Automotive voice market: The boom of self-research by OEMs will promote reform in the supply mode

Before the advent of fully automated driving, the user focus on driving, and voice interaction is still the most convenient and safest interaction mode in vehicles.

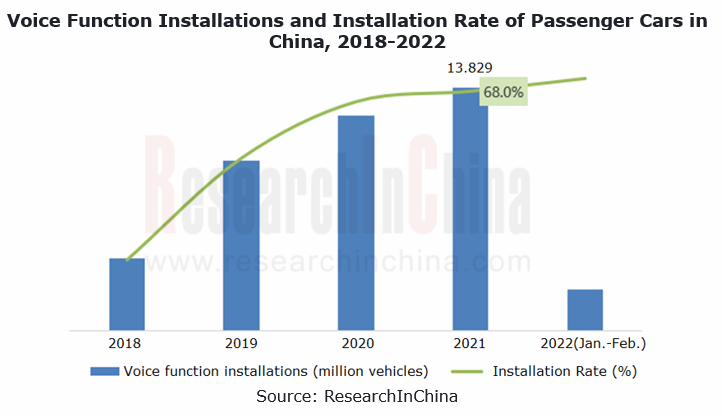

In 2021, over 13 million passenger cars in China carried voice feature, with a year-on-year increase of 13% and an installation rate of 68%. The market bore a rapid bullish trend.

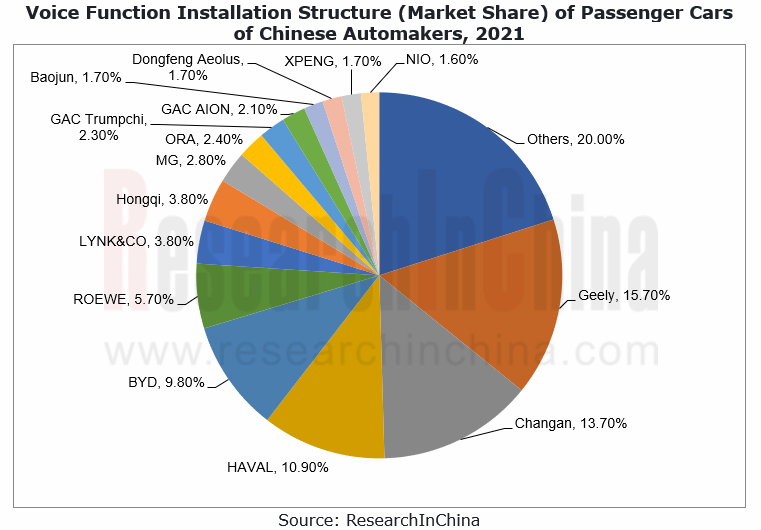

In 2021, more than 5.5 million vehicles of Chinese automakers were outfitted with voice feature, a year-on-year spike of 40.4%. Among the top four brands, BYD saw the voice installations soar by 151% on an annualized basis, and Haval’s rose 53% from a year earlier.

From IVI software to ADAS, voice-enabled functions continue to evolve

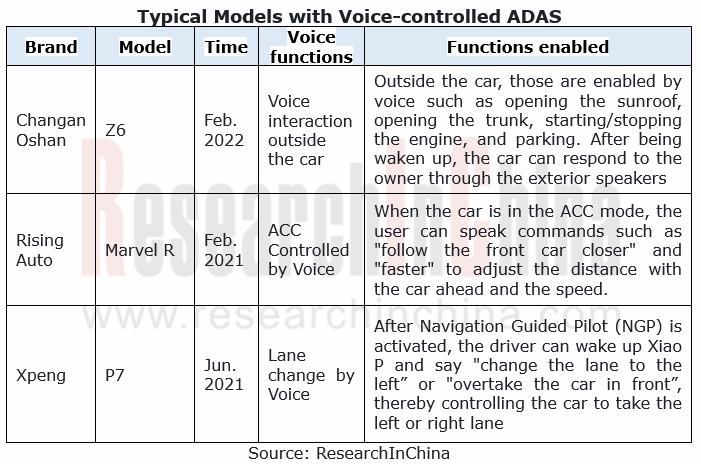

In terms of functionality, what is controlled by voice ranges from IVI software (music, navigation, etc.) to hardware (like seats, air conditioner), power systems (such as driving modes), and to ADAS (like ACC control). With more and more automotive interfaces, voice can control lane change, adaptive cruise, and parking.

iFLYTEK and Cerence are the top two leaders

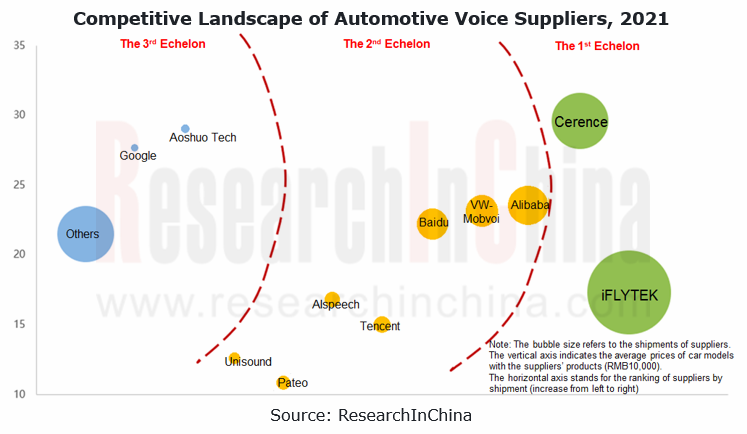

Among suppliers, iFLYTEK and Cerence are in the first echelon, together sweeping more than 70% market shares.

iFLYTEK shipped more than 7 million sets of voice products in 2021, a figure projected to outnumber 9 million sets in 2022 still as the largest supplier in the market.

iFLYTEK mainly serves Chinese carmakers, and the average unit price of models supported ranges from RMB150,000 to RMB200,000. In the OEM market, iFlytek’s voice products have been available in excess of 36 million vehicles, being merited as follows:

? iFLYTEK has delved in the automotive field for 19 years as the industry’s leader in multilingual automatic speech recognition (ASR), text-to-speech (TTS) and other technologies;

? The Feiyu (flying fish) system for automakers employs a software and hardware platform design, which can be reused by multiple models and be introduced rapidly to vehicle models with varying market targets, prices and configurations.

With superiorities in AI expertise, data accumulation as well as the software and hardware platforms that can offer custom-made services, iFLYTEK has become a heavyweight in the automotive voice industry. But other rivals should not be underestimated, especially Cerence (separated from Nuance, a world-renowned giant in intelligent voice).

In 2020, Geely’s China Euro Vehicle Technology (CEVT) and Great Wall Motor's strategic partner Bean Tech announced to select Cerence ARK to develop automotive voice assistants. NIO also proclaimed to introduce Cerence’s voice technology. Prior to this, these brands were all customers of iFLYTEK.

Cerence ARK is an end-to-end AI-powered automotive assistant solution that integrates interactive voice AI technologies such as environment-adaptive voice signal enhancement, custom wake-up words, random interruption of dialogue, multi-intent semantic understanding, wake-up-free multi-round dialogue, and cross-domain dialogue in support of context understanding. Cerence ARK is a turnkey automotive product that enables automakers to quickly develop, deploy and manage a fully localized automotive voice assistant.

In addition, Cerence supports more than 70 languages around the world, making it the best choice for Chinese brands to go overseas. Automakers such as SAIC, Geely, Wuling Motors, NIO and Hongqi have all used Cerence's voice technology in their overseas models.

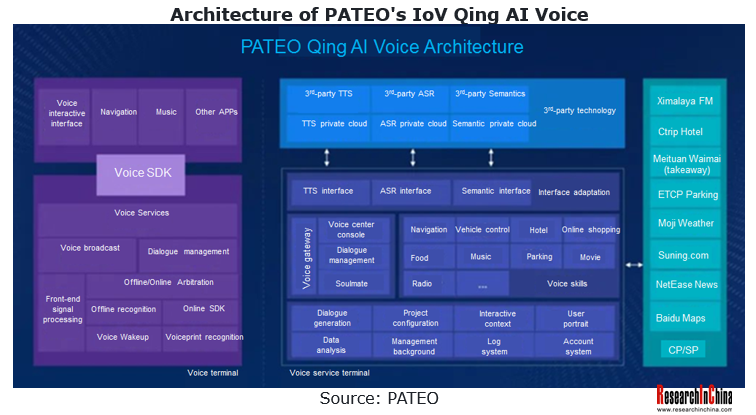

In addition to iFLYTEK, Cerence and the like that can provide OEMs with full-chain voice capabilities, some other suppliers provide a platform that can access the voice capabilities of all companies to satisfy customers who want to "enjoy the benefits of all players". PATEO's IoV Qing AI voice platform is just a reliable choice.

PATEO Qing AI is a voice platform with pluggable capabilities, which supports the access to ASR, NLU, and TTS capabilities of multiple enterprises, provides different voice services to different projects and models, freely configures functions, increases or decreases skills, and facilitates quick application. The platform favors a variety of integration methods of different systems (such as Linux and Android) and different terminals (vehicle and mobile phone).

At present, PATEO's Qing AI voice platform has been connected to the voice capabilities of Cerence, Baidu, AIspeech and iFlytek. It enables full-duplex voice interaction, multi-round dialogue, deep contextual memory and understanding, wake-up-free, “what you see is what you can say”, voice source positioning, voiceprint recognition, voice cloning and other functions. It has been seen in FAW VW, Dongfeng Motor, Wuling Motors (Silver Badge), BEIJING Auto, Geely, etc. The PATEO voice product carried by Voyah FREE supports four-tone-zone voice recognition, multi-round dialogue, navigation, music, car control, and “what you see is what you can say about setting interfaces”, greetings and other functions.

No matter how much suppliers offer, it cannot compete with the lucrativeness brought by "mastery of the core data"

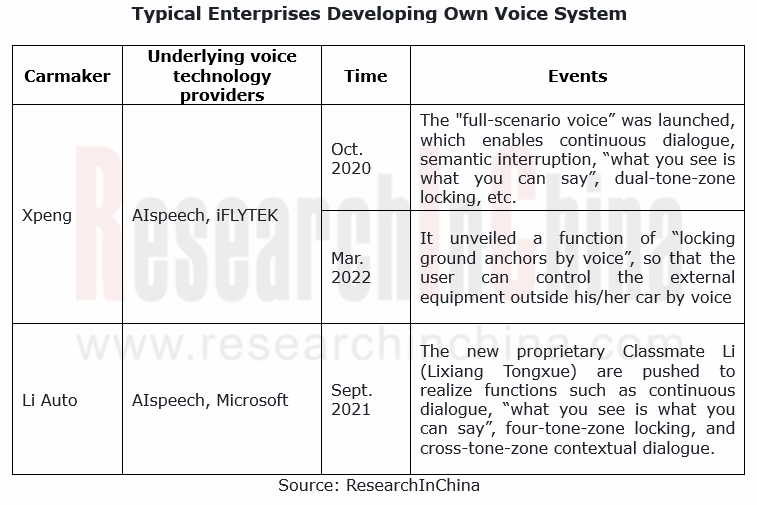

Although the solution packages of suppliers are fine, OEMs want more in terms of function differentiation, security guarantee of open automotive interfaces, quick response of OTA and user data. The OEMs represented by Xpeng and Li Auto have adopted the development model of "introducing the underlying technology of suppliers and developing their own voice system".

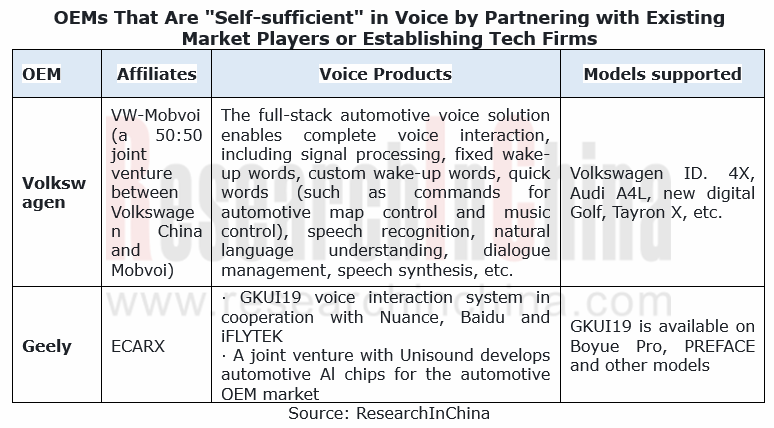

Like Xpeng and Li Auto vigorously developing voice on their own, Volkswagen, Geely, Great Wall Motor, etc. are sparing no efforts in self-developed voice by setting up subsidiaries.

In a nutshell, the mode of traditional OEMs applying suppliers’ solution packages has quietly transferred to the in-depth cooperation between OEMs (with more detailed needs) and technology providers (responsible for delivery). OEMs are not only demanders, but also technology suppliers and system integrators in the voice supply chain. For traditional voice suppliers, the "reform" has kicked off.

OEMs and Tier1s’ Intelligent Cockpit Platform (Hardware and Software) Innovation Strategy Research Report, 2026

Intelligent Cockpit Platform Research: multi-dimensional cockpit system architecture reconstruction for multi-agent collaboration and proactive intelligent services

The intelligent cockpit software s...

Automotive AIOS Research Report, 2026

Automotive AIOS Research: Mass Production Solutions Are Implemented

Mass Production Solutions Are Implemented on A Small Scale.

In 2026, AIOS starts small-scale implementation, helping to improve v...

Automotive Telematics Service Provider (TSP) Research Report, 2026

TSP Research: Leading providers collectively turn to AI agents to provide all-scenario active services

Telematics Service Providers (TSPs) are the core hub of the telematics industry chain, connectin...

Automotive Smart Interior Research Report, 2026

Smart Interior Research: As Technologies like Interactive Starlight Headliner, Hidden Display and Surface Projection Are Launched, Automotive Interiors Become Ever More Intelligent

The Automotive Sma...

Research Report on AI Applications in Cockpits, 2026

AI Application in Cockpits: AI Services Become More Comprehensive, Convenient, and Refined.

In the first half of 2026, cockpit AI functions underwent initial upgrades across multiple dimensions, inc...

Software-Defined Vehicles in 2026: OEM Software Development and Supply Chain Deployment Strategy Research Report

Research on OEMs’ Software Strategies: R&D Focus, Development Strategies and Supplier Building Models of 30 OEMs

In this paper, we adopt a research framework covering 13 subsystems and 48 sub-di...

Passenger Car Chassis Domain Control and Chassis Cross-Domain Integration Research Report, 2026

Chassis Control Research: Mass Production of Full Chassis-by-Wire Solutions Starts

1. A Cluster of Full Chassis-by-Wire Solutions Make Their Debut, and EMB Enters Mass Production and Adoption for the...

Central Domain Control (Powertrain, Chassis, Body) and Motion Controller Research Report, 2026

Central Domain Control and Motion Control Research: XYZ Coordinated Control and Full X-by-Wire Actuation System

With the gradual penetration of L3+ autonomous driving, the chassis control system is ...

48V Low-voltage Power Distribution Network (PDN) Architecture and Supply Chain Panorama Research Report, 2026

Research on 48V Low-Voltage Power Distribution Network (PDN): An Active 48V Supply Chain, with Priority Deployment in High-Power Scenarios Such as Steer-by-Wire Chassis

The automotive 48V low-voltage...

AI-Defined Vehicle (AIDV) OEMs' Deployment Strategies Research Report, 2026

AIDV Research: Deployment Strategies of 22 OEMs

The AI-Defined Vehicle (AIDV) OEMs' Deployment Strategies Research Report, 2026, released by ResearchInChina, analyzes the AI deployment strategies of ...

OEMs’ Passenger Car Model Planning Research Report, 2026

Vehicle Model Planning Research: Chinese OEMs Launch Sub-Brands Intensively, While Multinational OEMs Apply the Brakes to Electrification Strategies

ResearchInChina released the OEMs’ Passenger Car M...

Autonomous Driving Simulation and World Model Research Report, 2026

Autonomous driving simulation research: "Simulation test + world model"-driven test system has become R&D infrastructure.

The "Autonomous Driving Simulation and World Model Research Report, 2026"...

Cockpit-Driving Integration Central Domain Controller SoC and AI Supercomputing Architecture Research Report, 2026

Cockpit-Driving integration and AI supercomputing research: The One Chip solution is rapidly installed in vehicles, and AI supercomputing architectures are moving towards full-domain integration.

AI ...

Intelligent Driving End-to-End Large Model Research Report, 2026

Research on Intelligent Driving Large Models: A Critical Period for Technological Competition and Paradigm Integration

As autonomous driving technology rapidly iterates from L2 to L3?L4, intelligent...

Automotive Digital Key Industry Trend Report, 2026

Digital Key Research: Automotive BLE, UWB and SLE Hardware Layout

The Automotive Digital Key Industry Trend Report, 2026, released by ResearchInChina, analyzes and predicts the digital key market, co...

Monthly Report on Automotive New Technology (May 2026)

UHD gaze technology, full-color LiDAR, UWB, etc. promote the upgrade of intelligent driving perception capabilities

This report is published once a month and is available for annual subscription.The...

In-Cabin Monitoring Systems (DMS, OMS, etc.) Research Report, 2026

In-Cabin Monitoring System Research: DMS to Become Mandatory in 2027, Expected to be Installed in Over 14 Million Vehicles

ResearchInChina released the In-Cabin Monitoring Systems (DMS, OMS, etc.) Re...

Automotive Service-Oriented Architecture (SOA) and Cross-Domain Middleware Industry Report, 2026

Research on automotive SOA and cross-domain middleware: The era of AI atomic services and AI cross-domain fusion agents is coming.

Automotive SOA evolves towards AI + full SOA servitization Driv...