Research Report on Overseas Layout of Chinese Passenger Car OEMs and Supply Chain Companies, 2024

Research on overseas layout of OEMs: There are sharp differences among regions. The average unit price of exports to Europe is 3.7 times that to Southeast Asia.

The Research Report on Overseas Layout of Chinese Passenger Car OEMs and Supply Chain Companies, 2024 analyzes the status quo of China's automobile exports, overseas data, overseas automotive industry policies and other macro-environments; the status quo the automotive markets, tariff and subsidy policies, and performance of Chinese brands in key countries and regions such as Russia, Mexico, Saudi Arabia, Germany, Thailand, Japan, South Korea, Chile, France, Belgium, etc.; the overseas performance, expansion strategies, and factory construction and layout of OEMs such as SAIC, Chery, Changan, Dongfeng, Geely, Great Wall Motor, BYD, NIO, Neta, and Xpeng; the overseas production, R&D, and market layout of automotive supply chain companies such as CATL, CALB, FinDreams Battery, SVOLT Energy, EVE, Gotion High-tech, Desay SV, Ecarx, Hangsheng Electronics, Zhongding Group, Bohai Automotive Systems, Xingyu Automotive Lighting Systems and Fuyao Glass.

Passenger car exports: Europe is the largest export market of battery-electric vehicles, with the average export unit price 3.7 times that to Southeast Asia.

China's automobile exports have continued to grow at a high rate since 2022. Facing challenges from complex and changing external environments, ever more OEMs also have to make cautious deployments in overseas markets while accelerating their overseas market layout plan. The next three years are an important time node for Chinese OEMs to implement overseas strategies, and they need to closely track the internal and external environments.

In August 2024, China exported 610,000 vehicles, a year-on-year upsurge of 39% and a month-on-month growth of 10%. From January to August, China exported 4.09 million vehicles, surging by 27%. The main boosters to China's automobile exports in 2024 are still the higher penetration rate of new energy vehicles in the global market, the greater competitive edges of Chinese automobiles, and the small growth in the European and American automotive markets. In particular, the more competitive Chinese fuel-powered vehicles in the Russian and Middle Eastern markets boost the exports.

From January to August 2024, China's passenger car exports (42% of were new energy vehicles) swept 84.2% of the total automobile exports. Developed European countries such as Belgium and the United Kingdom also became important export markets for Chinese new energy vehicles.

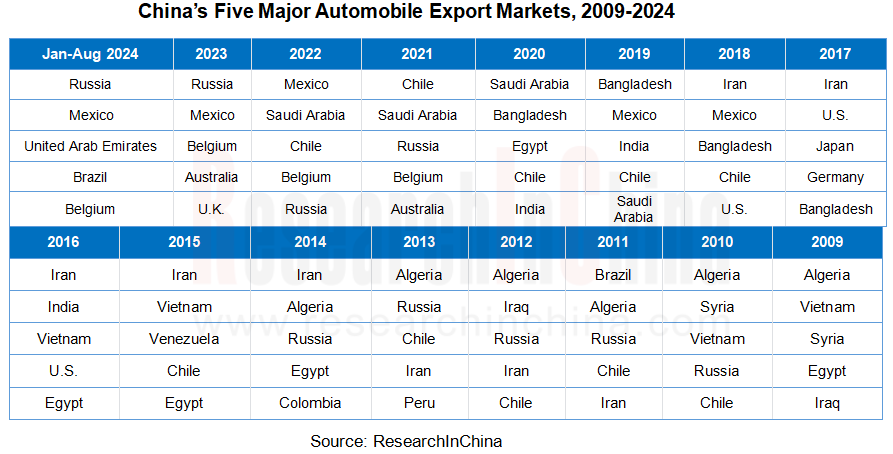

From the changes in the five major export markets of Chinese automobiles from 2009 to 2024, it can be seen that:

Before 2016, China mainly exported automobiles to Middle East, Southeast Asia, and Latin America;

After 2017, economically developed countries such as Belgium, Australia, Saudi Arabia, and the United Kingdom became the main destinations for China's automobile exports. It was also this year that the General Administration of Customs of the People's Republic of China began to include new energy vehicles in statistics for the first time.

Before the Sino-US trade friction, the United States often ranked among China's top five automobile export markets, but it has not been shortlisted since 2019. In September 2024, the US government officially locked in steep tariff hikes on Chinese imports, including a 100% duty on electric vehicles, which makes it more difficult for Chinese vehicles to enter the US market.

Since 2021, with the growth of new energy vehicle exports, developed countries have begun to become export destinations of Chinese automobiles frequently. The development of new energy vehicles has brought China's automobile exports into a critical window period of all-round upgrading and transformation from product export to technology export, service export, and brand export.

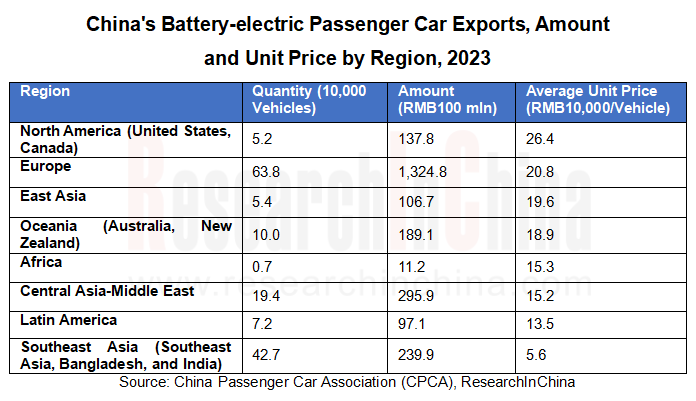

Europe is the largest export market for Chinese battery-electric vehicles. In 2023, China exported 640,000 battery-electric vehicles valued at RMB132.5 billion to Europe, with the average unit price of RMB208,000, 3.7 times that (RMB56,000) to Southeast Asia. The export of new energy vehicles to Europe and the United States has not only brought about "quantitative changes" but also "qualitative changes." Chinese OEMs have begun to enter overseas markets in a systematic and organized manner by establishing a perfect service system from overseas production to operations, sales, and R&D.

Amid countervailing investigations, increased tariffs, and even more stringent market access policies, China's automobile exports face challenges, but the solid foundation of China's automotive industry, complete automotive electronics industry chain, leading intelligent vehicle connection technology, and mature industrial worker system lay a firm foundation for the constant growth of China's automobile exports.

Overseas layout of OEMs: New vehicle factories gather in Thailand, and Europe will be the future layout focus.

Today, China is no longer simply exporting automobiles. Ever more OEMs begin to build after-sales service systems overseas.

SAIC established a European parts center in Amsterdam, the Netherlands, to offer after-sales services; it opened a second European parts center in France in the summer of 2024. SAIC has more than 2,800 marketing and service outlets around the world, of which MG has over 400 marketing and service outlets in Europe and 2 parts centers in the Netherlands and Belgium.

In September 2024, BYD announced that it had entered into an agreement with Hedin Mobility Group (BYD's dealer in Germany and Sweden) to acquire Hedin Electric Mobility GmbH and transfer the distribution activities of BYD vehicles and spare parts in the German market to BYD Automotive GmbH. The transaction also includes a business transfer of the two pioneer stores in Stuttgart and Frankfurt which are operated by Hedin Mobility Group. Therefore, BYD will no longer rely on German importers and will directly contact local dealers instead.

NIO has built the NIO Power Europe Plant in Pest, Hungary. The factory will serve as the operational fulcrum of the European strategy and will mainly produce swap stations that provide battery swap services for electric vehicles. It specializes in battery swap station manufacturing and after-sales services, NIO's European power-up business training, and the R&D of power-up products.

Some OEMs have begun to deploy their automotive technologies overseas.

In 2023, SAIC announced that it would cooperate with Audi to jointly develop technology. Audi and SAIC have decided to jointly develop new models built on a China-specific platform named “Advanced Digitized Platform” for the next generations of premium intelligent, connected vehicles (ICV).

At the end of 2023, Stellantis acquired an about 20% stake in Leapmotor for EUR1.5 billion. Through this acquisition, Leapmotor will provide electrification technology to Stellantis which will produce electric vehicles at its Turin plant in Italy.

Starting in 2024, Xpeng may earn corresponding fees by providing technical services to Volkswagen.

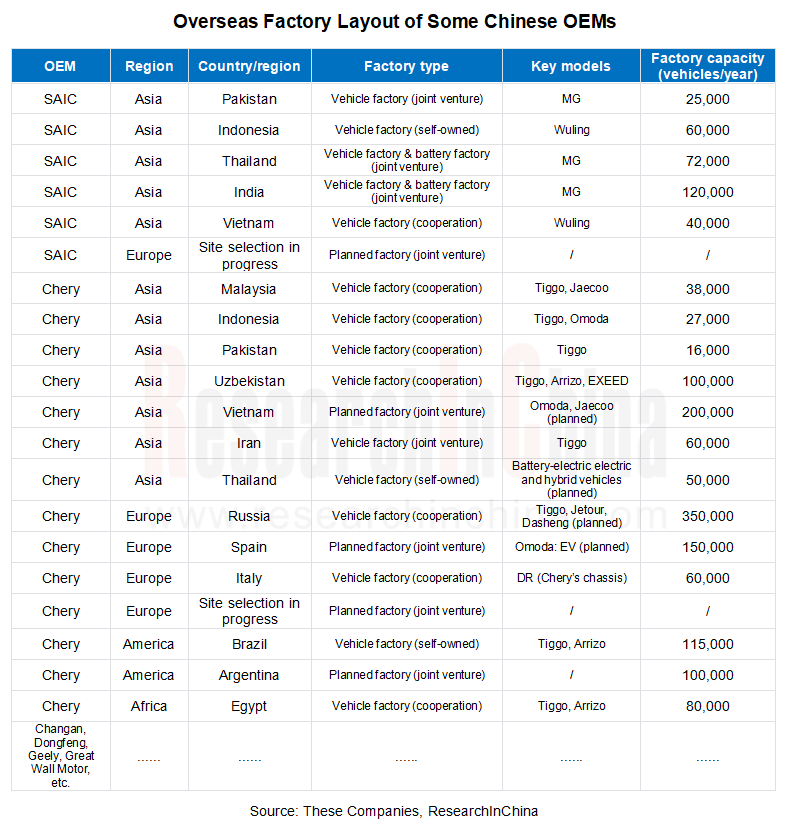

Of course, the establishment of overseas factories by OEMs has always been on the agenda of OEMs as the main measure to deal with tariffs and trade barriers. From the perspective of the overseas factory layout of Chinese OEMs:

The KD production model of cooperating with local factories in overseas markets has become relatively mature, but new cooperative manufacturers are still joining. In September 2024, Dongfeng Motor Corporation and Sudan G Group officially signed a contract to launch a new automobile assembly model dubbed "Made in China + Sudan". In September 2024, Geely inked an agreement with Vietnam-based Tasco to co-fund an automobile assembly plant in Thai Binh, Vietnam that assembles automobiles in the form of CKD. In January 2024, Great Wall Motor officially signed a contract on CKD with EP Manufacturing Berhad (EPMB), a large listed manufacturing group company in Malaysia, starting the assembly and production of GWM’s automobiles.

Chinese OEMs prefer to build overseas factories in Asia. Many of the new energy vehicle factories are planned to be built sin Europe, but with pending locations. New factories planned in Thailand, Indonesia, Brazil and other places will be constructed faster. The new factory planned by Changan in Thailand is located in an industrial park in Rayong Province. The BYD factory there was put into production in July 2024. There are also factories of SAIC MG, Chery, Great Wall Motor GAC and Neta in this province. See the Chinese OEMs (Passenger Car) Going Overseas Report, 2024 - Thailand for details.

Differing from SAIC’s acquisition of MG and Geely's acquisition of Volvo for the purpose of quickly deploying overseas markets, some Chinese OEMs have directly took over some factories transferred by other OEMs overseas to achieve overseas deployment at the lowest cost and fastest time. For example, BYD is set to revamp a defunct Ford factory in Cama?ari, Bahia, Brazil, which closed in 2021, and start production at the plant in 2025. Great Wall Motor took over the GM factory in Thailand on November 2, 2020. Chery's Spanish factory was originally owned by Nissan Motor Iberica. The joint venture factory between JSW Group and SAIC in India was formerly the Indian factory of GM.

In general, Chinese OEMs have begun to accelerate the construction of their own overseas factories, especially in Southeast Asia and Latin America; but they are relatively more cautious in the layout of factories in Europe and the United States. Despite difficulties, they still take this step unhesitatingly.

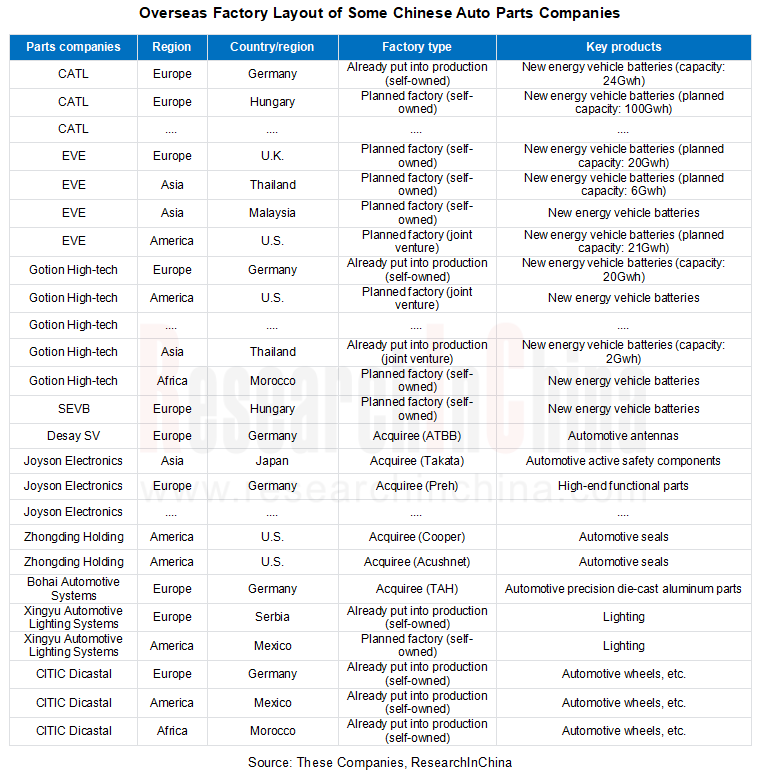

Supply chain companies going overseas: In the early days, they mainly acquired traditional parts companies. Now battery companies plan to build their own factories around the world

Chinese auto parts companies have also begun to accelerate their overseas layout. Chinese suppliers such as CATL, Gotion High-tech, Desay SV, and Joyson Electronics all have factories in Europe and have entered the supply chain of local European OEMs.

Traditional auto parts companies, such as automotive glass, interior parts, seals and die-casting parts suppliers, have already made layout overseas early. Some companies have expanded their overseas markets by way of acquiring overseas auto parts companies. Examples include Desay SV's acquisition of Germany-based ATBB, Joyson Electronics' acquisition of Germany-based Preh and QUIN, and Zhongding Holding's acquisition of Germany-based AMK and KACO. There are also multiple companies that have built their own factories overseas, for example, Xingyu Automotive Lighting Systems in Serbia, CITIC Dicastal in Germany, the Czech Republic and other European and American countries, and Tuopu Group in Poland.

Compared with OEMs which prefer to build their own factories in Southeast Asia, auto parts companies tend to build factories in Europe, especially in Germany maybe because they can serve the European automotive industry conveniently, and Germany boasts a mature automotive industry and abundant talents and its local governments support the investment and development of Chinese companies. See the Chinese OEMs (Passenger Car) Going Overseas Report, 2024 – Germany for details.

Chinese companies have advantages in cost and technology for mass production of batteries. As European OEMs speed up the electrified transformation in their local markets, Chinese battery companies are accelerating their plans to build factories in Europe to meet the European market's surging demand for power batteries. Hungary has become one of the most popular export destinations for Chinese battery companies. CATL, EVE, BYD, and SEVB have all planned to build factories in Hungary. Chinese battery companies frequently invest in Hungary mainly because of the country's complete automotive industry chain and its location as the center of Europe. The Hungarian government also hopes to turn the country into a manufacturing hub for electric vehicles, batteries and other new technologies with the help of Chinese investors.

While electric vehicle and parts companies are expanding overseas markets, Chinese intelligent driving solution suppliers have also made their foray into overseas markets by setting up overseas R&D centers and launching overseas market projects. Pony.ai plans to establish a regional R&D center in Luxembourg to focus on the exploration and R&D of cutting-edge fields of autonomous driving. Pony.ai has already built cooperation on autonomous driving technology and application in South Korea, Luxembourg, Saudi Arabia, the United Arab Emirates and more. iMotion positions its German subsidiary as a European engineering and technology center to fully meet challenges from regulations, policies, traffic environments, and R&D processes. WeRide has successfully commercialized autonomous driving in the United States, the United Arab Emirates, France, Singapore, and other places, involving robobuses, robotaxis, and sanitation vehicles.

OEMs and Tier1s’ Intelligent Cockpit Platform (Hardware and Software) Innovation Strategy Research Report, 2026

Intelligent Cockpit Platform Research: multi-dimensional cockpit system architecture reconstruction for multi-agent collaboration and proactive intelligent services

The intelligent cockpit software s...

Automotive AIOS Research Report, 2026

Automotive AIOS Research: Mass Production Solutions Are Implemented

Mass Production Solutions Are Implemented on A Small Scale.

In 2026, AIOS starts small-scale implementation, helping to improve v...

Automotive Telematics Service Provider (TSP) Research Report, 2026

TSP Research: Leading providers collectively turn to AI agents to provide all-scenario active services

Telematics Service Providers (TSPs) are the core hub of the telematics industry chain, connectin...

Automotive Smart Interior Research Report, 2026

Smart Interior Research: As Technologies like Interactive Starlight Headliner, Hidden Display and Surface Projection Are Launched, Automotive Interiors Become Ever More Intelligent

The Automotive Sma...

Research Report on AI Applications in Cockpits, 2026

AI Application in Cockpits: AI Services Become More Comprehensive, Convenient, and Refined.

In the first half of 2026, cockpit AI functions underwent initial upgrades across multiple dimensions, inc...

Software-Defined Vehicles in 2026: OEM Software Development and Supply Chain Deployment Strategy Research Report

Research on OEMs’ Software Strategies: R&D Focus, Development Strategies and Supplier Building Models of 30 OEMs

In this paper, we adopt a research framework covering 13 subsystems and 48 sub-di...

Passenger Car Chassis Domain Control and Chassis Cross-Domain Integration Research Report, 2026

Chassis Control Research: Mass Production of Full Chassis-by-Wire Solutions Starts

1. A Cluster of Full Chassis-by-Wire Solutions Make Their Debut, and EMB Enters Mass Production and Adoption for the...

Central Domain Control (Powertrain, Chassis, Body) and Motion Controller Research Report, 2026

Central Domain Control and Motion Control Research: XYZ Coordinated Control and Full X-by-Wire Actuation System

With the gradual penetration of L3+ autonomous driving, the chassis control system is ...

48V Low-voltage Power Distribution Network (PDN) Architecture and Supply Chain Panorama Research Report, 2026

Research on 48V Low-Voltage Power Distribution Network (PDN): An Active 48V Supply Chain, with Priority Deployment in High-Power Scenarios Such as Steer-by-Wire Chassis

The automotive 48V low-voltage...

AI-Defined Vehicle (AIDV) OEMs' Deployment Strategies Research Report, 2026

AIDV Research: Deployment Strategies of 22 OEMs

The AI-Defined Vehicle (AIDV) OEMs' Deployment Strategies Research Report, 2026, released by ResearchInChina, analyzes the AI deployment strategies of ...

OEMs’ Passenger Car Model Planning Research Report, 2026

Vehicle Model Planning Research: Chinese OEMs Launch Sub-Brands Intensively, While Multinational OEMs Apply the Brakes to Electrification Strategies

ResearchInChina released the OEMs’ Passenger Car M...

Autonomous Driving Simulation and World Model Research Report, 2026

Autonomous driving simulation research: "Simulation test + world model"-driven test system has become R&D infrastructure.

The "Autonomous Driving Simulation and World Model Research Report, 2026"...

Cockpit-Driving Integration Central Domain Controller SoC and AI Supercomputing Architecture Research Report, 2026

Cockpit-Driving integration and AI supercomputing research: The One Chip solution is rapidly installed in vehicles, and AI supercomputing architectures are moving towards full-domain integration.

AI ...

Intelligent Driving End-to-End Large Model Research Report, 2026

Research on Intelligent Driving Large Models: A Critical Period for Technological Competition and Paradigm Integration

As autonomous driving technology rapidly iterates from L2 to L3?L4, intelligent...

Automotive Digital Key Industry Trend Report, 2026

Digital Key Research: Automotive BLE, UWB and SLE Hardware Layout

The Automotive Digital Key Industry Trend Report, 2026, released by ResearchInChina, analyzes and predicts the digital key market, co...

Monthly Report on Automotive New Technology (May 2026)

UHD gaze technology, full-color LiDAR, UWB, etc. promote the upgrade of intelligent driving perception capabilities

This report is published once a month and is available for annual subscription.The...

In-Cabin Monitoring Systems (DMS, OMS, etc.) Research Report, 2026

In-Cabin Monitoring System Research: DMS to Become Mandatory in 2027, Expected to be Installed in Over 14 Million Vehicles

ResearchInChina released the In-Cabin Monitoring Systems (DMS, OMS, etc.) Re...

Automotive Service-Oriented Architecture (SOA) and Cross-Domain Middleware Industry Report, 2026

Research on automotive SOA and cross-domain middleware: The era of AI atomic services and AI cross-domain fusion agents is coming.

Automotive SOA evolves towards AI + full SOA servitization Driv...