Global and China Automotive Millimeter-wave (MMW) Radar Industry Report, 2020-2021

Our Global and China Automotive Millimeter-wave (MMW) Radar Industry Report, 2020-2021 combs through and summarizes the characteristics of the global and China passenger car radar markets, related enterprises’ characteristics, development trends and so forth. In the years to come, ADAS functions upgrade, new cockpit applications (e.g., life signs monitoring), and 4D radar launches will combine to drive up the demand for automotive radars.

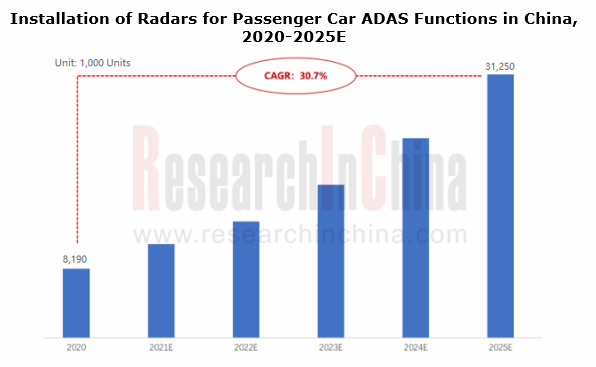

In 2025, China passenger car ADAS functions will carry more than 31 million radars, with demand AAGR of 30.7%.

In 2020, a total of 8.19 million radars were installed in passenger cars in China, including 4.77 million front view radars and 3.31 million rear angle radars. These radars were demanded by front and side road environment detections among L1-L2 ADAS functions.

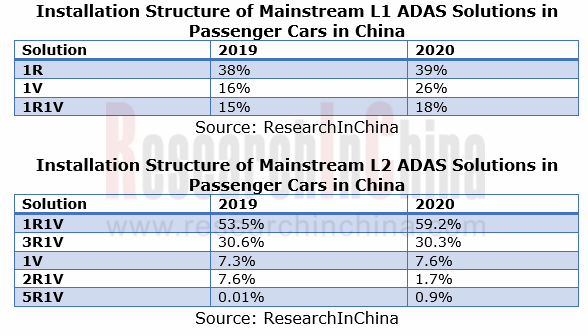

From current mainstream ADAS system solutions, it can be seen that L1 depends on 1R, 1V or 1R1V solution that features simple perception strategy and needs a limited number of radars; L2 needs more radars for requiring a higher level of sensor fusion. Noticeably, the use of 5R1V in vehicles in 2020 provided a further boost to the radar demand.

In a word, the increasing number of sensors per autonomous vehicle is accompanied by ADAS functions upgrade. It is estimated that passenger cars in China will be equipped with over 31 million radars in 2025.

The growth in the demand is expected to follow such trajectory:

- The upgrade from L1 to L2/L3 will demand 3 or 5 radars;

- For L4/L5, single vehicle may need 7 or even more radars (deployed at both sides of vehicle body);

- ADAS upgrade will fuel the demand for front view radars at first, and then rear angle ones;

- The front view radar + rear angle radar solution is becoming a basic configuration, and the increasing demand for front view radars comes with the launch of L3 functions.

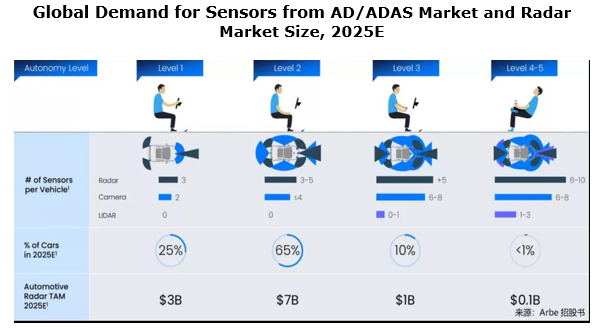

The following picture shows Arbe’s prediction about the demand for various sensors from ADAS in 2025. Arbe argues that in five years, L1 ADAS will be configured with 3 radars, L3 with over 5, and L4-L5 possibly even with as many as 6 to 10. Arbe expresses obvious optimism about the demand for radars.

Cockpit applications like vital signs monitoring and gesture control are expected to be a new engine to the radar growth.

As intelligent cockpit evolves, radars are finding their way into new areas. Currently, they are largely used in cockpits for vital signs monitoring and gesture control.

A. Vital signs monitoring: Wuhu Sensortech Intelligent Technology Co., Ltd. (WHST) was the first one to achieve mass-production

At present, in-vehicle monitoring mainly adopts cameras which invade privacy, while radars can ease the concern. In April 2020, HYCAN 007, a mass-produced model under the brand co-created by GAC and NIO became available on market, which also means the mass production of STA79-4, WHST’s automotive radar used in the car for vital signs monitoring.

In June 2020, at its “Online Launch of Vital Signs Monitoring Technology”, Great Wall Motor also used STA79-4 for vital signs monitoring in vehicle. The solution has been mounted on 2021 WEY VV6.

B. Gesture control: the foreign vendor Acconeer and China’s WHST are exploring.

In-vehicle gesture control is currently enabled using cameras, but the technology requires ultrahigh accuracy devices. 60GHz radar that features up to 7GHz bandwidth for sub-micron resolution required by gesture control becomes a new option for cockpit gesture control. More than that, 60GHz radar can penetrate materials to transmit signals, and the integrated design makes it more compact enough to be hidden inside the housing of a device.

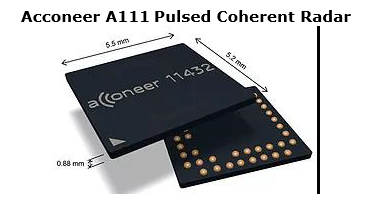

In 2018, Sweden-based Acconeer rolled out A111, a 60GHz pulsed coherent radar applicable to vehicles for smoothly controlling the vehicle functions to be actuated. Furthermore, it can be applied widely in areas from robots and drones, and mobile and wearable devices to Internet of Things, power tools and industry, healthcare and fitness. In automobiles, it is often used for gesture recognition and safety alert.

4D radars being installed in vehicles enjoys a rosy prospect.

4D radar outperforms a 3D one in the following three aspects:

(1) Detect “height”, for example, distinguishing an overpass from vehicles on the road;

(2) Offer higher resolution: 1-degree angular resolution (even lower in the case of super resolution algorithm) in both azimuth and elevation;

(3) Classify static obstacles, able to detect roadside obstacles and small targets, e.g., water bottles and tire fragments.

The unique edge ensures 4D radars to work better in detection of static obstacles and support L3-L5 highly automated driving. As for its application scenarios, 4D radars will be massively seen in ADAS front view function in future to replace some few-channel LiDARs, expectedly becoming a “new star” in radar market.

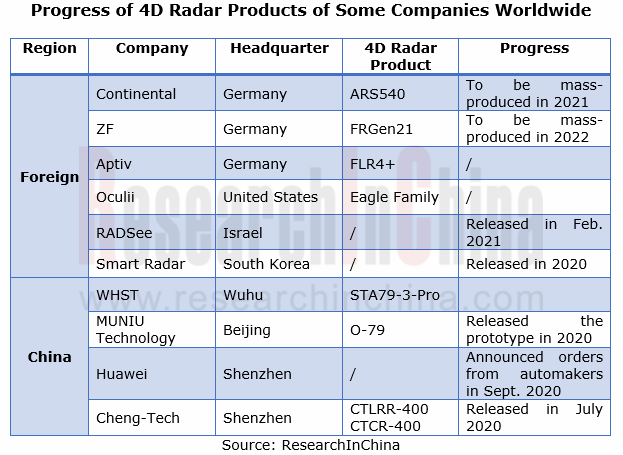

Current foreign 4D radar vendors are divided into two types: conventional Tier1 suppliers like Continental, Aptiv and ZF; start-ups, typically Arbe, Oculii and Vayyar.

Chinese players such as WHST, MUNIU Technology and Huawei, started late but gather pace.

The curtain on the mass-production of 4D radars has been lifted. Continental ARS540 ordered by BMW is to be spawned in 2021; ZF 4D radar mounted on SAIC R ES33 will be produced in quantity in 2022.

In March 2021, SAIC R Brand showcased ES33, its new model of strategic importance. 2 ZF 4D radars are installed at the front bumper of the car, affording an over 300m detection range. Besides, ES33 also bears 31 other perception hardware devices including 1 LiDAR and 12 cameras, hoping to enable L3-L4 automated driving.

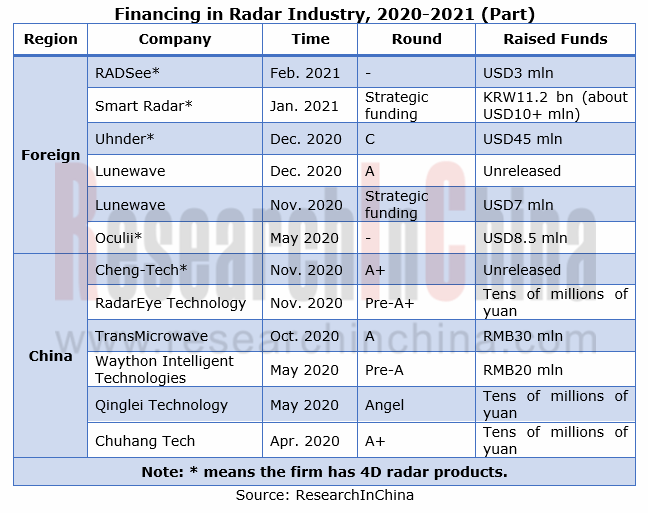

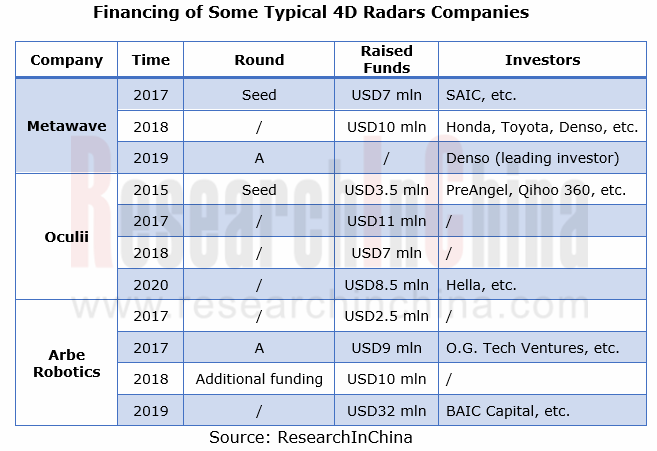

As well as OEMs welcoming 4D radar, capital favors it, too. Since 2020, the financing for nearly 50% start-ups in radar industry has gone to 4D radar.

Also, some traditional OEMs and Tier1 suppliers bet on 4D radars in recent years. For example, SAIC, Honda, Toyota and Denso invested in Metawave between 2017 and 2019; BAIC participated in the USD32 million funding round Arbe closed in 2019; in 2020, Hella was an investor in Oculii’s USD8.5 million strategic funding round.

Research Report on AI Applications in Cockpits, 2026

AI Application in Cockpits: AI Services Become More Comprehensive, Convenient, and Refined.

In the first half of 2026, cockpit AI functions underwent initial upgrades across multiple dimensions, inc...

Software-Defined Vehicles in 2026: OEM Software Development and Supply Chain Deployment Strategy Research Report

Research on OEMs’ Software Strategies: R&D Focus, Development Strategies and Supplier Building Models of 30 OEMs

In this paper, we adopt a research framework covering 13 subsystems and 48 sub-di...

Passenger Car Chassis Domain Control and Chassis Cross-Domain Integration Research Report, 2026

Chassis Control Research: Mass Production of Full Chassis-by-Wire Solutions Starts

1. A Cluster of Full Chassis-by-Wire Solutions Make Their Debut, and EMB Enters Mass Production and Adoption for the...

Central Domain Control (Powertrain, Chassis, Body) and Motion Controller Research Report, 2026

Central Domain Control and Motion Control Research: XYZ Coordinated Control and Full X-by-Wire Actuation System

With the gradual penetration of L3+ autonomous driving, the chassis control system is ...

48V Low-voltage Power Distribution Network (PDN) Architecture and Supply Chain Panorama Research Report, 2026

Research on 48V Low-Voltage Power Distribution Network (PDN): An Active 48V Supply Chain, with Priority Deployment in High-Power Scenarios Such as Steer-by-Wire Chassis

The automotive 48V low-voltage...

AI-Defined Vehicle (AIDV) OEMs' Deployment Strategies Research Report, 2026

AIDV Research: Deployment Strategies of 22 OEMs

The AI-Defined Vehicle (AIDV) OEMs' Deployment Strategies Research Report, 2026, released by ResearchInChina, analyzes the AI deployment strategies of ...

OEMs’ Passenger Car Model Planning Research Report, 2026

Vehicle Model Planning Research: Chinese OEMs Launch Sub-Brands Intensively, While Multinational OEMs Apply the Brakes to Electrification Strategies

ResearchInChina released the OEMs’ Passenger Car M...

Autonomous Driving Simulation and World Model Research Report, 2026

Autonomous driving simulation research: "Simulation test + world model"-driven test system has become R&D infrastructure.

The "Autonomous Driving Simulation and World Model Research Report, 2026"...

Cockpit-Driving Integration Central Domain Controller SoC and AI Supercomputing Architecture Research Report, 2026

Cockpit-Driving integration and AI supercomputing research: The One Chip solution is rapidly installed in vehicles, and AI supercomputing architectures are moving towards full-domain integration.

AI ...

Intelligent Driving End-to-End Large Model Research Report, 2026

Research on Intelligent Driving Large Models: A Critical Period for Technological Competition and Paradigm Integration

As autonomous driving technology rapidly iterates from L2 to L3?L4, intelligent...

Automotive Digital Key Industry Trend Report, 2026

Digital Key Research: Automotive BLE, UWB and SLE Hardware Layout

The Automotive Digital Key Industry Trend Report, 2026, released by ResearchInChina, analyzes and predicts the digital key market, co...

Monthly Report on Automotive New Technology (May 2026)

UHD gaze technology, full-color LiDAR, UWB, etc. promote the upgrade of intelligent driving perception capabilities

This report is published once a month and is available for annual subscription.The...

In-Cabin Monitoring Systems (DMS, OMS, etc.) Research Report, 2026

In-Cabin Monitoring System Research: DMS to Become Mandatory in 2027, Expected to be Installed in Over 14 Million Vehicles

ResearchInChina released the In-Cabin Monitoring Systems (DMS, OMS, etc.) Re...

Automotive Service-Oriented Architecture (SOA) and Cross-Domain Middleware Industry Report, 2026

Research on automotive SOA and cross-domain middleware: The era of AI atomic services and AI cross-domain fusion agents is coming.

Automotive SOA evolves towards AI + full SOA servitization Driv...

Automotive Display, Center Console and Cluster Industry Report, 2026

Automotive Display Research: Multi-Screen Application Slows Down, While OLED and MiniLED Are Introduced in Vehicles Quickly

In 2026, automotive displays will no longer excessively pursue the number a...

Global and China Intelligent Vehicle Standard System Construction and Certification Research Report, 2026

Intelligent Driving Standards and Certification: With the Maturing Standardization System, China Will Participate in Formulation of Global Standards

China's automotive industry is transforming from ...

Automotive Intelligent Diagnosis Industry Report, 2026

Automotive Intelligent Diagnosis Research: Powered by AI, Remote Diagnosis Is Being Upgraded towards Intelligence.

ResearchInChina released the Automotive Intelligent Diagnosis Industry Report, 2026....

Automotive Cloud Service Platform Research Report, 2026

Research on automotive cloud service platform: with architecture upgrade and computing power improvement, cloud services enter a new stage

In 2026, the Internet of Vehicles industry generates petaby...