In April 2021, Waymo’s CEO and CFO left the company. In addition, the Chief Safety Officer, head of manufacturing and global supply and general manager of Laser Bear LiDAR business, head of Automotive Partnerships and Corporate Development have also resigned since late 2020.

Waymo’s L4 development model has been set back. Its efforts to develop L4 with the model of “refitted vehicles—road test data collection—trial operation” hit a bottleneck, while companies like Tesla, Mobileye and Momenta adopt the widely-accepted “shadow model” where the data collected by L2 mass-produced vehicles are used to train a L4 algorithm model.

Except for few companies like Waymo and Uber which perform worse than expected, L4 autonomous driving firms in other fields gain momentum. Favored by capital in 2021, they make big strikes in technology and cost reduction, making a thriving market. As the saying goes, a thousand sails pass by the wrecked ship, and ten thousand saplings shoot up beyond the withered tree.

L4 autonomous driving firms are in capital’s good graces.

During 2020-2021, the global L4 autonomous driving industry has seen a turning point: bellwethers such as Waymo and Cruise vie for more competitive edges in Robotaxi; Uber sold its autonomous driving business to Aurora and invested USD400 million in it; technology giants like Huawei and Baidu deploy dimension reduction application of L4 autonomous driving for commercialization; WeRide and Didi Woya each have raised hundreds of millions of US dollars in 2021.

Although several of its executives have left since 2021, Waymo still raised USD2.5 billion in a new round funding in June 2021. Moreover, GM Cruise has also raised USD2.75 billion in 2021. After bouncing several times, Origin, GM Cruise’s first autonomous robotaxi design, is projected to enter volume production in early 2023.

In 2021, L4 start-ups usher in a funding boom. TuSimple, a Chinese autonomous truck manufacturer listed its shares in the US, which took its market capitalization to more than USD10 billion. The sought-after company announced to secure orders for 6,500 units of its autonomous trucks. Its domestic peer PlusAI was listed on the New York Stock Exchange by way of special purpose acquisition company (SPAC). This signals L4 autonomous driving companies have been in the new phase of rapid development. There will be more L4 autonomous driving companies going public.

Cost reduction” and “dimension reduction application” bring development opportunities to L4 autonomous driving companies.

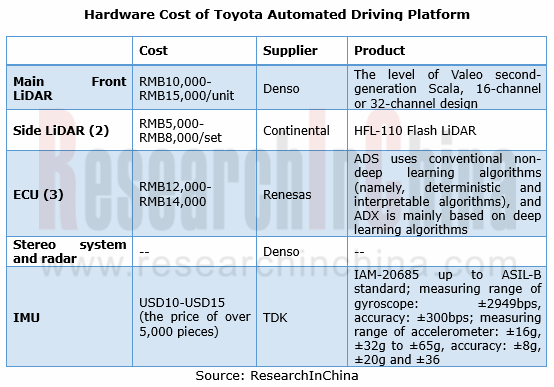

Too high cost has been an inevitable practical challenge in commercialization of L4 autonomous driving. The hardware devices for a L4 autonomous vehicle generally include: 6-12 cameras, 3-12 radars, 1-3 LiDARs, 2 GNSSs/IMUs and 2 computing platforms (including the redundant one). As the technology advances, the cost of hardware is on the decline.

On one estimate, the cost of hardware for a set of L4 autonomous driving system of Toyota is RMB40,000 or so. Wherein, the main front LiDAR costs the most, roughly RMB10,000 to RMB15,000; the combined cost of the two side LiDARs stands at RMB5,000 to RMB8,000; that of the 3 ECUs is RMB12,000 to RMB14,000. The dilution of software cost is accompanied by the rising sales.

In China, Baidu introduced Apollo Moon, its new-generation mass-produced Robotaxi in June 2021, with cost expected to be slashed to RMB480,000, a third of that of current L4 mass-produced autonomous models. The ARCFOX αT-refitted vehicle adopts the ANP-Robotaxi architecture, and packs 13 cameras, 1 LiDAR, 5 radars and Baidu's self-developed central computing platform with computing force up to 800TOPS.

In July 2021, GAC AION and Huawei launched the cooperative project AH8 model, their first co-developed large-sized intelligent full-electric SUV based on GAC GEP3.0 Chassis Platform and Huawei Computing and Communication Architecture (CCA). The L4 autonomous car is projected to be spawned in late 2023.

As costs go down, we predict RMB300,000 autonomous vehicles with L4 autonomy will come out in the next 2 or 3 years.

At present, L4 autonomous driving technology has yet to mature. Multiple automakers and technology providers have started dimension reduction application. AVP tends to be a key L4 autonomous driving technology deployed on mass-produced vehicles. For example, starting from AVP, Baidu will progressively achieve driving automation of passenger cars in all scenarios.

In January 2021, Weltmeister W6, a Baidu AVP-enabled mass-produced L4 model, rolled off the assembly line. As the world’s first model of such kind, the car carries 5 cameras, 12 ultrasonic radars and Baidu's autonomous driving computing platform ACU. The AVP solution consists of just cameras and ultrasonic radars, making its cost available.

In July 2021, Baidu and Great Wall Motor built in-depth cooperation on AVP. They plan to equip WEY Mocha with Baidu AVP that is based on Apollo software algorithms and up to ASIL-B functional safety standard, enabling L4 autonomous parking within visual range. It is predicted that the new model is about to be launched on market in the second half of 2021.

In addition, the auto parts giant ZF also tries hard to deploy AVP, in hope of developing future-oriented autonomous driving technologies with AVP as a starting point. In April 2021, ZF first released its AVP technology which enables automated parking via CalmCar 360° surround view perception and ultrasonic radars; in June, ZF led a USD150 million C round financing for CalmCar. They have forged a strategic partnership to develop a cost-effective AVP system, and plan to use it in mass-produced models of OEMs in China in 2022.

L4 autonomous driving for commercial vehicles enters the phase of cross-scenario mass production and application.

The demission of John Krafcik, Google Waymo’s CEO, becomes a watershed in the industry. It indicates that it is hard to achieve commercial operation of L4 autonomous driving in real terms by depending on tests and verifications in ideal conditions. Given this, large companies have started developing multi-scenario application solutions to amass data and iterate algorithms in actual operating scenarios.

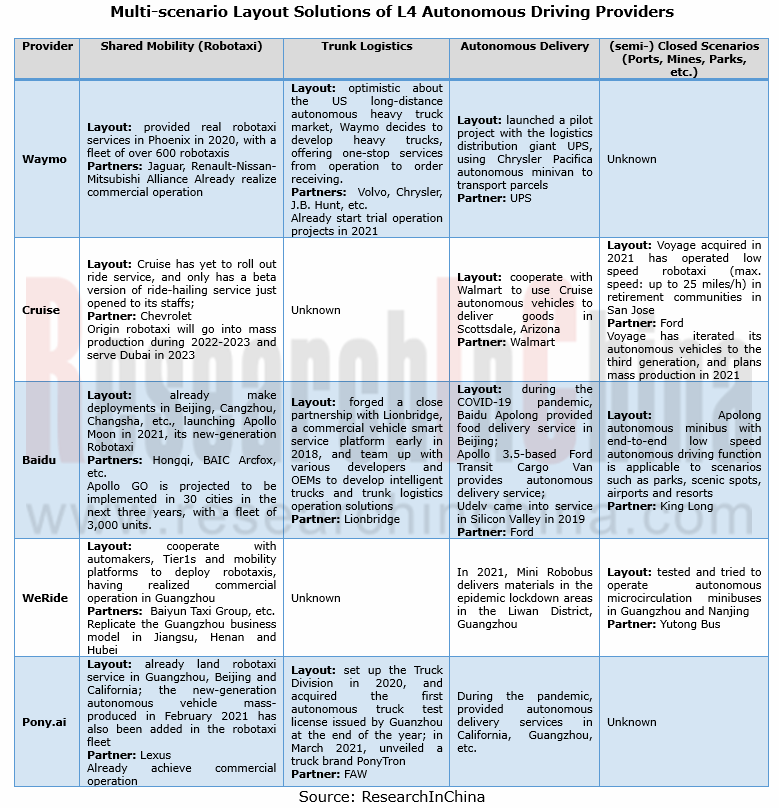

In the near future, L4 autonomous driving layout will target designated scenarios, especially shared mobility, trunk logistics, autonomous delivery, and (semi-) closed scenarios.

L4 autonomous driving providers are working hard on application of the technology in different scenarios. Examples include Baidu Apollo with technical expertise in Robotaxi, autonomous minibus and autonomous parking, and providers like Waymo and Pony.ai which turn to autonomous logistics and delivery from Robotaxi.

Waymo: by the end of 2020, Waymo has boasted a fleet of more than 600 Robotaxi. In 2021, Waymo plans to introduce a fleet of 100 Jaguar I-PACE autonomous vehicles equipped with the latest fifth-generation software and hardware.

In terms of autonomous commercial vehicles, following its in-depth cooperation with Volvo in 2020, Waymo partnered closely with Fiat Chrysler Automobiles (FCA) to manufacture autonomous commercial trucks, and introduced Waymo Via trucking service tested on roads in two states of the US.

Motional: in March 2020, Hyundai and Aptiv set up a joint venture, a L4/L5 autonomous vehicle developer that integrated the resources of NuTonomy. The founding of this joint venture noticeably quickened their pace of deploying autonomous driving.

In October 2020, Motional and Lyft announced the resumption of their self-driving mobility service in Las Vegas; in March 2021, Motional indicated it will select Ambarella CVflow? SoC family for its autonomous vehicles; in June 2021, Motional said it will launch nuPlan, an extended public dataset.

Pony.ai: in February 2021, Pony.ai’s first Robotaxis with the latest system rolled off its standard production line; in April 2021, Pony.ai upgraded PonyPliot+ Robotaxi service in all aspects; in May 2021, the Robotaxi service was landed in Yizhuang, Beijing.

As for autonomous commercial vehicles, Pony.ai set up its Truck Division in 2020 and acquired its first autonomous truck test license issued by Guangzhou at the end of the year; in March 2021, it introduced its truck brand—PonyTron.

Although the whole highly automated driving industry still faces a range of challenges such immature supply chain, very high cost, not enough safety, and unsound laws and regulations, and needs some time for commercial application in all scenarios, L4 autonomous driving technology is getting rapid upgrade and the overall cost is dropping, which makes the commercial use in designated scenarios an expectation.

Our Global and China L4 Autonomous Driving and Start-ups Report, 2021 highlights the following:

Autonomous driving industry (main technologies, status quo of autonomous driving test, investment and financing, policies, standards, etc.);

Autonomous driving industry (main technologies, status quo of autonomous driving test, investment and financing, policies, standards, etc.);

L4 autonomous driving market (size, competitive pattern, technology trends, etc.);

Development of L4 autonomous driving technologies (computing platform, high-precision positioning, etc.) in China (technical solutions of providers, mass production plans of OEMs, etc.);

Implementation of L4 autonomous driving (business models, main application scenarios (Robotaxi, autonomous delivery, etc.), etc.);

Main Chinese and foreign L4 autonomous driving technology providers (layout, application, etc.).

OEMs and Tier1s’ Intelligent Cockpit Platform (Hardware and Software) Innovation Strategy Research Report, 2026

Intelligent Cockpit Platform Research: multi-dimensional cockpit system architecture reconstruction for multi-agent collaboration and proactive intelligent services

The intelligent cockpit software s...

Automotive AIOS Research Report, 2026

Automotive AIOS Research: Mass Production Solutions Are Implemented

Mass Production Solutions Are Implemented on A Small Scale.

In 2026, AIOS starts small-scale implementation, helping to improve v...

Automotive Telematics Service Provider (TSP) Research Report, 2026

TSP Research: Leading providers collectively turn to AI agents to provide all-scenario active services

Telematics Service Providers (TSPs) are the core hub of the telematics industry chain, connectin...

Automotive Smart Interior Research Report, 2026

Smart Interior Research: As Technologies like Interactive Starlight Headliner, Hidden Display and Surface Projection Are Launched, Automotive Interiors Become Ever More Intelligent

The Automotive Sma...

Research Report on AI Applications in Cockpits, 2026

AI Application in Cockpits: AI Services Become More Comprehensive, Convenient, and Refined.

In the first half of 2026, cockpit AI functions underwent initial upgrades across multiple dimensions, inc...

Software-Defined Vehicles in 2026: OEM Software Development and Supply Chain Deployment Strategy Research Report

Research on OEMs’ Software Strategies: R&D Focus, Development Strategies and Supplier Building Models of 30 OEMs

In this paper, we adopt a research framework covering 13 subsystems and 48 sub-di...

Passenger Car Chassis Domain Control and Chassis Cross-Domain Integration Research Report, 2026

Chassis Control Research: Mass Production of Full Chassis-by-Wire Solutions Starts

1. A Cluster of Full Chassis-by-Wire Solutions Make Their Debut, and EMB Enters Mass Production and Adoption for the...

Central Domain Control (Powertrain, Chassis, Body) and Motion Controller Research Report, 2026

Central Domain Control and Motion Control Research: XYZ Coordinated Control and Full X-by-Wire Actuation System

With the gradual penetration of L3+ autonomous driving, the chassis control system is ...

48V Low-voltage Power Distribution Network (PDN) Architecture and Supply Chain Panorama Research Report, 2026

Research on 48V Low-Voltage Power Distribution Network (PDN): An Active 48V Supply Chain, with Priority Deployment in High-Power Scenarios Such as Steer-by-Wire Chassis

The automotive 48V low-voltage...

AI-Defined Vehicle (AIDV) OEMs' Deployment Strategies Research Report, 2026

AIDV Research: Deployment Strategies of 22 OEMs

The AI-Defined Vehicle (AIDV) OEMs' Deployment Strategies Research Report, 2026, released by ResearchInChina, analyzes the AI deployment strategies of ...

OEMs’ Passenger Car Model Planning Research Report, 2026

Vehicle Model Planning Research: Chinese OEMs Launch Sub-Brands Intensively, While Multinational OEMs Apply the Brakes to Electrification Strategies

ResearchInChina released the OEMs’ Passenger Car M...

Autonomous Driving Simulation and World Model Research Report, 2026

Autonomous driving simulation research: "Simulation test + world model"-driven test system has become R&D infrastructure.

The "Autonomous Driving Simulation and World Model Research Report, 2026"...

Cockpit-Driving Integration Central Domain Controller SoC and AI Supercomputing Architecture Research Report, 2026

Cockpit-Driving integration and AI supercomputing research: The One Chip solution is rapidly installed in vehicles, and AI supercomputing architectures are moving towards full-domain integration.

AI ...

Intelligent Driving End-to-End Large Model Research Report, 2026

Research on Intelligent Driving Large Models: A Critical Period for Technological Competition and Paradigm Integration

As autonomous driving technology rapidly iterates from L2 to L3?L4, intelligent...

Automotive Digital Key Industry Trend Report, 2026

Digital Key Research: Automotive BLE, UWB and SLE Hardware Layout

The Automotive Digital Key Industry Trend Report, 2026, released by ResearchInChina, analyzes and predicts the digital key market, co...

Monthly Report on Automotive New Technology (May 2026)

UHD gaze technology, full-color LiDAR, UWB, etc. promote the upgrade of intelligent driving perception capabilities

This report is published once a month and is available for annual subscription.The...

In-Cabin Monitoring Systems (DMS, OMS, etc.) Research Report, 2026

In-Cabin Monitoring System Research: DMS to Become Mandatory in 2027, Expected to be Installed in Over 14 Million Vehicles

ResearchInChina released the In-Cabin Monitoring Systems (DMS, OMS, etc.) Re...

Automotive Service-Oriented Architecture (SOA) and Cross-Domain Middleware Industry Report, 2026

Research on automotive SOA and cross-domain middleware: The era of AI atomic services and AI cross-domain fusion agents is coming.

Automotive SOA evolves towards AI + full SOA servitization Driv...