The global automotive memory chip market was worth USD4.76 billion in 2023, and it is expected to reach USD10.25 billion in 2028 boosted by high-level autonomous driving. The automotive storage market is a high-growth semiconductor segment.

Automotive memory chips accounted for about 8-9% of the value of automotive semiconductors in 2023, and the proportion is expected to rise to 10-11% in 2028, mainly because the faster innovation in automotive memory chips promotes the rapid adoption of advanced memory chips into cars. Main driving forces are:

?DRAM: DRAM is the memory chip with the largest market size. In the field of consumer electronics (mobile phones, PCs, tablet PCs, etc.), DDR5 (LPDDR5) has become mainstream and will gradually replace the conventional DDR4 (LPDDR4) in the next 2-3 years. In the automotive field, the conventional DDR is evolving to DDR4, LPDDR3 and LPDDR4, and then to advanced storage products such as LPDDR5 and GDDR6.

?HBM: as the enhanced version of DRAM, HBM provides higher bandwidth and capacity by stacking multiple DRAM chips. Because of high price, it is unlikely to appear in vehicles for a long time, but the cloud server used for training the Transformer AI foundation model must be equipped with multiple HBMs which account for about 9% of the AI server cost, with the ASP (average selling price) per unit as high as USD18,000.

?NAND Flash: In the automotive computing system, important data and trained weight models are stored in the hard disk (i.e., eMMC or UFS). NAND generally stores continuous data in ADAS, IVI systems, center consoles, etc. In the trend towards five-domain fusion, a single vehicle will need 2TB+ NAND in the next 3-5 years, and automotive PCIe SSD for central computing will become an important growth engine.

?SRAM: SRAM is much faster than NAND and DRAM but more expensive. Independent SRAM has almost disappeared, and it is mainly integrated directly into CPU, GPU and various SoCs in the form of an IP kernel. High-performance automotive SoCs generally integrate high-capacity on-chip SRAM.

?MRAM: Wafer giants such as Samsung and TSMC are developing MRAM for the next-generation automotive applications. NXP plans to introduce MRAM to its next-generation S32 zonal ECUs and MCUs. The industry believes that MRAM is expected to replace SRAM as cache memory.

?EEPROM: a smart car requires up to 30-40 EEPROM chips, while an ordinary fuel-powered vehicle only needs about 15 EEPROM chips. EEPROM is extending to BMS, intelligent cockpits, gateways, "electric drive, battery, electric control" systems and other applications.

?FRAM: FRAM outperforms conventional Flash and EEPROM in reading and writing durability, writing speed and power consumption, and has been applied to airbag data storage, event data recorder (EDR), new energy vehicle CAN-BOX, new energy vehicle communication terminal (T-BOX) and other fields.

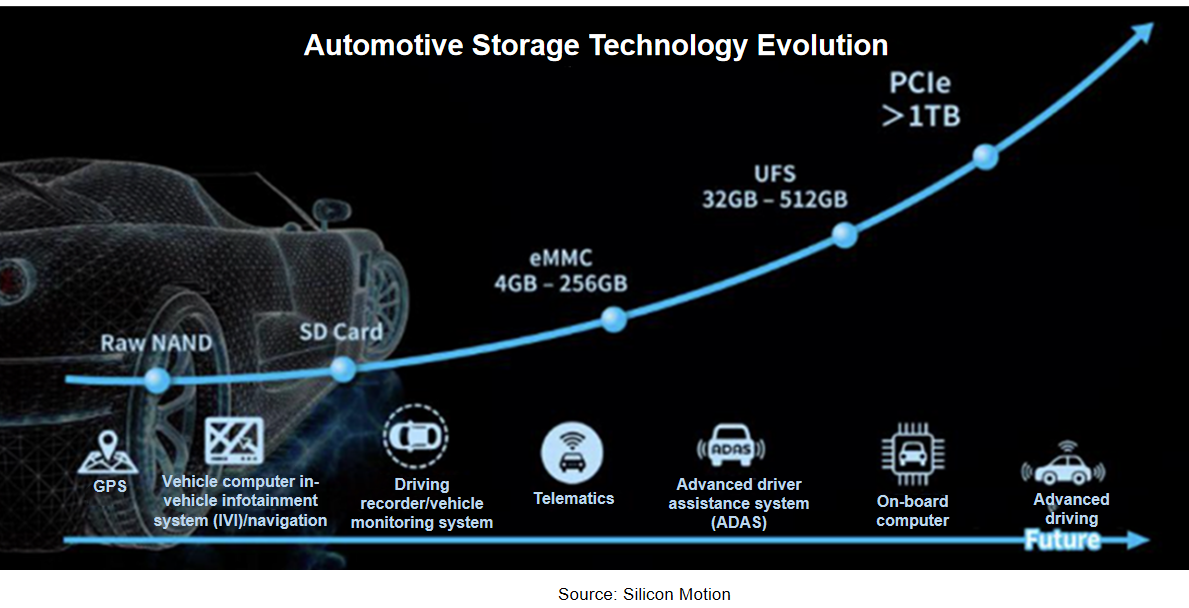

Evolution of automotive NAND Flash memory: UFS 4.0, PCIe SSD for central computing, CXL memory expansion technology

As with a computer system, a current automotive computing system also has a hard disk where important data and trained weight models are stored.

eMMC5.1 and UFS3.1 have become the mainstream standards for automotive NAND Flash memory. In February 2024, KIOXIA announced sampling of the industry’s first Universal Flash Storage (UFS) Ver. 4.0 embedded flash memory devices designed for automotive applications in line with AEC-Q100 Grade2 requirements. UFS 4.0 supports theoretical interface speeds of up to 23.2Gbps per lane or 46.4Gbps per device. It is conceivable that by 2025, UFS 4.0 will become one of automotive storage standards, and will be applicable to different automotive EEAs.

In the future, the automotive NVMe SSD based on PCIe interfaces will offer data throughput of more than 10GB/s, and the massive storage capacity will provide strong support for the next-generation intelligent automotive systems. Automotive SSD refers to the solid-state drive with PCIe as the physical layer and NVMe as the communication protocol.

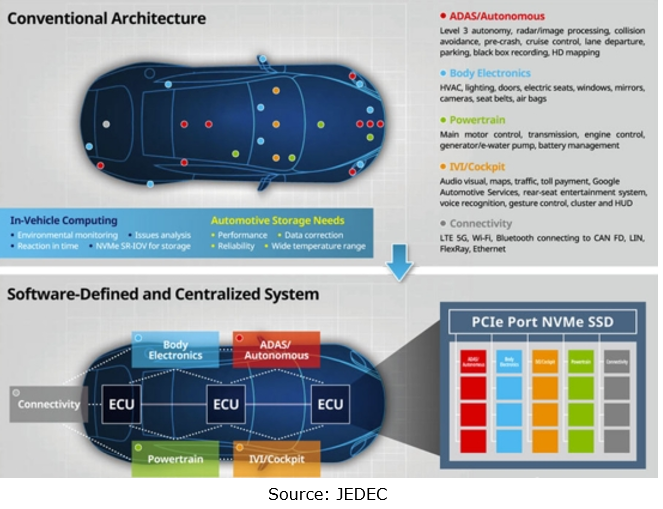

NVMe supports ultra-long queues so as to greatly ease the storage bottleneck problem during parallel computing. In the era of central computing, storage should be integrated into the central computer, and PCIe is the best choice. SSD is connected to the central computing unit SoC via a PCIe switch.

JEDEC, a standard setter in the storage industry, approved the JESD312 standard in November 2022, and officially released it on December 14. JESD312 defines the specifications of interface parameters, signaling protocols, environmental requirements, packaging, and other features for a solid state drive (SSD) targeted primarily at automotive applications. Automotive SSD is directly mounted on PCB in the form of BGA, with the size not larger than 28x28 mm. It uses four PCIe 4.0 interfaces to provide a peak transmission rate of up to 8 Gb/s.

JESD312 takes into a full account the changes of automotive electronic architectures, targets software-defined vehicles and central computing architecture, and allows the storage array to be partitioned.

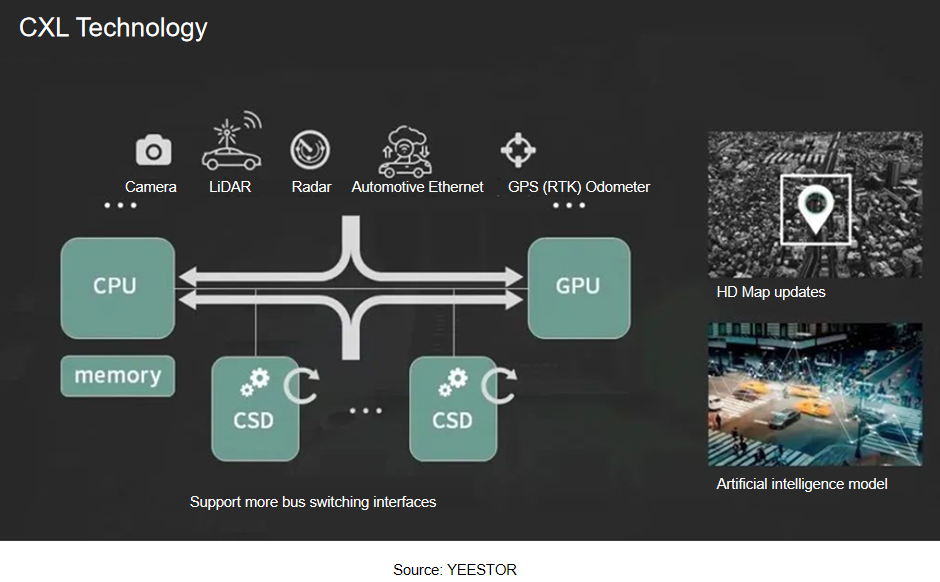

CXL (Compute Express Link), a storage technology based on PCIe, will be one of the important development directions of automotive storage in the future. CXL is a new open interconnect standard, and its essence is to change the original hard disk access model into the existing memory access model and exchange data in the form of memory access. CXL enables high-speed and efficient interconnect between CPU and GPU, FPGA or other accelerators, thus meeting the requirements of high-performance heterogeneous computing.

Evolution of automotive DRAM: In the era of Transformer model, GDDR6 and HBM develop rapidly, and storage cost shoots up.

The key to AI operation lies in storage instead of AI processor. 90% of the power consumption and delay of AI operation come from storage or data transfer. In 90% working conditions, the AI processor is waiting for the storage system to transfer data, and the time required by the computing system is almost negligible, so the performance of the storage system actually determines the real computing power. Wherein, the storage bandwidth can basically be equated to the performance of the storage system and the real computing power.

In the Transformer era, there are at least more than 1 billion model parameters, a model is at least 1GB, and the storage bandwidth determines whether Transformer can be run. In addition, storage dominates power consumption. According to Intel's research, when the semiconductor process reaches 7nm, an AI chip (accelerator) takes as high as 35pJ/bit to transfer data, making up 63.7% of the total power consumption.

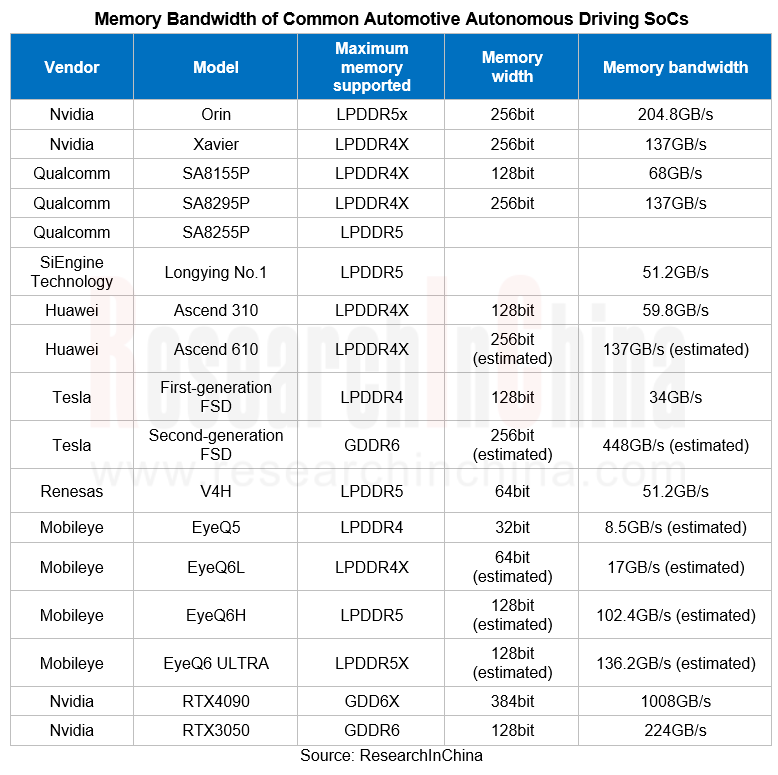

Intelligent vehicles pose ever higher requirements for image floating-point operation. To run Transformer smoothly, the weight model should be read up to 200 times per second, so the storage bandwidth should be at least 400GB/s, 600 GB/s better. On this basis, Samsung and Micron plan to launch their own automotive GDDR6 solutions.

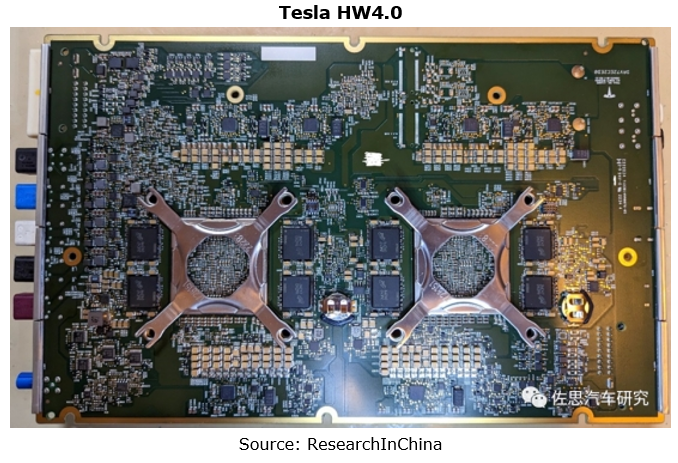

In Tesla HW3.0, the storage bandwidth of the first-generation FSD is only 34GB/s, which is difficult to support the next-generation foundation models. Tesla’s latest self-driving brain HW4.0 therefore uses GDDR6 at all costs, 16 pieces (2GB per piece) used, with 8 each on the front and back side, plus the 4 GDDR6 chips (also 2GB) in the cockpit controller, totaling 20 pieces (40GB), and the cost is more than USD160. HW3.0 uses 8 LPDDR4 chips, and a total of 8 LPDDR4 RAMs, each with capacity of 1GB, totaling 8GB, and the cost is about USD28.

In Tesla HW4.0, GDDR6 is non-automotive-grade D9PZR provided by Micron, and the GDDR6 physical layer of is from Cadence. Rambus also provides the GDDR6 physical layer and earns approximately USD140 million in annual revenue from its storage physical layer IPs. In September 2023, Cadence acquired the SerDes and memory interface PHY IP business from Rambus Inc.

Currently, among Tesla's automotive memory chips, the 2nd-generation FSD has the highest bandwidth ranging from 448Gb/s to 1008GB/s. SK Hynix’s HBM2E (H5WG6HMN6QX038R) supports minimum bandwidth of 460GB/s, with the density of 16GB. The dual-channel design allows for 920GB/s, even up to 1840GB/s, but it is still far less cost-effective than GDDR6.

GDDR6 is expected to prevail, and HBM may follow. Tesla HW 5.0 or the third-generation FSD chip may use HBM, but this is a distant future.

OEMs and Tier1s’ Intelligent Cockpit Platform (Hardware and Software) Innovation Strategy Research Report, 2026

Intelligent Cockpit Platform Research: multi-dimensional cockpit system architecture reconstruction for multi-agent collaboration and proactive intelligent services

The intelligent cockpit software s...

Automotive AIOS Research Report, 2026

Automotive AIOS Research: Mass Production Solutions Are Implemented

Mass Production Solutions Are Implemented on A Small Scale.

In 2026, AIOS starts small-scale implementation, helping to improve v...

Automotive Telematics Service Provider (TSP) Research Report, 2026

TSP Research: Leading providers collectively turn to AI agents to provide all-scenario active services

Telematics Service Providers (TSPs) are the core hub of the telematics industry chain, connectin...

Automotive Smart Interior Research Report, 2026

Smart Interior Research: As Technologies like Interactive Starlight Headliner, Hidden Display and Surface Projection Are Launched, Automotive Interiors Become Ever More Intelligent

The Automotive Sma...

Research Report on AI Applications in Cockpits, 2026

AI Application in Cockpits: AI Services Become More Comprehensive, Convenient, and Refined.

In the first half of 2026, cockpit AI functions underwent initial upgrades across multiple dimensions, inc...

Software-Defined Vehicles in 2026: OEM Software Development and Supply Chain Deployment Strategy Research Report

Research on OEMs’ Software Strategies: R&D Focus, Development Strategies and Supplier Building Models of 30 OEMs

In this paper, we adopt a research framework covering 13 subsystems and 48 sub-di...

Passenger Car Chassis Domain Control and Chassis Cross-Domain Integration Research Report, 2026

Chassis Control Research: Mass Production of Full Chassis-by-Wire Solutions Starts

1. A Cluster of Full Chassis-by-Wire Solutions Make Their Debut, and EMB Enters Mass Production and Adoption for the...

Central Domain Control (Powertrain, Chassis, Body) and Motion Controller Research Report, 2026

Central Domain Control and Motion Control Research: XYZ Coordinated Control and Full X-by-Wire Actuation System

With the gradual penetration of L3+ autonomous driving, the chassis control system is ...

48V Low-voltage Power Distribution Network (PDN) Architecture and Supply Chain Panorama Research Report, 2026

Research on 48V Low-Voltage Power Distribution Network (PDN): An Active 48V Supply Chain, with Priority Deployment in High-Power Scenarios Such as Steer-by-Wire Chassis

The automotive 48V low-voltage...

AI-Defined Vehicle (AIDV) OEMs' Deployment Strategies Research Report, 2026

AIDV Research: Deployment Strategies of 22 OEMs

The AI-Defined Vehicle (AIDV) OEMs' Deployment Strategies Research Report, 2026, released by ResearchInChina, analyzes the AI deployment strategies of ...

OEMs’ Passenger Car Model Planning Research Report, 2026

Vehicle Model Planning Research: Chinese OEMs Launch Sub-Brands Intensively, While Multinational OEMs Apply the Brakes to Electrification Strategies

ResearchInChina released the OEMs’ Passenger Car M...

Autonomous Driving Simulation and World Model Research Report, 2026

Autonomous driving simulation research: "Simulation test + world model"-driven test system has become R&D infrastructure.

The "Autonomous Driving Simulation and World Model Research Report, 2026"...

Cockpit-Driving Integration Central Domain Controller SoC and AI Supercomputing Architecture Research Report, 2026

Cockpit-Driving integration and AI supercomputing research: The One Chip solution is rapidly installed in vehicles, and AI supercomputing architectures are moving towards full-domain integration.

AI ...

Intelligent Driving End-to-End Large Model Research Report, 2026

Research on Intelligent Driving Large Models: A Critical Period for Technological Competition and Paradigm Integration

As autonomous driving technology rapidly iterates from L2 to L3?L4, intelligent...

Automotive Digital Key Industry Trend Report, 2026

Digital Key Research: Automotive BLE, UWB and SLE Hardware Layout

The Automotive Digital Key Industry Trend Report, 2026, released by ResearchInChina, analyzes and predicts the digital key market, co...

Monthly Report on Automotive New Technology (May 2026)

UHD gaze technology, full-color LiDAR, UWB, etc. promote the upgrade of intelligent driving perception capabilities

This report is published once a month and is available for annual subscription.The...

In-Cabin Monitoring Systems (DMS, OMS, etc.) Research Report, 2026

In-Cabin Monitoring System Research: DMS to Become Mandatory in 2027, Expected to be Installed in Over 14 Million Vehicles

ResearchInChina released the In-Cabin Monitoring Systems (DMS, OMS, etc.) Re...

Automotive Service-Oriented Architecture (SOA) and Cross-Domain Middleware Industry Report, 2026

Research on automotive SOA and cross-domain middleware: The era of AI atomic services and AI cross-domain fusion agents is coming.

Automotive SOA evolves towards AI + full SOA servitization Driv...