Automotive PCB research: vehicle intelligence and electrification bring about demand for PCBs, and local manufacturers come to the fore.

The share of electronics in curb weight of a vehicle is rising, expectedly up to 34.3% in 2020, which is accompanied by more vehicle entertainment and safety functions and the growth of new energy vehicles. This gives a direct boost to demand for automotive printed circuit boards (PCB).

The COVID-19 epidemic in 2020 slashed the global vehicle sales and led to a big shrinkage of the industry scale to USD6,261 million. Yet the gradual epidemic control has driven the sales up a lot. Moreover, the growing penetration of ADAS and new energy vehicles will favor sustained growth in demand for PCBs, which is projected to outstrip USD12 billion in 2026.

As the largest PCB manufacturing base and also the biggest vehicle production base in the world, China demands a great many of PCBs. By one estimate, China’s automotive PCB market was worth up to USD3,501 million in 2020.

Vehicle intelligence pushes up demand for PCBs.

As consumers demand safer, more comfortable, more intelligent automobiles, vehicles tend to be electrified, digitalized and intelligent. ADAS needs many PCB-based components such as sensor, controller and safety system. Vehicle intelligence therefore directly spurs demand for PCBs.

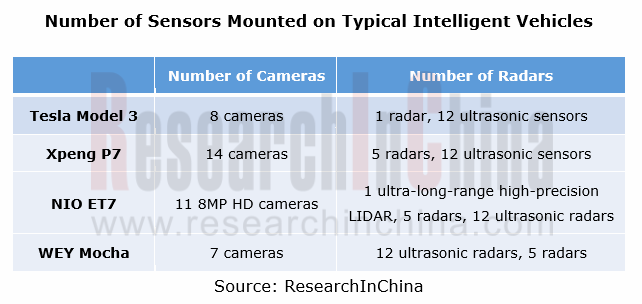

In ADAS sensor’s case, the average intelligent vehicle carries multiple cameras and radars to enable driving assistance functions. An example is Tesla Model 3 which packs 8 cameras, 1 radar and 12 ultrasonic sensors. On one estimate, the PCB for Tesla Model 3 ADAS sensors is valued at RMB536 to RMB1,364, or 21.4% to 54.6% of total PCB value, which makes it clear that vehicle intelligence boost demand for PCBs.

Vehicle electrification stimulates demand for PCBs.

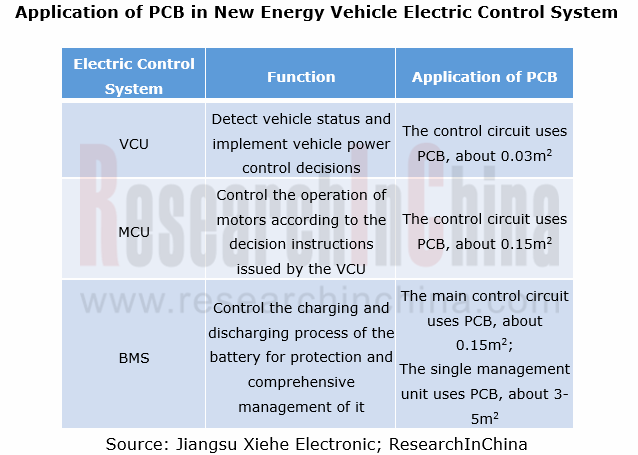

Differing from conventional vehicles, new energy vehicles need PCB-based power systems like inverter, DC-DC, on-board charger, power management system and motor controller, which directly boosts demand for PCBs. Examples include Tesla Model 3, a model with total PCB value higher than RMB2,500, 6.25 times that of ordinary fuel-powered vehicles.

In recent years, the global penetration of new energy vehicles has been on the rise. Major countries have formulated benign new energy vehicle industry policies; mainstream automakers race to launch their development plans for new energy vehicles as well. These moves will be a major contributor to the expansion of new energy vehicles. It is conceivable that the global penetration of new energy vehicles will ramp up in the years to come.

It is predicted that the global new energy vehicle PCB market will be worth RMB38.25 billion in 2026, as new energy vehicles become widespread and the demand from higher levels of vehicle intelligence favors a growth in PCB value per vehicle.

Local vendors cut a figure in the severer market competition.

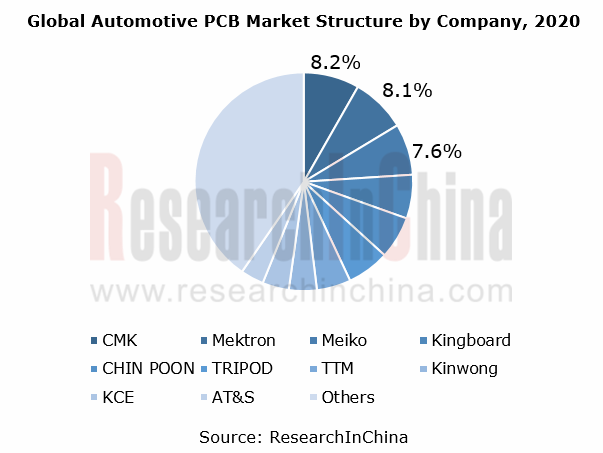

At present, the global automotive PCB market is dominated by Japanese players such as CMK and Mektron and Taiwan’s players like CHIN POON Industrial and TRIPOD Technology. The same is true of the Chinese automotive PCB market. Most of these players have built production bases in Chinese Mainland.

In Chinese Mainland, local companies take a small share in the automotive PCB market. Yet some of them already make deployments in the market, with increasing revenues from automotive PCBs. Some companies have a customer base covering the world’s leading auto parts suppliers, which means it is easier for them to secure bigger orders to gain strength. In future they may command more of the market.

Capital market helps local players.

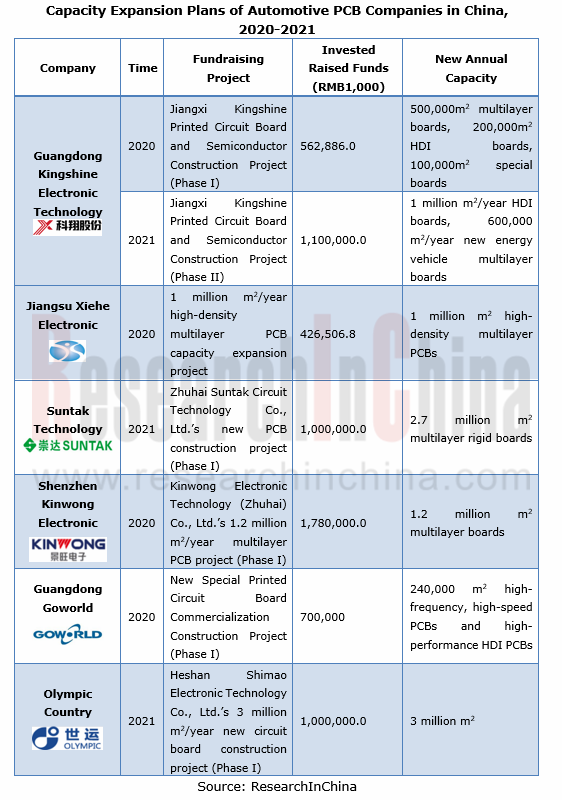

In recent two years, automotive PCB companies seek capital support to expand capacity for more competitive edges. With the backing of capital market, local players will become more competitive as a matter of course.

Automotive PCB products head in high-end direction, and local companies make deployments.

At present, automotive PCB products are led by double-layer and multi-layer boards, with relatively low demand for HDI boards and high frequency high speed boards, high value-added PCB products which will be more in demand in future as demand for vehicle communication and interiors increases and electrified, intelligent and connected vehicles develop.

The overcapacity of low-end products and fierce price war make companies less profitable. Some local companies tend to deploy high value-added products for becoming more competitive.

Research Report on AI Applications in Cockpits, 2026

AI Application in Cockpits: AI Services Become More Comprehensive, Convenient, and Refined.

In the first half of 2026, cockpit AI functions underwent initial upgrades across multiple dimensions, inc...

Software-Defined Vehicles in 2026: OEM Software Development and Supply Chain Deployment Strategy Research Report

Research on OEMs’ Software Strategies: R&D Focus, Development Strategies and Supplier Building Models of 30 OEMs

In this paper, we adopt a research framework covering 13 subsystems and 48 sub-di...

Passenger Car Chassis Domain Control and Chassis Cross-Domain Integration Research Report, 2026

Chassis Control Research: Mass Production of Full Chassis-by-Wire Solutions Starts

1. A Cluster of Full Chassis-by-Wire Solutions Make Their Debut, and EMB Enters Mass Production and Adoption for the...

Central Domain Control (Powertrain, Chassis, Body) and Motion Controller Research Report, 2026

Central Domain Control and Motion Control Research: XYZ Coordinated Control and Full X-by-Wire Actuation System

With the gradual penetration of L3+ autonomous driving, the chassis control system is ...

48V Low-voltage Power Distribution Network (PDN) Architecture and Supply Chain Panorama Research Report, 2026

Research on 48V Low-Voltage Power Distribution Network (PDN): An Active 48V Supply Chain, with Priority Deployment in High-Power Scenarios Such as Steer-by-Wire Chassis

The automotive 48V low-voltage...

AI-Defined Vehicle (AIDV) OEMs' Deployment Strategies Research Report, 2026

AIDV Research: Deployment Strategies of 22 OEMs

The AI-Defined Vehicle (AIDV) OEMs' Deployment Strategies Research Report, 2026, released by ResearchInChina, analyzes the AI deployment strategies of ...

OEMs’ Passenger Car Model Planning Research Report, 2026

Vehicle Model Planning Research: Chinese OEMs Launch Sub-Brands Intensively, While Multinational OEMs Apply the Brakes to Electrification Strategies

ResearchInChina released the OEMs’ Passenger Car M...

Autonomous Driving Simulation and World Model Research Report, 2026

Autonomous driving simulation research: "Simulation test + world model"-driven test system has become R&D infrastructure.

The "Autonomous Driving Simulation and World Model Research Report, 2026"...

Cockpit-Driving Integration Central Domain Controller SoC and AI Supercomputing Architecture Research Report, 2026

Cockpit-Driving integration and AI supercomputing research: The One Chip solution is rapidly installed in vehicles, and AI supercomputing architectures are moving towards full-domain integration.

AI ...

Intelligent Driving End-to-End Large Model Research Report, 2026

Research on Intelligent Driving Large Models: A Critical Period for Technological Competition and Paradigm Integration

As autonomous driving technology rapidly iterates from L2 to L3?L4, intelligent...

Automotive Digital Key Industry Trend Report, 2026

Digital Key Research: Automotive BLE, UWB and SLE Hardware Layout

The Automotive Digital Key Industry Trend Report, 2026, released by ResearchInChina, analyzes and predicts the digital key market, co...

Monthly Report on Automotive New Technology (May 2026)

UHD gaze technology, full-color LiDAR, UWB, etc. promote the upgrade of intelligent driving perception capabilities

This report is published once a month and is available for annual subscription.The...

In-Cabin Monitoring Systems (DMS, OMS, etc.) Research Report, 2026

In-Cabin Monitoring System Research: DMS to Become Mandatory in 2027, Expected to be Installed in Over 14 Million Vehicles

ResearchInChina released the In-Cabin Monitoring Systems (DMS, OMS, etc.) Re...

Automotive Service-Oriented Architecture (SOA) and Cross-Domain Middleware Industry Report, 2026

Research on automotive SOA and cross-domain middleware: The era of AI atomic services and AI cross-domain fusion agents is coming.

Automotive SOA evolves towards AI + full SOA servitization Driv...

Automotive Display, Center Console and Cluster Industry Report, 2026

Automotive Display Research: Multi-Screen Application Slows Down, While OLED and MiniLED Are Introduced in Vehicles Quickly

In 2026, automotive displays will no longer excessively pursue the number a...

Global and China Intelligent Vehicle Standard System Construction and Certification Research Report, 2026

Intelligent Driving Standards and Certification: With the Maturing Standardization System, China Will Participate in Formulation of Global Standards

China's automotive industry is transforming from ...

Automotive Intelligent Diagnosis Industry Report, 2026

Automotive Intelligent Diagnosis Research: Powered by AI, Remote Diagnosis Is Being Upgraded towards Intelligence.

ResearchInChina released the Automotive Intelligent Diagnosis Industry Report, 2026....

Automotive Cloud Service Platform Research Report, 2026

Research on automotive cloud service platform: with architecture upgrade and computing power improvement, cloud services enter a new stage

In 2026, the Internet of Vehicles industry generates petaby...