Automotive Memory Chip Research: Localization is imperative amid intense competition

The global smart phone storage market size hit US$46 billion in 2021 when the global automotive storage market size reached about US$4.5 billion, which is only equivalent to 1/10 of the former. Under development trend of intelligent connected vehicles, automobiles will become one of main growth engines of memory IC industry. By 2027, global automotive storage market size will exceed US$12.5 billion, with a CAGR of 18.6% from 2021 to 2027.

According to Micron Technology, the automotive storage market in China amounted to about US$700 million in 2021, and it will jump to US$1.5 billion by 2023. On the one hand, the growth momentum comes from growth of automobile shipments in China; on the other hand, it also benefits from continuous expansion of automotive memory and memory capacity.

High-level autonomous vehicles have posed enormous demand for automotive memory capacity, density and bandwidth

At present, main storage applications in automotive market include DRAM(DDR, LPDDR) and NAND (e.MMC and UFS, etc.). Low-power LPDDR and NAND will be main growth engines, and the demand for NOR Flash, used for chip startup, will continue to increase. In addition, higher intelligent driving levels will have a direct impact on the demand for GDDR, which is RAM specially used for ADAS floating-point computing chips in vehicles.

More powerful sensors, ADAS/AD integrated systems, central computers, digital cockpits, event recording systems,terminal-cloud computing, vehicle FOTA, etc. all put forward higher requirements for automotive memory. On the one hand, the memory capacity will go up from gigabytes (GB) to terabytes (TB); on the other hand, the memory density and bandwidth will be greatly improved.

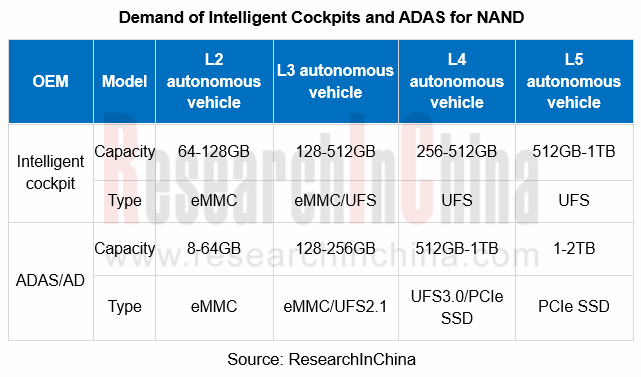

For example, NAND Flash mainly store continuous data in ADAS, IVI systems, automotive center console systems, etc. As autonomous driving levels up, the demand for NAND capacity in ADAS has swelled. Generally, L1/L2 ADAS only requires the mainstream 8GB e-MMC, L3 needs 128/256GB, and L5 may involve over 2TBt. In the future, the data production, transmission and recording of advanced autonomous vehicles will require higher density and speed, so that PCIe SSD may be adopted.

Autonomous vehicles boast more and more internal and external perception devices, including front cameras, internal cameras, high-resolution imaging radar, LiDAR, etc., and they will exploit high-density NOR Flash(QSPI, xSPI, etc., for chip startup) and DRAM(LPDDR3/4, LPDDR5, GDDR, etc.) widely.

At present, L1-L2 autonomous vehicles largely use LPDDR3 or LPDDR4, with the bandwidth of 25-50 GB/s. The bandwidth requirement is raised to 200GB/s for L3 autonomous driving, 300GB/s for L4 and 500GB/s for L5. Therefore, LPDDR5 and GDDR6 with higher bandwidth can simplify the system design of high-level autonomous vehicles.

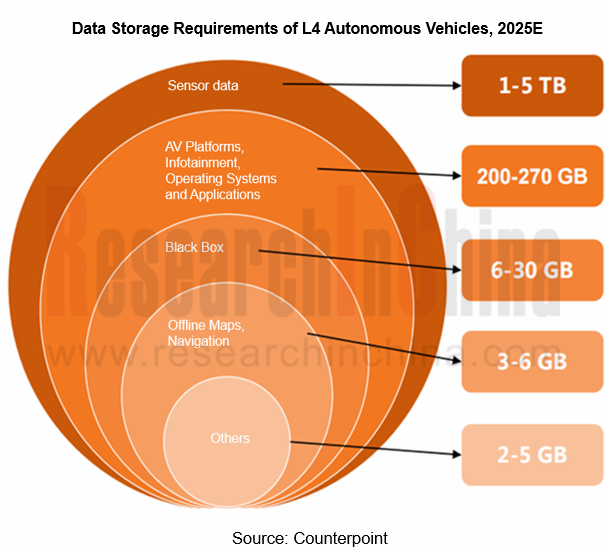

Counterpoint’s data shows that in the next decade, the memory capacity of a single vehicle will reach 2TB~11TB, catering to the requirements of different autonomous driving levels.

At the same time, autonomous driving is driven by data. The development of ADAS platforms needs massive road test data from cameras, radar, LiDAR, GPS and the like. These data are uploaded to the cloud for storage, AI training, simulation testing and verification. A one-hour L2 or L4-L5 road test probably generates 2TB or 16-20TB of data correspondingly, so that a single road test will produce 8-60TB of data, and the entire development cycle will churn out exabytes (EB) of data.

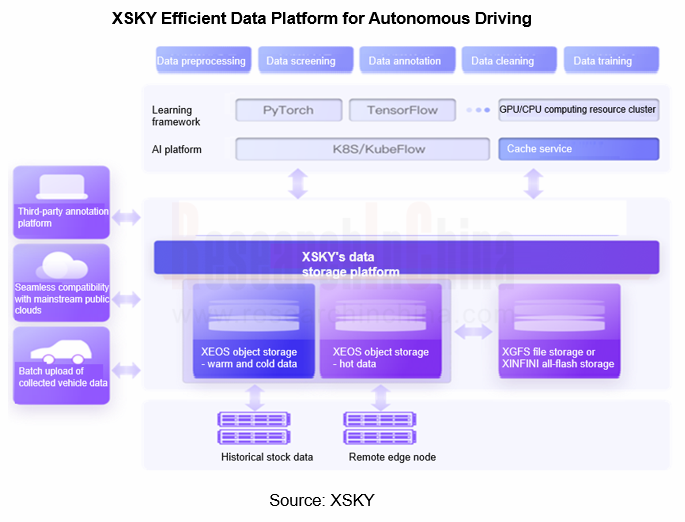

This has triggered huge market demand for autonomous driving cloud storage. In China, there are many cloud service providers that offer product solutions for autonomous driving data cloud storage, including Tencent Cloud, Alibaba Cloud, WD My Cloud, Sugon ParaStor, YRCloudFile, XSKY and so on.

As the functions of intelligent cockpits become more and more diversified, larger storage capacity is constantly in demand, and storage technology is constantly innovating

With the wide application of central integrated digital cockpits, DRAM has evolved from DDR2 and DDR3 to LPDDR4, LPDDR5 or GDDR. In addition, the interface of mobile phones has transferred from eMMC to UFS, so will smart cockpit memory chips. It is also possible for high-end models to adopt PCIe SSD.

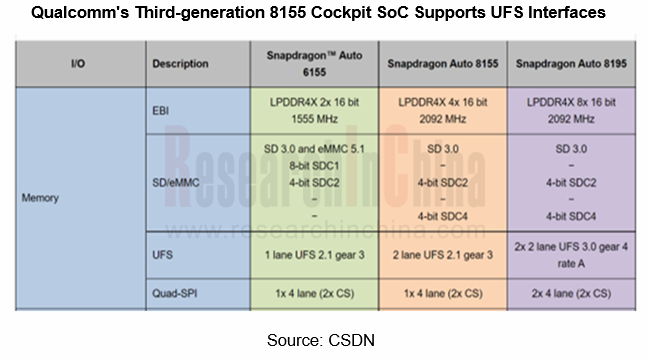

The cores of both UFS and eMMC interfaces involve NAND flash, but their control interfaces follow different protocols. The maximum communication rate of eMMC is 400MB/s, relative to 1,160 MB/s of UFS. The communication speed directly affects the startup time and software loading time of vehicles, which offer varying experience. In response to the demand for faster startup, reading and writing, the storage in the cockpit field must support UFS2.1 at least. Qualcomm's third-generation 8155 cockpit SoC has already endorsed UFS interfaces.

The intelligent cockpits of newly launched models demonstrate the increasingly powerful storage capacity:

?Xpeng P7 launched in 2020 is equipped with Qualcomm Snapdragon 820A with 8G memory + 128GB storage, enabling users to download more automotive Apps, supporting applet expansion, and featuring both practicality and fun;

?The next-generation SA8155P-based ZEEKR intelligent cockpit, available in ZEEKR 001 unveiled in 2021, has an 8-core CPU of the 7 nm process, with 16G memory and 128GB storage.

?Li L9 which debuted in 2022 comes standard with two Qualcomm Snapdragon 8155 chips with 24G memory and 256GB high-speed storage, which together form a powerful computing platform.

Chinese storage suppliers accelerate deployment in the promising automotive storage market

The requirements for automotive storage products are much higher than those for consumer electronics. Automotive-grade storage products have to take a long R&D and verification cycle, undergo a complicated certification process, comply with IATF16949, ASPCIE and ISO 26262, and satisfy the standards of some automakers, such as GMW3172 and VW80000. As a result, this market poses high barriers to entry and embodies obvious oligopoly.

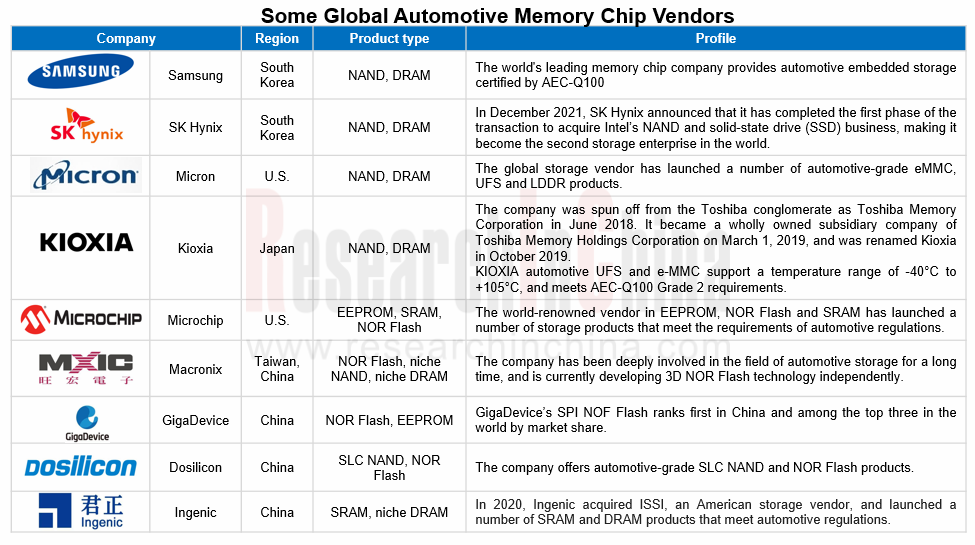

Overseas storage vendors such as Micron, Samsung, SK Hynix and Microchip still dominate the development of the automotive storage industry as monopolists. Among them, Micron enjoys the global market share of over 45%. In 2021, Micron launched its industry-leading automotive LPDDR5 certified by ISO 26262 ASIL-D, with the maximum capacity of 128GB.

In recent years, Chinese memory chip vendors have made great efforts in automotive storage products:

SRAM: Ingenic has been focusing on independent CPU, SoC and AI engines for many years. In 2020, it acquired 100% stake in Beijing ISSI. By virtue of intellectual property rights, it can completely avoid the impact of the sanctions imposed by the United States government, independently develop and produce SRAM in line with automotive regulations, and produce niche DRAM. Ingenic has reached close cooperation with auto parts vendors such as Bosch and Continental.

EEPROM: Giantec Semiconductor, a leading EEPROM enterprise in China, launched GT24C512B, a high-reliability automotive A1-grade memory chip, in August 2022, which can withstand erasing and writing for up to 4 million times at room temperature, and has been applied to OBC, VCU and other related fields.

NOR Flash: GigaDevice has delved in the field of NOR Flash for many years. By market share, it ranks first in China and third in the world. The GD25 series launched by GigaDevice is the only mass-produced NOR Flash in China that meets AEC-Q100, with the storage capacity of 2Mb~2Gb.

In addition to OEMs, there is another type of storage players in China, like Longsys, BIWIN Storage Technology and Powe, who buy wafers and particles from IDMs and purchase master chips from third-party master chip vendors, then conduct packaging tests through their own or third-party packaging and testing factories, and produce storage products of different storage types, interfaces and standards.

OEMs and Tier1s’ Intelligent Cockpit Platform (Hardware and Software) Innovation Strategy Research Report, 2026

Intelligent Cockpit Platform Research: multi-dimensional cockpit system architecture reconstruction for multi-agent collaboration and proactive intelligent services

The intelligent cockpit software s...

Automotive AIOS Research Report, 2026

Automotive AIOS Research: Mass Production Solutions Are Implemented

Mass Production Solutions Are Implemented on A Small Scale.

In 2026, AIOS starts small-scale implementation, helping to improve v...

Automotive Telematics Service Provider (TSP) Research Report, 2026

TSP Research: Leading providers collectively turn to AI agents to provide all-scenario active services

Telematics Service Providers (TSPs) are the core hub of the telematics industry chain, connectin...

Automotive Smart Interior Research Report, 2026

Smart Interior Research: As Technologies like Interactive Starlight Headliner, Hidden Display and Surface Projection Are Launched, Automotive Interiors Become Ever More Intelligent

The Automotive Sma...

Research Report on AI Applications in Cockpits, 2026

AI Application in Cockpits: AI Services Become More Comprehensive, Convenient, and Refined.

In the first half of 2026, cockpit AI functions underwent initial upgrades across multiple dimensions, inc...

Software-Defined Vehicles in 2026: OEM Software Development and Supply Chain Deployment Strategy Research Report

Research on OEMs’ Software Strategies: R&D Focus, Development Strategies and Supplier Building Models of 30 OEMs

In this paper, we adopt a research framework covering 13 subsystems and 48 sub-di...

Passenger Car Chassis Domain Control and Chassis Cross-Domain Integration Research Report, 2026

Chassis Control Research: Mass Production of Full Chassis-by-Wire Solutions Starts

1. A Cluster of Full Chassis-by-Wire Solutions Make Their Debut, and EMB Enters Mass Production and Adoption for the...

Central Domain Control (Powertrain, Chassis, Body) and Motion Controller Research Report, 2026

Central Domain Control and Motion Control Research: XYZ Coordinated Control and Full X-by-Wire Actuation System

With the gradual penetration of L3+ autonomous driving, the chassis control system is ...

48V Low-voltage Power Distribution Network (PDN) Architecture and Supply Chain Panorama Research Report, 2026

Research on 48V Low-Voltage Power Distribution Network (PDN): An Active 48V Supply Chain, with Priority Deployment in High-Power Scenarios Such as Steer-by-Wire Chassis

The automotive 48V low-voltage...

AI-Defined Vehicle (AIDV) OEMs' Deployment Strategies Research Report, 2026

AIDV Research: Deployment Strategies of 22 OEMs

The AI-Defined Vehicle (AIDV) OEMs' Deployment Strategies Research Report, 2026, released by ResearchInChina, analyzes the AI deployment strategies of ...

OEMs’ Passenger Car Model Planning Research Report, 2026

Vehicle Model Planning Research: Chinese OEMs Launch Sub-Brands Intensively, While Multinational OEMs Apply the Brakes to Electrification Strategies

ResearchInChina released the OEMs’ Passenger Car M...

Autonomous Driving Simulation and World Model Research Report, 2026

Autonomous driving simulation research: "Simulation test + world model"-driven test system has become R&D infrastructure.

The "Autonomous Driving Simulation and World Model Research Report, 2026"...

Cockpit-Driving Integration Central Domain Controller SoC and AI Supercomputing Architecture Research Report, 2026

Cockpit-Driving integration and AI supercomputing research: The One Chip solution is rapidly installed in vehicles, and AI supercomputing architectures are moving towards full-domain integration.

AI ...

Intelligent Driving End-to-End Large Model Research Report, 2026

Research on Intelligent Driving Large Models: A Critical Period for Technological Competition and Paradigm Integration

As autonomous driving technology rapidly iterates from L2 to L3?L4, intelligent...

Automotive Digital Key Industry Trend Report, 2026

Digital Key Research: Automotive BLE, UWB and SLE Hardware Layout

The Automotive Digital Key Industry Trend Report, 2026, released by ResearchInChina, analyzes and predicts the digital key market, co...

Monthly Report on Automotive New Technology (May 2026)

UHD gaze technology, full-color LiDAR, UWB, etc. promote the upgrade of intelligent driving perception capabilities

This report is published once a month and is available for annual subscription.The...

In-Cabin Monitoring Systems (DMS, OMS, etc.) Research Report, 2026

In-Cabin Monitoring System Research: DMS to Become Mandatory in 2027, Expected to be Installed in Over 14 Million Vehicles

ResearchInChina released the In-Cabin Monitoring Systems (DMS, OMS, etc.) Re...

Automotive Service-Oriented Architecture (SOA) and Cross-Domain Middleware Industry Report, 2026

Research on automotive SOA and cross-domain middleware: The era of AI atomic services and AI cross-domain fusion agents is coming.

Automotive SOA evolves towards AI + full SOA servitization Driv...