passenger Car Chassis Domain Control and Chassis Cross-Domain Integration Research Report, 2026

Chassis Control Research: Mass Production of Full Chassis-by-Wire Solutions Starts

1. A Cluster of Full Chassis-by-Wire Solutions Make Their Debut, and EMB Enters Mass Production and Adoption for the...

Central Domain Control (Powertrain, Chassis, Body) and Motion Controller Research Report, 2026

Central Domain Control and Motion Control Research: XYZ Coordinated Control and Full X-by-Wire Actuation System

With the gradual penetration of L3+ autonomous driving, the chassis control system is ...

48V Low-voltage Power Distribution Network (PDN) Architecture and Supply Chain Panorama Research Report, 2026

Research on 48V Low-Voltage Power Distribution Network (PDN): An Active 48V Supply Chain, with Priority Deployment in High-Power Scenarios Such as Steer-by-Wire Chassis

The automotive 48V low-voltage...

AI-Defined Vehicle (AIDV) OEMs' Deployment Strategies Research Report, 2026

AIDV Research: Deployment Strategies of 22 OEMs

The AI-Defined Vehicle (AIDV) OEMs' Deployment Strategies Research Report, 2026, released by ResearchInChina, analyzes the AI deployment strategies of ...

OEMs’ Passenger Car Model Planning Research Report, 2026

Vehicle Model Planning Research: Chinese OEMs Launch Sub-Brands Intensively, While Multinational OEMs Apply the Brakes to Electrification Strategies

ResearchInChina released the OEMs’ Passenger Car M...

Autonomous Driving Simulation and World Model Research Report, 2026

Autonomous driving simulation research: "Simulation test + world model"-driven test system has become R&D infrastructure.

The "Autonomous Driving Simulation and World Model Research Report, 2026"...

Cockpit-Driving Integration Central Domain Controller SoC and AI Supercomputing Architecture Research Report, 2026

Cockpit-Driving integration and AI supercomputing research: The One Chip solution is rapidly installed in vehicles, and AI supercomputing architectures are moving towards full-domain integration.

AI ...

Intelligent Driving End-to-End Large Model Research Report, 2026

Research on Intelligent Driving Large Models: A Critical Period for Technological Competition and Paradigm Integration

As autonomous driving technology rapidly iterates from L2 to L3?L4, intelligent...

Automotive Digital Key Industry Trend Report, 2026

Digital Key Research: Automotive BLE, UWB and SLE Hardware Layout

The Automotive Digital Key Industry Trend Report, 2026, released by ResearchInChina, analyzes and predicts the digital key market, co...

Monthly Report on Automotive New Technology (May 2026)

UHD gaze technology, full-color LiDAR, UWB, etc. promote the upgrade of intelligent driving perception capabilities

This report is published once a month and is available for annual subscription.The...

In-Cabin Monitoring Systems (DMS, OMS, etc.) Research Report, 2026

In-Cabin Monitoring System Research: DMS to Become Mandatory in 2027, Expected to be Installed in Over 14 Million Vehicles

ResearchInChina released the In-Cabin Monitoring Systems (DMS, OMS, etc.) Re...