China In-Vehicle Payment Market Research Report, 2023 released by ResearchInChina analyzes and researches the status quo of China's in-vehicle payment market, components of the industry chain, layout of OEMs and payment platforms, consumer survey, and development trends.

①The market demand for in-vehicle payment is rising.

In-vehicle payment refers to the function allowing for payment through in-vehicle communication (e.g., SIM card and WiFi) and IVI system. In-vehicle payment enables car owners to pay for services such as parking, refueling, food ordering and shopping without getting off the car, bringing far more convenient and better experience to users.

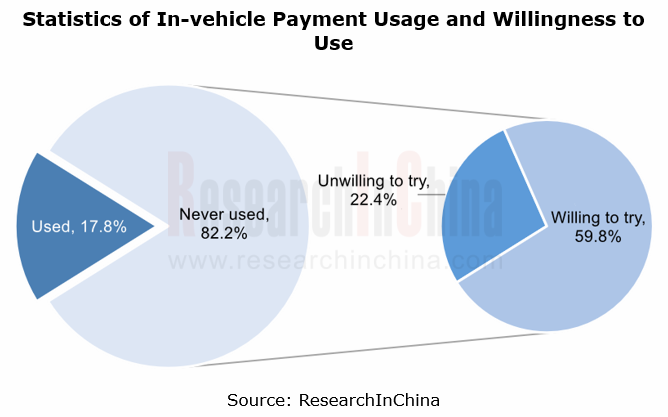

According to the survey by ResearchInChina, there are a relatively small number of people using in-car payment at this stage, making up only 17.8% of the total samples. Yet users' willingness to use this function is very high. 72.7% of the consumers who have not used in-car payment yet, or 59.8% of the total samples say they are "willing to try in-car payment".

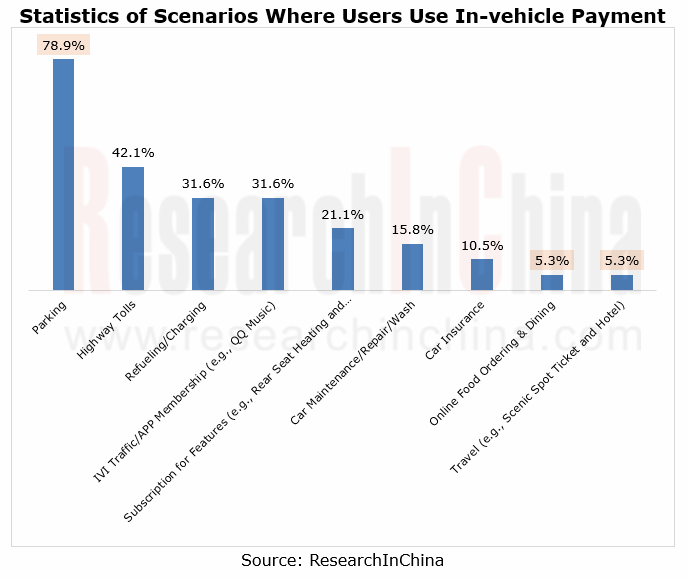

At present, users use in-car payment in such scenarios as parking, highway pass, refueling/charging, and purchasing IVI traffic and APP membership. Of the users who have used in-car payment:

- Up to 78.9% use in-car payment for parking;

- 42.1% use in-car payment for highway tolls;

- In-vehicle payment is also often used to pay for refueling/charging fees (31.6%), IVI traffic and APP membership (31.6%), feature subscription (21.1%), car maintenance/repair/wash (15.8%), and car insurance (10.5%);

- Fewer users use this function in the scenarios of online food ordering and dining (5.3%) and travel (5.3%).

②The in-vehicle payment industry chain is taking shape.

In terms of supply chain, in-vehicle payment involves two major segments: in-vehicle payment device and in-vehicle payment platform.

In-vehicle payment devices are led by communication devices (SIM card, communication module and T-Box), interaction devices (touch/voice/ face/gesture/fingerprint interaction), and authentication devices (security chip); in-vehicle payment platforms are primarily cloud platform, payment platform, IVI system, ecosystem service platform, ecosystem service provider, and OEM.

As companies in each industry chain segment worked to make layout in recent years, the in-vehicle payment market has kept growing, with the following two major features.

1. In-vehicle payment is available to more scenarios.

Foreign automakers including BMW, Mercedes-Benz, Honda and Hyundai, and Chinese automakers such as Great Wall Motor, Xpeng Motors, Geely, Chery and AITO have launched their in-car payment function. They have widely deployed this function in parking, refueling/charging and food ordering scenarios, and are also applying it on a small scale in car wash/maintenance/repair services, feature subscription, ticket booking and other scenarios.

For example, in October 2022, BMW added the BMW ConnectedDrive Store to its IVI system via OTA updates. It enables in-car payment for subscriptions, and 13 features such as front seat heating, steering wheel heating and Carplay through the IVI system.

2. Multimodal interaction is being added to in-vehicle payment.

At present, the most common in-car payment is scan to pay and password-free payment. As in-car multimodal interaction technology improves, face recognition, fingerprint recognition and voice recognition are becoming the new in-car payment interaction and authentication methods.

For example, Mercedes-Benz has added fingerprint recognition and authentication to its latest in-car payment system PAY+; Chery EXEED TX/TXL supports face verification payment, a function allowing users to pay for parking fees or shopping through face recognition. The addition of multimodal interaction makes in-vehicle payment more secure and convenient.

3. The ecosystem is a key factor affecting in-car payment.

In the mobile payment system, millions of iOS and Android developers have developed various applications and built very rich application ecosystems, meeting living, work and entertainment needs of consumers and making smartphones an indispensable terminal in users' life.

In the in-car payment system, financial institutions like China UnionPay and VISA have developed a series of in-car payment systems; Alipay, Banma Zhixing and Huawei among others have built a variety of vehicle ecosystem platforms and launched a range of in-car services covering parking, refueling, travel, shopping and other scenarios.

Compared with mobile payment, the in-vehicle payment ecosystem is still weak at this stage, only meeting the payment needs in specific scenarios. With the development of intelligent cockpit and high-level autonomous driving, drivers will be freed from driving tasks in specific scenarios and pay more attention to other in-car needs. At this time, creating an in-car living space and building a closed-loop ecosystem with payment as the entrance will become a big demand.

Automotive AIOS Research Report, 2026

Automotive AIOS Research: Mass Production Solutions Are Implemented

Mass Production Solutions Are Implemented on A Small Scale.

In 2026, AIOS starts small-scale implementation, helping to improve v...

Automotive Telematics Service Provider (TSP) Research Report, 2026

TSP Research: Leading providers collectively turn to AI agents to provide all-scenario active services

Telematics Service Providers (TSPs) are the core hub of the telematics industry chain, connectin...

Automotive Smart Interior Research Report, 2026

Smart Interior Research: As Technologies like Interactive Starlight Headliner, Hidden Display and Surface Projection Are Launched, Automotive Interiors Become Ever More Intelligent

The Automotive Sma...

Research Report on AI Applications in Cockpits, 2026

AI Application in Cockpits: AI Services Become More Comprehensive, Convenient, and Refined.

In the first half of 2026, cockpit AI functions underwent initial upgrades across multiple dimensions, inc...

Software-Defined Vehicles in 2026: OEM Software Development and Supply Chain Deployment Strategy Research Report

Research on OEMs’ Software Strategies: R&D Focus, Development Strategies and Supplier Building Models of 30 OEMs

In this paper, we adopt a research framework covering 13 subsystems and 48 sub-di...

Passenger Car Chassis Domain Control and Chassis Cross-Domain Integration Research Report, 2026

Chassis Control Research: Mass Production of Full Chassis-by-Wire Solutions Starts

1. A Cluster of Full Chassis-by-Wire Solutions Make Their Debut, and EMB Enters Mass Production and Adoption for the...

Central Domain Control (Powertrain, Chassis, Body) and Motion Controller Research Report, 2026

Central Domain Control and Motion Control Research: XYZ Coordinated Control and Full X-by-Wire Actuation System

With the gradual penetration of L3+ autonomous driving, the chassis control system is ...

48V Low-voltage Power Distribution Network (PDN) Architecture and Supply Chain Panorama Research Report, 2026

Research on 48V Low-Voltage Power Distribution Network (PDN): An Active 48V Supply Chain, with Priority Deployment in High-Power Scenarios Such as Steer-by-Wire Chassis

The automotive 48V low-voltage...

AI-Defined Vehicle (AIDV) OEMs' Deployment Strategies Research Report, 2026

AIDV Research: Deployment Strategies of 22 OEMs

The AI-Defined Vehicle (AIDV) OEMs' Deployment Strategies Research Report, 2026, released by ResearchInChina, analyzes the AI deployment strategies of ...

OEMs’ Passenger Car Model Planning Research Report, 2026

Vehicle Model Planning Research: Chinese OEMs Launch Sub-Brands Intensively, While Multinational OEMs Apply the Brakes to Electrification Strategies

ResearchInChina released the OEMs’ Passenger Car M...

Autonomous Driving Simulation and World Model Research Report, 2026

Autonomous driving simulation research: "Simulation test + world model"-driven test system has become R&D infrastructure.

The "Autonomous Driving Simulation and World Model Research Report, 2026"...

Cockpit-Driving Integration Central Domain Controller SoC and AI Supercomputing Architecture Research Report, 2026

Cockpit-Driving integration and AI supercomputing research: The One Chip solution is rapidly installed in vehicles, and AI supercomputing architectures are moving towards full-domain integration.

AI ...

Intelligent Driving End-to-End Large Model Research Report, 2026

Research on Intelligent Driving Large Models: A Critical Period for Technological Competition and Paradigm Integration

As autonomous driving technology rapidly iterates from L2 to L3?L4, intelligent...

Automotive Digital Key Industry Trend Report, 2026

Digital Key Research: Automotive BLE, UWB and SLE Hardware Layout

The Automotive Digital Key Industry Trend Report, 2026, released by ResearchInChina, analyzes and predicts the digital key market, co...

Monthly Report on Automotive New Technology (May 2026)

UHD gaze technology, full-color LiDAR, UWB, etc. promote the upgrade of intelligent driving perception capabilities

This report is published once a month and is available for annual subscription.The...

In-Cabin Monitoring Systems (DMS, OMS, etc.) Research Report, 2026

In-Cabin Monitoring System Research: DMS to Become Mandatory in 2027, Expected to be Installed in Over 14 Million Vehicles

ResearchInChina released the In-Cabin Monitoring Systems (DMS, OMS, etc.) Re...

Automotive Service-Oriented Architecture (SOA) and Cross-Domain Middleware Industry Report, 2026

Research on automotive SOA and cross-domain middleware: The era of AI atomic services and AI cross-domain fusion agents is coming.

Automotive SOA evolves towards AI + full SOA servitization Driv...

Automotive Display, Center Console and Cluster Industry Report, 2026

Automotive Display Research: Multi-Screen Application Slows Down, While OLED and MiniLED Are Introduced in Vehicles Quickly

In 2026, automotive displays will no longer excessively pursue the number a...