ADAS and Autonomous Driving Tier 1 Suppliers Report, 2018-2019

-

May 2019

- Hard Copy

- USD

$3,200

-

- Pages:145

- Single User License

(PDF Unprintable)

- USD

$3,000

-

- Code:

LY006

- Enterprise-wide License

(PDF Printable & Editable)

- USD

$4,500

-

- Hard Copy + Single User License

- USD

$3,400

-

ADAS and Autonomous Driving Tier 1 Suppliers Report, 2018-2019: Huge Investment, Increasing Orders, and Soaring Labor Cost

From the progress of the world’s main Tier1 suppliers in autonomous driving, it can be seen that the giants like Bosch and Continental are moving forward at their own pace in line with their timetable.

Traditional Tier1 suppliers are sparing no efforts in enlarging talent teams (especially software), developing ADAS/AD domain controllers, acquiring sensor firms and self-development, testing autonomous driving technology in various scenarios (industrial park, highway, parking, etc.), expanding autonomous fleets for road test, building test fields on their own or together with others, establishing operation and data management centers, and allying themselves with more partners.

Tier1 suppliers suffer a slump in profits and even a bigger loss because of huge investment in autonomous driving, but there is good news that orders are increasing.

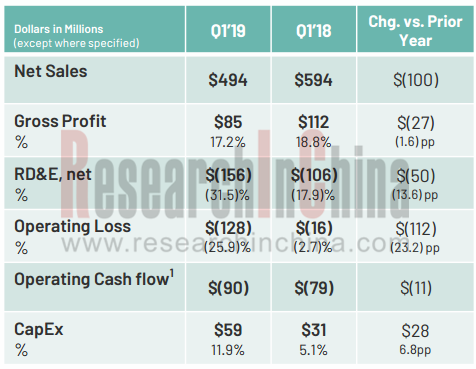

Veoneer’s operating loss for 2019Q1 jumped to USD128 million compared with USD16 million in 2018Q1; its R&D expenses rose to USD156 million from USD106 million in 2018Q1; capital expenditure surged from USD31 million to USD59 million largely for camera capacity expansion, according to Veoneer’s 2019Q1 financial results in the table above.

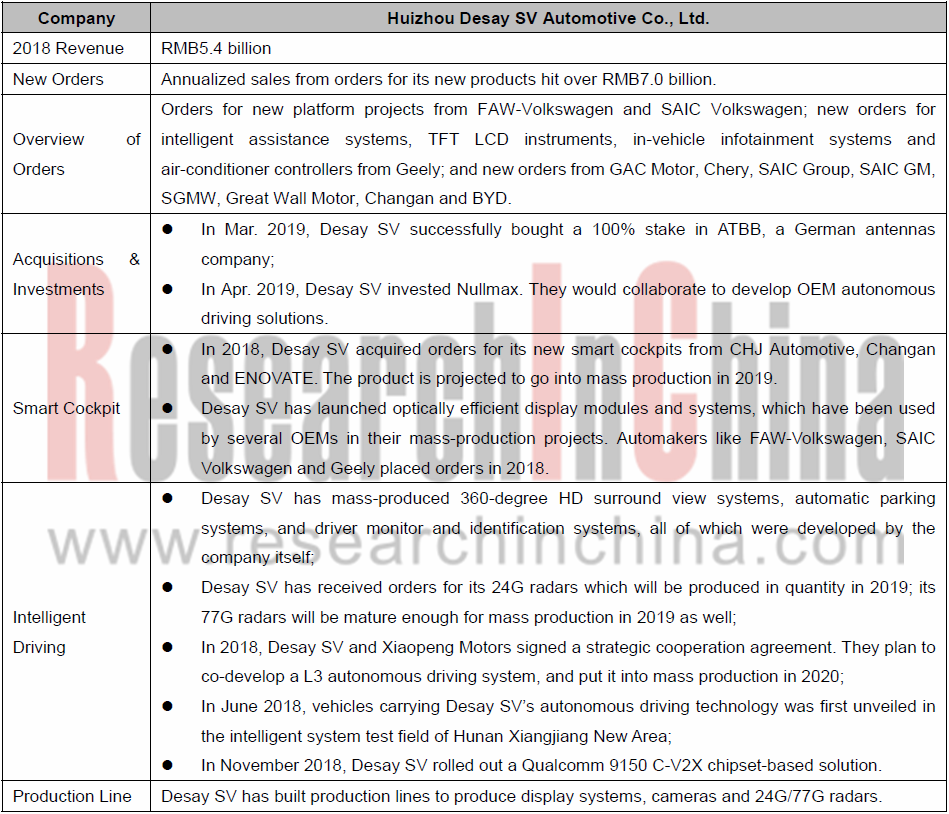

Among Chinese Tier1 suppliers, Huizhou Desay SV Automotive Co., Ltd., a leading player in ADAS and autonomous driving field, also sees its profit decline. The supplier’s operating results for 2019Q1 indicate that its net income attributable to the shareholders of the listed company stood at RMB43.54 million, a 72.82% plunge on an annualized basis, which was caused by a nosedive in China’s 2019Q1 automobile sales and the company’s huge investment in research and development of new technologies. In 2018, the company reported RMB5.4 billion in revenue, with annualized sales from orders for its new products outnumbering RMB7.0 billion.

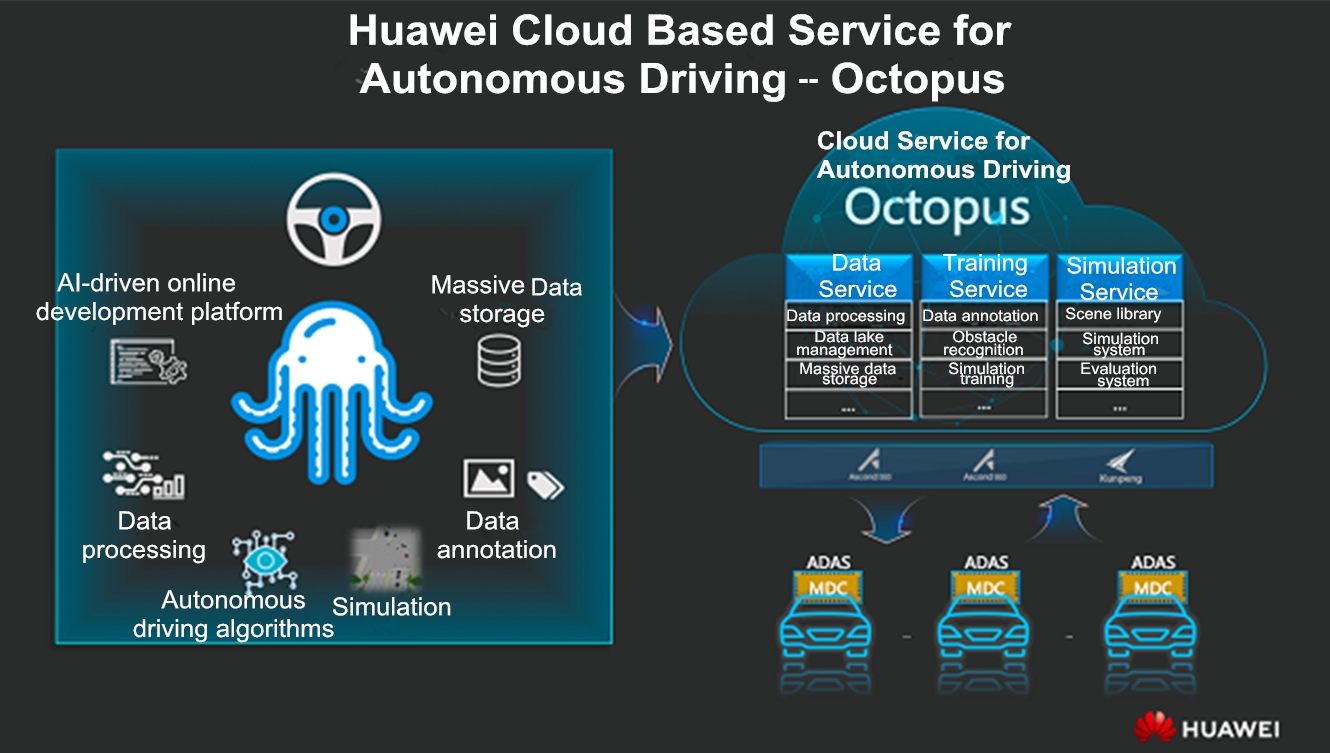

In April 2019, Huawei made its debut as a Tier1 supplier at Auto Shanghai, and exhibited solutions such as MDC, intelligent connectivity, Huawei Cloud (Octopus) and three types of sensors.

Huawei’s entry will intensify the already fierce competition among Tier1 suppliers of ADAS and autonomous driving solutions.

1 Comparative Analysis of Main ADAS and Autonomous Driving Tier1 Suppliers

1.1 Autonomous Driving System Is Divided into Three Levels

1.2 Autonomous Driving Planning, Commercialization Process and Development Features of Foreign Tier1 Suppliers

1.3 Product Layout of Foreign Tier1 Suppliers

1.4 Comparison of Foreign Tier1 Suppliers (including Revenue, Profit, Orders, Partners and Investment)

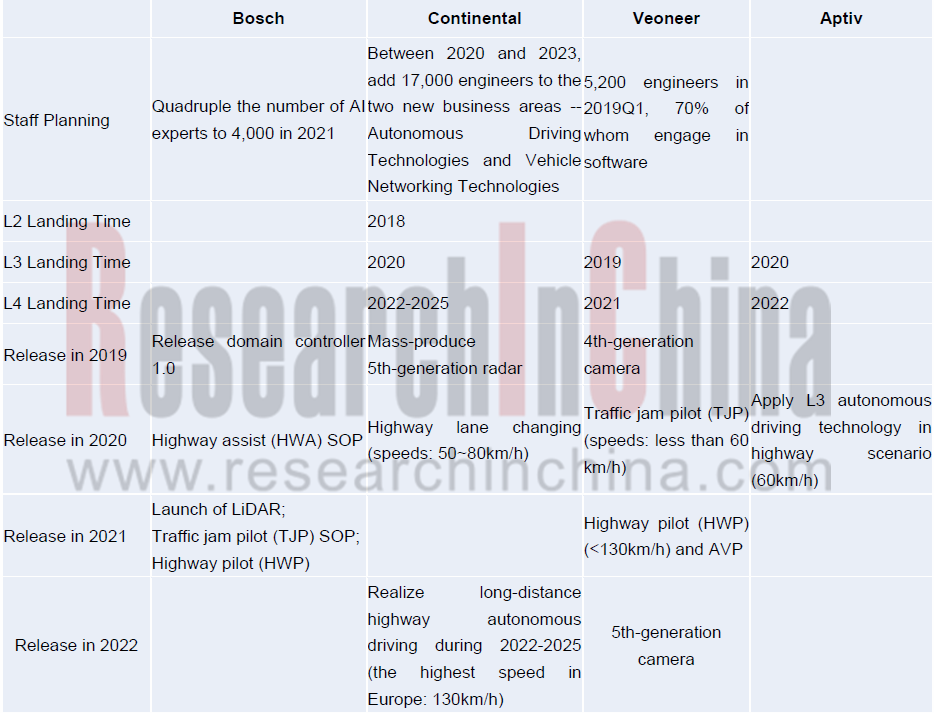

1.5 Planning Comparison of Foreign Tier1 Suppliers (including Personnel Planning, Launch Time of L2-L4, Products to Be Launched in 2019-2022)

1.6 Vision Product Investment Comparison of Foreign Tier1 Suppliers (Monocular, Stereo, etc.)

1.7 Radar Investment Comparison of Foreign Tier1 Suppliers (Millimeter Wave Radar, LiDAR, Ultrasonic Radar)

1.8 Other Technology Investment Comparison of Foreign Tier1 Suppliers (V2X, HD Map, High-precision Positioning, Domain Controller)

1.9 Autonomous Driving Application Scenario R&D Comparison of Main Tier1 Suppliers (Minibus, City, Highway, Parking)

1.10 Autonomous Driving Test and Operation Comparison of Main Tier1 Suppliers (Test Field, Test Vehicle, Base, etc.)

1.11 Development Layout Comparison of Chinese Tier1 Suppliers

2 Tier1 Suppliers of ADAS and Autonomous Driving Solutions Worldwide

2.1 Bosch

2.1.1 Profile

2.1.2 Autonomous Driving Sensor

2.1.3 Autonomous Driving Positioning Solution

2.1.4 Decision: Domain Controller

2.1.5 Autonomous Driving Product Layout

2.1.6 Autonomous Shuttle

2.1.7 Autonomous Driving Partners

2.1.8 ADAS and Autonomous Driving in 2018-2019

2.2 Continental

2.2.1 Profile

2.2.2 Performance

2.2.3 Organizational Restructuring Will Be Completed by 2020

2.2.4 Sensors

2.2.5 Autonomous Driving Development Plan

2.2.6 Three Integrated Solutions for Autonomous Driving

2.2.7 CuBE and Seamless Driving & Delivery

2.2.8 Autonomous Driving Layout and Partners

2.2.9 Autonomous Driving Layout in 2018-2019

2.3 Aptiv

2.3.1 Profile

2.3.2 Revenue and Orders

2.3.3 Strategic Positioning

2.3.4 Multi-domain Controller

2.3.5 ADAS Sensor

2.3.6 Autonomous Driving Route

2.3.7 Autonomous Driving Solution CSLP

2.3.8 L4 Test Autonomous Vehicle

2.3.9 Cooperation with Lyft in Autonomous Driving

2.3.10 Expedited Layout in Autonomous Driving Industry Chain through Investments, Acquisitions and Collaborations

2.3.11 Autonomous Driving Layout in 2018-2019

2.4 Valeo

2.4.1 Profile

2.4.2 Sensor Product Layout

2.4.3 Sensing Solution

2.4.4 Three Autonomous Driving Systems and Technology Roadmaps

2.4.5 Cruise4U (Highway)

2.4.6 Drive4U (Urban Road)

2.4.7 Automated Parking System Park4U

2.4.8 Autonomous Driving Partners

2.4.9 Autonomous Driving Dynamics in 2018-2019

2.5 ZF

2.5.1 Profile

2.5.2 Product Layout

2.5.3 ZF Sensors

2.5.4 ProAI

2.5.5 Autonomous Taxi and IoT Platform

2.5.6 Autonomous Driving Partners

2.5.7 Autonomous Driving Dynamics in 2018-2019

2.6 Hyundai Mobis

2.6.1 Profile

2.6.2 Autonomous Driving Layout

2.6.3 Research Progresses of ADAS and Autonomous Driving

2.6.4 ADAS and Autonomous Driving Dynamics in 2018-2019

2.7 Veoneer

2.7.1 Profile

2.7.2 Development in 2018 and Outlook for 2019

2.7.3 Major Projects and Customers

2.7.4 Product Milestones

2.7.5 Autonomous Driving Layout

2.7.6 Vision Products and Functional Planning

2.7.7 Monocular Vision System

2.7.8 Zeus

2.7.9 Autonomous Driving Solutions

2.7.10 ADAS Partners

2.7.11 Planning for Autonomous Driving Development

2.7.12 ADAS and Autonomous Driving Dynamics in 2018-2019

2.8 Visteon

2.8.1 Profile

2.8.2 Operation (Worldwide) in 2018

2.8.3 Operation (China) in 2018

2.8.4 Positioning in the Autonomous Driving Industry Chain

2.8.5 Major Products

2.8.6 Autonomous Driving Domain Controller DriveCore

2.8.7 DriveCore Computing Platform: Compute

2.8.8 DriveCore Algorithm: Studio

2.8.9 DriveCore Middleware: Runtime

2.8.10 ADAS Development History and Autonomous Driving Roadmap

2.8.11 Three ADAS Segments and Features

2.8.12 L3/L4 Autonomous Driving Test

2.8.13 Autonomous Driving Schedule

2.8.14 Autonomous Driving Partners

2.8.15 Autonomous Driving Dynamics in 2018-2019

2.9 Magna

2.9.1 Vision Products

2.9.2 Visual ADAS

2.9.3 MAX4 Domain Controller

2.9.4 MAX4 for L4 Autonomous Driving

2.9.5 Autonomous Driving Dynamics

2.10 Denso

2.10.1 Revenue

2.10.2 Autonomous Driving Investment and R&D Layout

2.10.3 Millimeter Wave Radar

2.10.4 Denso Ten

2.10.5 ADAS and Autonomous Driving Dynamics

3 Tier 1 Suppliers of Intelligent Connected ADAS and Autonomous Driving Solutions in China

3.1 Baidu

3.1.1 Apollo Platform

3.1.2 Apollo Autonomous Driving Open Roadmap

3.1.3 Apollo Open Platform Progress

3.1.4 Apollo Partners

3.1.5 L4 Passenger Car Solution and Partners

3.1.6 L4 Autonomous Park Car Solution

3.1.7 Open Source of V2X CVIS Solution

3.1.8 Upcoming Commercial Packaged Solution

3.1.9 Autonomous Driving Progress

3.2 Tencent

3.2.1 AD Lab

3.2.2 Autonomous Driving Layout

3.2.3 Autonomous Driving Solution

3.2.4 Autonomous Driving Planning

3.3 Neusoft Reach

3.3.1 Profile

3.3.2 Product Line

3.3.3 ADAS

3.3.4 Autonomous Driving

3.3.5 Cooperation

3.4 Huawei

3.4.1 Intelligent Connected Vehicle Business

3.4.2 L4 Computing Platform

3.4.3 C-V2X Technology

3.4.4 Intelligent Connected Vehicle Partners

3.4.5 Octopus

3.5 Foryou Corporation

3.5.1 Automotive Electronics Business

3.5.2 R&D Planning in 2019

3.6 Desay SV

3.6.1 Profile

3.6.2 Intelligent Vehicle Revenue and R&D Investment

3.6.3 Development of Three Major Businesses

3.6.4 Future Development Strategy

OEMs and Tier1s’ Intelligent Cockpit Platform (Hardware and Software) Innovation Strategy Research Report, 2026

Intelligent Cockpit Platform Research: multi-dimensional cockpit system architecture reconstruction for multi-agent collaboration and proactive intelligent services

The intelligent cockpit software s...

Automotive AIOS Research Report, 2026

Automotive AIOS Research: Mass Production Solutions Are Implemented

Mass Production Solutions Are Implemented on A Small Scale.

In 2026, AIOS starts small-scale implementation, helping to improve v...

Automotive Telematics Service Provider (TSP) Research Report, 2026

TSP Research: Leading providers collectively turn to AI agents to provide all-scenario active services

Telematics Service Providers (TSPs) are the core hub of the telematics industry chain, connectin...

Automotive Smart Interior Research Report, 2026

Smart Interior Research: As Technologies like Interactive Starlight Headliner, Hidden Display and Surface Projection Are Launched, Automotive Interiors Become Ever More Intelligent

The Automotive Sma...

Research Report on AI Applications in Cockpits, 2026

AI Application in Cockpits: AI Services Become More Comprehensive, Convenient, and Refined.

In the first half of 2026, cockpit AI functions underwent initial upgrades across multiple dimensions, inc...

Software-Defined Vehicles in 2026: OEM Software Development and Supply Chain Deployment Strategy Research Report

Research on OEMs’ Software Strategies: R&D Focus, Development Strategies and Supplier Building Models of 30 OEMs

In this paper, we adopt a research framework covering 13 subsystems and 48 sub-di...

Passenger Car Chassis Domain Control and Chassis Cross-Domain Integration Research Report, 2026

Chassis Control Research: Mass Production of Full Chassis-by-Wire Solutions Starts

1. A Cluster of Full Chassis-by-Wire Solutions Make Their Debut, and EMB Enters Mass Production and Adoption for the...

Central Domain Control (Powertrain, Chassis, Body) and Motion Controller Research Report, 2026

Central Domain Control and Motion Control Research: XYZ Coordinated Control and Full X-by-Wire Actuation System

With the gradual penetration of L3+ autonomous driving, the chassis control system is ...

48V Low-voltage Power Distribution Network (PDN) Architecture and Supply Chain Panorama Research Report, 2026

Research on 48V Low-Voltage Power Distribution Network (PDN): An Active 48V Supply Chain, with Priority Deployment in High-Power Scenarios Such as Steer-by-Wire Chassis

The automotive 48V low-voltage...

AI-Defined Vehicle (AIDV) OEMs' Deployment Strategies Research Report, 2026

AIDV Research: Deployment Strategies of 22 OEMs

The AI-Defined Vehicle (AIDV) OEMs' Deployment Strategies Research Report, 2026, released by ResearchInChina, analyzes the AI deployment strategies of ...

OEMs’ Passenger Car Model Planning Research Report, 2026

Vehicle Model Planning Research: Chinese OEMs Launch Sub-Brands Intensively, While Multinational OEMs Apply the Brakes to Electrification Strategies

ResearchInChina released the OEMs’ Passenger Car M...

Autonomous Driving Simulation and World Model Research Report, 2026

Autonomous driving simulation research: "Simulation test + world model"-driven test system has become R&D infrastructure.

The "Autonomous Driving Simulation and World Model Research Report, 2026"...

Cockpit-Driving Integration Central Domain Controller SoC and AI Supercomputing Architecture Research Report, 2026

Cockpit-Driving integration and AI supercomputing research: The One Chip solution is rapidly installed in vehicles, and AI supercomputing architectures are moving towards full-domain integration.

AI ...

Intelligent Driving End-to-End Large Model Research Report, 2026

Research on Intelligent Driving Large Models: A Critical Period for Technological Competition and Paradigm Integration

As autonomous driving technology rapidly iterates from L2 to L3?L4, intelligent...

Automotive Digital Key Industry Trend Report, 2026

Digital Key Research: Automotive BLE, UWB and SLE Hardware Layout

The Automotive Digital Key Industry Trend Report, 2026, released by ResearchInChina, analyzes and predicts the digital key market, co...

Monthly Report on Automotive New Technology (May 2026)

UHD gaze technology, full-color LiDAR, UWB, etc. promote the upgrade of intelligent driving perception capabilities

This report is published once a month and is available for annual subscription.The...

In-Cabin Monitoring Systems (DMS, OMS, etc.) Research Report, 2026

In-Cabin Monitoring System Research: DMS to Become Mandatory in 2027, Expected to be Installed in Over 14 Million Vehicles

ResearchInChina released the In-Cabin Monitoring Systems (DMS, OMS, etc.) Re...

Automotive Service-Oriented Architecture (SOA) and Cross-Domain Middleware Industry Report, 2026

Research on automotive SOA and cross-domain middleware: The era of AI atomic services and AI cross-domain fusion agents is coming.

Automotive SOA evolves towards AI + full SOA servitization Driv...